"People won’t casually engage with this stuff. They’ve got to want to know, you have to want to go down that rabbit hole, you have to want to understand what’s going on."

Upon finishing Grant Williams’ impressive three and a half hour interview with David Rogers Webb, I figure I can send this particular “Havenstein Moment” to the presses.

Even before getting to the “Great Taking” stuff, a lot of what Webb had to say resonated with me. I highly suggest subscribing to Grant’s service for this sort of content.

As for subscribing here, if you’re not a paid subscriber, please consider doing so. A lot of time and winnowing goes into these posts, and it’s cheaper for you than eating at Denny’s more than once or twice a year.

USA Ratio of Total Market Cap to GDP

“Name one long-term problem that we’ve solved in the last 4, 8, 12 years? We’ve only made everything worse. And now we’ve got this insane border policy…Every problem we have, we’ve made worse…Beneath the surface, and away from the stock market there are a lot of really serious issues that just aren’t being addressed.”

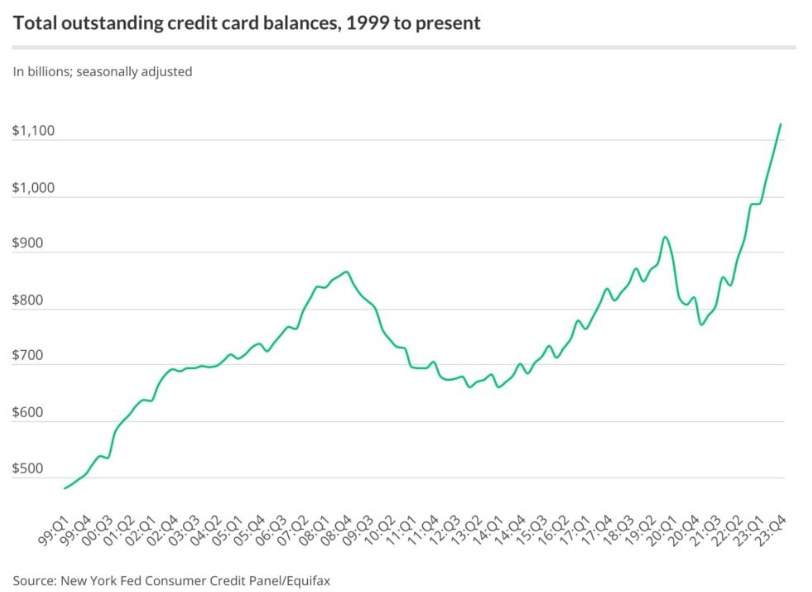

Credit Card Debt

RV Shipments

Jim Grant

“I would say that, as important as the future of interest rates goes, I think the recent past of rates is just as and perhaps more important. By that I mean the 10 or so years of - figuratively speaking - free money, money growing on trees, has had profound effects on the structure of things, on expectations, on valuations - especially on the structure of our consolidated corporate balance sheet.”

“I would say that interest rates are perhaps the most important prices in capitalism, and I would that interest rates inform, but manipulated interest rates misinform, and I think where we stand is in good part on the very unsteady ground of manipulated interest rates, therefore manipulated expectations and manipulated balance sheets.”

“The Fed has nailed its colors to the flag of a 2% measured rate of inflation, 2% or so, maybe a little bit more. However it also has a dog in the fight of financial

stability, and by its policies of the past 10 or a dozen years, it has unintentionally worked to subvert financial stability.”

“You've got a Fed that is chomping at the bit to cut in the face of a $3 trillion crypto market cap, an example of how we might not be starved of liquidity.”

“The month was October 1955, and the Brooklyn Dodgers had just won the World Series, which is apropos of actually nothing except that I was thrilled by that. I was 26 of the time, a little bit impressionable, and so what [William McChesney] Martin says - let me quote - he said my good friend, the President of the Federal Reserve Bank, Allan Sproul, says that there was a thing that called creeping inflation, and, you know, the Harvard economists said that two, or three, or three and a half percent inflation was good for us, because it lubricated the wheels of Commerce, you had to have a little bit of that, you didn't want deflation - this is where this deflation phobia thing began to surface - so the President of the Federal Reserve Bank of New York said, is that really what we want? Who's going to tell the life insurance guy, who's going to tell the saver, who's going to tell the the owner of savings bonds a 3% loss every year is good? So it was an argument based upon the morality of money. Money is work. Work is heartbeats. Heartbeats are finite therefore it's a moral question. So that was then.”1

“From about 1820 until about 1914, the price level was stable to slightly declining. That's according to the Bank of England's historical data.”

“You have the Federal Reserve, which actually knows it doesn't know ,but pretends it knows, and in this pretense does inordinate damage to things by messing up interest rates.”

Lacy Hunt

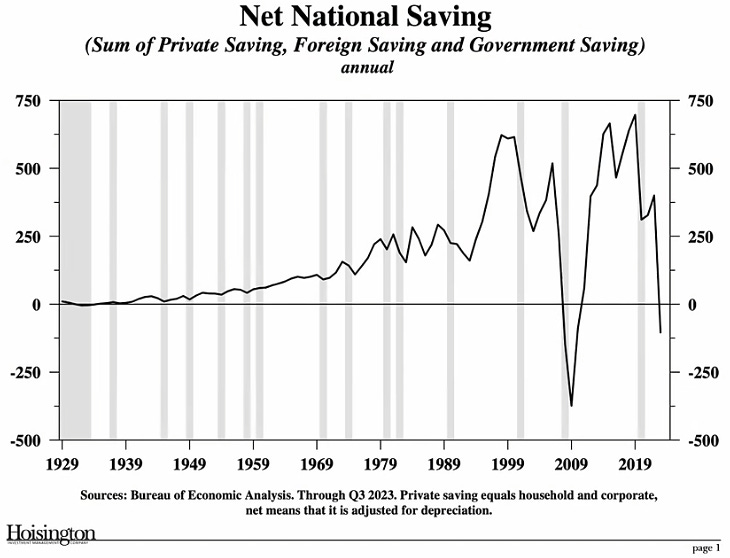

“With negative net national savings we are at a more perilous state. It's an indication that the economy collectively is living beyond its means, and there is now a constraint on the production function.”

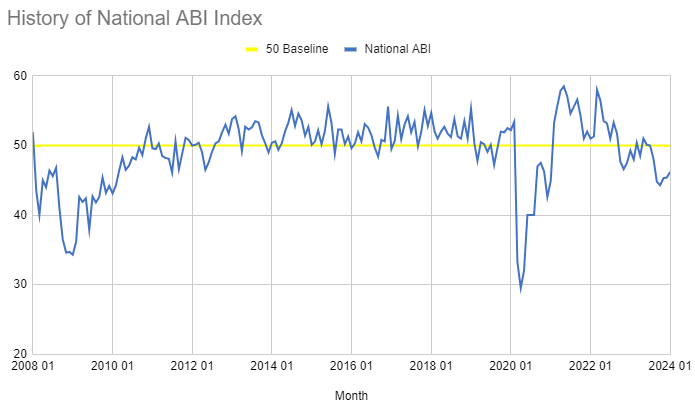

Architectural Billings Index

“The Architecture Billings Index (ABI) is a leading economic indicator for nonresidential construction activity, with a lead time of approximately 9–12 months.”

“This now marks the lengthiest period of declining billings since 2010, although it is reassuring that the pace of this decline is less rapid and the broader economy showed improvement in January,” said Kermit Baker, PhD, AIA Chief Economist.

America’s Office Fire Sale Has Barely Begun

It appears we are currently in another period of “extend and pretend”

“Pressure is building slowly as leases expire: Many companies are reducing their space by 30% to 40% when their contracts end. Lenders are also eager to kick the can down the road. They don’t want to force borrowers to sell buildings into a weak commercial real-estate market, which would lead to punishing losses.

This might explain why debt maturities aren’t triggering the kind of distress that some property watchers expected [yet]. Of the $35.8 billion of office loans that came due in the commercial mortgage-backed securities market last year, only a quarter were paid off in full”

“CIM Group has sold 888 at Grand Hope Park, a 34-story luxury residential tower in Downtown Los Angeles, for $186 million…The deal comes eight months after the company listed the 525-unit property with an asking price of $236 million. At that time, the property was 94 percent occupied. The initial asking price was 40 percent lower than replacement cost…If accurate, that would make the final purchase price about 53 percent less than replacement cost.”

In San Francisco, a 20-story office tower that sold for $146 million a decade ago was listed in December for just $80 million.

In Chicago, a 200,000-square-foot-office building in the city’s Clybourn Corridor that sold in 2004 for nearly $90 million was purchased last month for $20 million, a 78 percent markdown.

And in Washington, a 12-story building that mixes office and retail space three blocks from the White House that sold for $100 million in 2018 recently went for just $36 million.

“It means less money in municipal coffers and a less robust downtown…Some cities that tried to raise taxes and cut back on public services found that those responses accelerated the process of urban flight. It sort of compounded itself.”

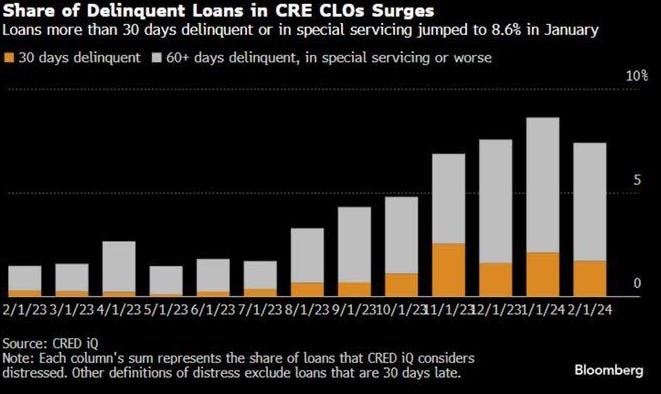

CLO’s

“An obscure investment product used to finance risky real estate projects is facing unprecedented stress as borrowers struggle to repay loans tied to commercial property ventures. Known as commercial real estate collateralized loan obligations, or CRE CLOs, they bundle debt that would usually be seen as too speculative for conventional mortgage-backed securities into bonds of varying risk and return.

In just the last seven months the share of troubled assets held by these niche products has surged four-fold, by one measure, to more than 7.4%. For the hardest hit, delinquency rates are in the double digits. That’s left major players in the $80 billion market rushing to rework loans, while short sellers are ramping up attacks on publicly-traded issuers they say may be so beset by missed payments that they have little to no equity value…

They’re primarily stuffed full of short-term, floating-rate loans for properties undergoing renovations or expansions, the type of risky debt that banks or CMBS often don’t want to hold. With rising interest rates eroding resale prices for refurbished multifamily dwellings and demand for office space still tepid, many borrowers are starting to struggle to meet their obligations. That’s left a number of CRE CLO issuers — which finance the riskiest part of the structures themselves and sell off the safer pieces — already absorbing losses.

Some say the pain could eventually spread to those invested in less risky portions, too. “The CRE CLO market is the first shoe to drop in terms of defaults in the CRE debt markets”…

To be sure, the highest rated debt issued by CRE CLOs benefit from ample protection built into the structure of the securities, and analysts across the board expect those bonds to be just fine.”

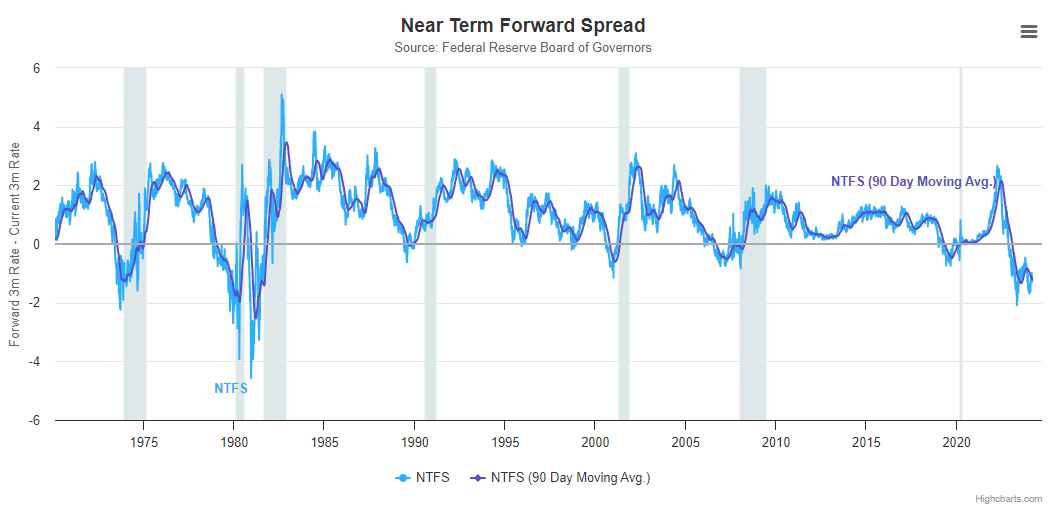

“The near term forward spread is the difference between the expected 3-month interest rate 18-months from now minus the current 3-month yield. The near term forward spread is a good indicator of the future stance of monetary policy as well as recessions. The blue line shows the most recent estimate of the NTFS, while the purple line shows the 90 day moving average. The gray bars represent NBER recession dates.”

Amy Nixon

“The real estate agent benefits a family. That's who needs an agent, a family who wants somebody that understands the neighborhood, who wants somebody to walk them through homes personally, and tour and explain different things about the home, and the neighborhood, and who wants to feel like they have an advocate. That's that's the real estate agent is really there for.

By making real estate agents less necessary, with the sort of promise of ‘oh well, this might save you a little bit of transaction costs’, what it's actually doing though is making things easier for investors and these tech companies to own the market, and run the market. That's really what's going to be I think the long-term trajectory of what flows out of this judgment, and I don't like to see that, because the human element of the housing market is what I'm here for, and I've seen how investors impacted the market so much in 2021 -and pretty much since Covid - investors have just come like vultures on any affordable housing in a lot of metros, and just turned them all into rentals.

That's not something that I want to see for people, and for our future, and unfortunately I just don't see what's going to make them stop, because even in this tighter credit market, with rates hiked, and cap rates not being very favorable anymore in terms of it takes a lot of work now to find a property that's actually going to cash flow, and the numbers run right, with prices and rates the way they are today - but investors are still getting deals done, and they're still making cash offers, because I think long term they see what I've been seeing lately, which is that our money's going to continue to get debased, and that means hard assets are where you want your money to be parked to protect yourself.”

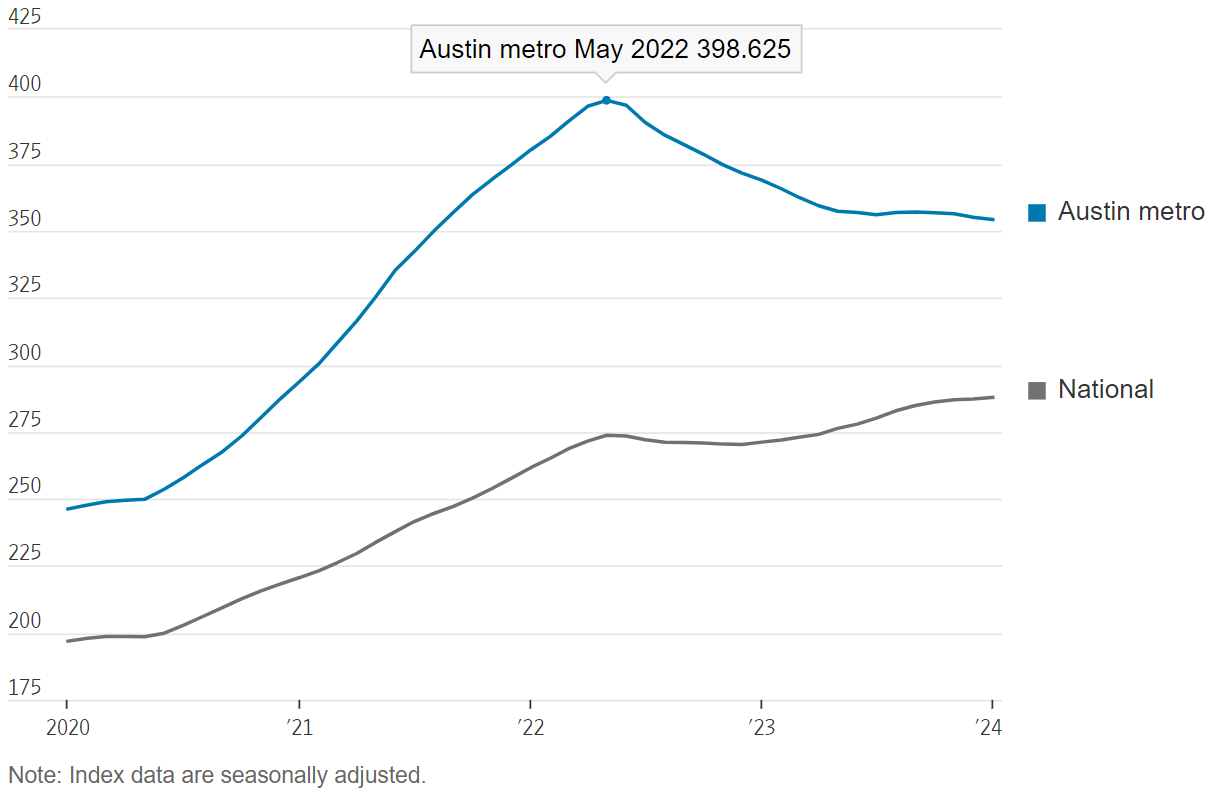

Once America’s Hottest Housing Market, Austin Is Running in Reverse

Home prices have fallen more than anywhere in the U.S.

Phoenix

“The supply of homes for sale in the Phoenix MLS is almost back to 2018 levels – pre-pandemic levels. The number of homes for sale (all home types) in the Phoenix area MLS could surpass 2018 levels by the end of March.”

Canada Is Spending 75% of Its Planned Budget Deficit To Buy Mortgage Bonds

“The move will inject additional liquidity into the mortgage market, similar to the way quantitative ease (QE) did. While the Bank of Canada (BoC) will be in charge of executing this policy, they want it to be crystal clear—this isn’t QE, it’s fiscal spending. QE involves balance sheet expansion and is designed to stimulate demand, and raise inflation. The GoC policy will only stimulate mortgage demand and therefore apply positive pressure to inflate home prices.”

“So they are literally trying to make Canadian housing even MORE unaffordable? This all sounds so beyond insane it doesn’t even sound like something Canada would do.”

I saw a thread on this article: 'I am losing my mind': Behind the rosy job numbers, Americans are struggling to find work, and in the comments it became a commentary on education, and maybe the general mood, in America today:

“I've got jobs for ya'll. I'm an asst. principal. In my school district we are short a few dozen teachers forcing me to shove over 35 kids into some classes. It's absolutely crisis mode in some areas, particularly special ed. We get ZERO apps for teaching vacancies. If you have ANY degree and can fog a mirror, we'll give you a temp cert and get you on track for your permanent cert. Doesn't matter in what. Degree in business? Sociology? We'll have you teaching English, social studies, or chemistry so that you don't know what the f*ck you're doing and quit middle of the year. Work for us and you'll get paid 55k to teach kids who are braindead from their phones, deal with bitchy parents and exhaust yourself in general. But hey, 8 weeks during summer off (unpaid) and a pension based on a shit salary if you last 30 years. You get 2k raises per year and end at 85k. Oh did I mention that houses start at 575k in the area?”

“As a former teacher who got out, I want to recommend that no one apply for teaching jobs in the United States right now unless you are desperate. The shortage is deserved.”

“Similar here. One of our retiring math teachers has made it her mission to convince people not to go into this. My therapist tells me that since 2020, his clientele has exploded with nurses, police officers, firemen, and teachers. Police and teachers especially. He said he used to have more wealthy people before that, never got so many "middle class" people wanting therapy before. Including me.”

“In all my years I’ve never seen so many tenured teachers leaving midyear. And we can rarely any qualify candidates to take their place. When I became a teacher, there were hundreds of candidates, and I felt super fortunate to find this job and now basically we are begging for people to come work for us. I strongly believe there will not be any new teachers within five years and with the current wave of retirements and people quitting the profession early…I’m not sure how we can possibly keep public schools even open.”

David Rogers Webb

“In a lot of ways, I was very happy there and well-treated. I had a lot of respect for the intelligence of the people and the whole process. It’s an incredible platform and place to be do things, but it’s an addiction. The people that stay there, they’re addicted to being in this seat of power. And I’ve always found, it’s useful to look at the lives of the people that are maybe five years ahead of you, what are their lives like? And they were all on their second or third marriage or divorced. The women had never been married because they couldn’t have a personal life. So it’s an addiction.

…the money is not it. There was one guy, the guy who ran the medical venture area within Warburg, I remember one of the partners telling me that he had gotten a payout from something. And he had 60 million in his checking account because he didn’t have time to deal with it…you only need so much. And that’s something I knew early on. I don’t understand this obsession with chasing money.”

David Rogers Webb with Grant Williams

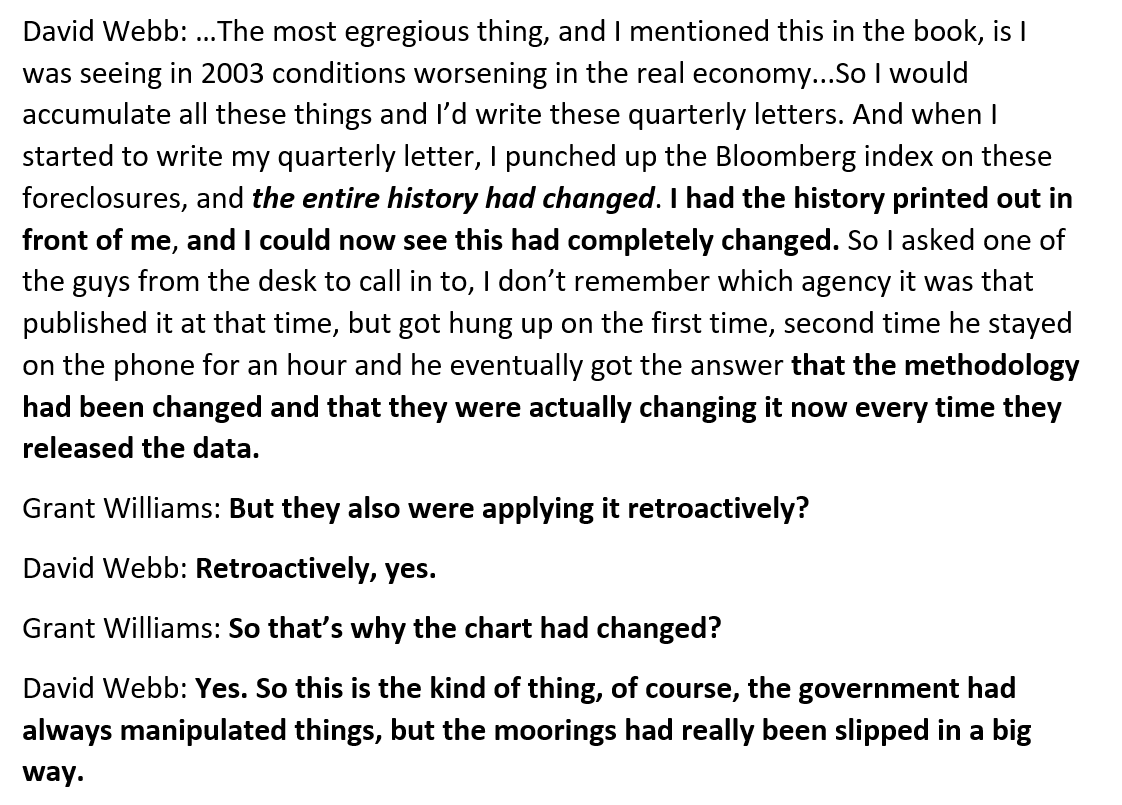

Webb talking about the late 1990’s:

“I started looking at what the Fed was doing, and you could see the effect of the open market operations. I followed M3 week-by-week, and I could see that in individual weeks the amount of new money was over a percent of GDP. In a week. Now, it wasn’t always that much, but still you’re going again into something that’s an order of magnitude bigger than whatever the economic growth was. They were always growing it, but it would accelerate and decelerate the growth…

The main insight was that there was something big affecting the markets that was not the real economics of the businesses, and it just became more and more extreme. But people can remain out of touch with what is really happening for a surprisingly long period of time…

What I was seeing happening through this post-Asian financial crisis is I could see the scale of the money creation was much higher than any economic growth, and I could see it at the margin incrementally that’s what was happening. That meant that the velocity of money had inverted. That the money creation, especially at the margin, was much higher than any economic growth that was happening. So the problem is, as people would know, it’s not going into the real economy, but I believe it then begins damaging the real economy. So it’s not helping the real economy, but it actually begins damaging the real economy.

And it goes into, and maybe we will get into this more later, I think it becomes part of the war cycle where it is going into unproductive purposes and downright destructive purposes and ends up actually damaging people broadly. So the velocity, when it really totally collapses, it’s an end-stage process where the money creation is entirely going into things that are not helping people, it’s hurtful to people. So that’s what was beginning to happen, and it was shocking to me.”

The Fed and BLS are rewriting history.

The Great Taking

Webb is famous for writing the book, The Great Taking, which he summarizes as the process since the 1960’s of taking :

“all property, financial property that could not have been taken in insolvency, because it was directly owned, and could have been directly owned even with electronic entry, and made it into a contractual claim that will have no standing.”

The Depository Trust Corp. (DTC, with an absurd $3.5 billion worth of equity backing many tens of trillions), is central to his thesis.

Essentially, his claim is that your holdings of, say, Berkshire Hathaway shares at a brokerage would - in the event of brokerage insolvency - exist in some sort of common pool, subject essentially to the type of “fraudulent conveyance” he says took place at Lehman in 2008.

A few “super creditors” (The G-SIB’s) would have first dibs on collateral, and you'd get what what left, maybe.2 (For individual accounts at Lehman, Webb likened it to a “returned stolen car.”)

Most of the interview I found very interesting, and I agreed with him on a number of life lessons (some quoted above), but I don’t know. He mentions the 2008 bankruptcy of a Florida broker dealer having set him on his journey, but that bankruptcy is mentioned only once, briefly, in his book:

“In 2008, I noticed the failure of a small broker dealer in Florida, and I was shocked to learn that client assets owned outright with no borrowing against them were swept to the receiver and encumbered in the bankruptcy estate. I had to understand how this could possibly have happened, and eventually uncovered that ownership right to securities, which had been personal property for four centuries, had somehow been subverted. This would be born out further in the bankruptcies of Lehman Brothers and MF Global.”

The first thing I though when I heard Webb say the above was, “I’m gonna look that up.” It would’ve been nice to get a little more color on this. I searched but was unable to find the broker dealer he was referring to.

He did mention a few more interesting things, like this quip:

“Those the gods would destroy, they first encouraged to borrow cheaply.”

Webb’s discussion of the “Paper Crisis” of 1968 was interesting. I found an interesting 2009 description of this long-forgotten event, starting out with an interesting problem:

With an investment in Compass Knowledge Holdings, Inc. of nearly $800,000 and some 540,000 shares, we own 3.4% the company’s more than 16 million outstanding shares. However, we are not recognized as shareholders by the company. Moreover, we are but one of more than 200 beneficial shareholders holding over 4 1/2 million shares of the company who are not counted as shareholders by the company.

The reason for this is of course we and the other 200 plus beneficial shareholders are not registered shareholders. This is the case because our collective shares of stock are held by our respective stock brokerage firms, each of which hold and register all of the shares in same single nominee name Cede, the nominee of the Depository Trust Company known as DTC. The latter is required to look through Cede but only to count the handful of brokerage firms holding stock as registered stockholders, but is neither required nor does it look through to the more than 200 of the brokers’ separate client accounts, the beneficial holders, who actually own the millions of shares of Compass Knowledge Holdings stock.

By counting only the handful of brokerage firms as holders of record rather than the more than 200 separate client accounts owning millions of shares each of whom are beneficial holders, together with what probably are a couple of hundred beneficial stockholders holding stock certificates, who were therefore counted as holders of record, Compass Knowledge Holdings, Inc. several years ago was allowed to certify that it had fewer than 300 shareholders, according to the SEC definition of shareholder, i.e. registered shareholder, even though it had considerably more than 300 actual i.e. beneficial stockholder owners…

Compass has claimed it is a private company since it is no longer required to comply with SEC rules and regulations requiring full disclosure of what is normal and usual information to shareholders in the United States of America such as annual or quarterly reports, proxies, insider purchases and sales of stock on Form 4 or 13-D filings, or financial P R releases, or conference calls, etc and has not even held annual meetings. So we and all the other over 300 outside shareholders are completely in the dark as to what goes on in the company.

The Paper Crisis

“…In 1968, this system for clearing and settling securities transactions disintegrated into chaos. Volumes on the New York and American Stock Exchanges exploded, and responding to an increased interest in over-the-counter issues, the NASD began development of NASDAQ. Stock transfer departments were overwhelmed by the increased volumes and began to fall behind. Delays at one firm held up the work at other firms who were waiting to receive stock certificates. Errors were generated causing more work; certificates were lost or stolen.

By December 1968, unsettled trades had accumulated to $4 billion and "the trade settlement system had virtually broken down." This "paperwork crisis," which lasted until 1971, was described in the resulting Congressional hearings as "the most prolonged and severe crisis in the securities industry in 40 years." The main culprit of the "paperwork crisis" was generally agreed to be the "stock certificate."

An influential report by Lybrand, Ross & Montgomery, for example, concluded that the "stock certificate [was] a chief catalyst of the paper crisis that in 1968 brought Wall Street to the edge of chaos." When the elimination of stock certificates proved to be politically unfeasible, the securities industry, with the strong encouragement of the Commission and Congress, began searching for ways to immobilize the stock certificate. The immobilization of stock certificates has largely been accomplished through the use of street names and the creation of securities depositories.

In 1968, the New York Clearing Corporation, a subsidiary of the New York Stock Exchange, established the Central Certificate Service, which was ultimately succeeded by The Depositary Trust Company (DTC), using a system that has continued to date. Under this system, investors are strongly encouraged to leave their certificates in an account maintained by a broker-dealer. In turn, broker-dealers maintain accounts at DTC, indicating the total number of shares held for their customers' accounts. To execute a delivery, the selling firm instructs DTC to debit its account for the amount of the sale and credit the buying broker's account. Title to the shares is transferred by computer entries, eliminating the necessity of physical transfer of the certificate from customer to broker, broker to broker, and broker to customer.

The immobilization of stock certificates has eliminated the prior function of stock certificates to identify beneficial owners as "holders of record." In contrast to conditions in 1965, beneficial owners are no longer represented in the vast majority of cases as "holders of record". Instead, beneficial owners are represented almost entirely on the corporate books by "CEDE & Co.," the nominee for banks and brokerage firms with accounts at DTC, and other nominee names serving similar function under other clearing systems”

The Curious William (Bill) Dentzer, Jr

From Webb’s book:

“In the grand scheme to confiscate all collateral, dematerialization of securities was the essential first step. The planning and efforts began over half a century ago. That there was some great strategic purpose behind dematerialization is evidenced by the fact that the CIA was assigned the mission. The project leader was William (Bill) Dentzer, Jr., a career CIA operative.”

Wait, what??

“Though he [Dentzer] had no background in any aspect of banking or finance, he was appointed New York State Superintendent of Banks by Nelson Rockefeller. This came after his nomination to the newly-formed New York State Council of Economic Advisors by its Chairman, former head of the World Bank, Eugene Black. Interestingly, Black’s father had been Chairman of the Federal Reserve in 1933.

Within two years of assuming his position as New York State Bank Superintendent, Dentzer was named Chairman and CEO of the newly formed Depository Trust Corp. (DTC), a post he held for the next twenty-two years, i.e., through the entire process of dematerialization.”

Wow. (I quoted extensively above because this is all important information directly relating to Webb’s claims.)

One last anecdote from Webb:

“In 1923, so 10 years before the banks closed in Cleveland, they build the biggest bank vault in the world with the biggest hinge ever built on a door. There are machine gun turrets over the truck entry into the building in 1923. What were they preparing for?

So in 1933, they create the argument that the public is hoarding gold and hurting the economy, so you better turn it all over to us. And it’s criminalized with harsh penalties. Harsh penalties. And the gold is to be turned over to the Federal Reserve.”

Food for thought.

"I believe that you have to have a center outside of yourself,

that if you are entirely focused on yourself,

it’s a kind of insanity."

“nobody GOES to dennys... they END UP there”

Coincidentally - no joke - I ate at a Denny's yesterday with someone (don't ask) for the first time in forever. We each had coffee, he had french toast, I had a sandwich. That was it. It was not good. $56 out the door.

But I believe

I am gone down into that well

so dark in which, said

Heraclitus, the truth is hidden.

Robert Chambers, “THE DEMOISELLE D’YS”3

Grant’s comments here reminded me of a passage by Elias Canetti: “A man identifies himself with the unit of his money ; doubt cast on it offends him and, if it is shattered, his self-confidence is shaken. He feels slighted and humiliated by the lowering of the value of his monetary unit and, if this process is accelerated and inflation occurs, it is men who are depreciated until they find themselves in formations which can only be equated with flight-crowds. The more people lose, the more united are they in their fate. What appears as panic in the few who are fortunate enough to be able to save something for themselves, turns into mass flight for all those others who have become equals by being deprived of their money.”

Since 2007, I’ve used a cash (i.e., non-margin) brokerage account to try to avoid what Webb warns about, but according to Webb no one is safe (unless you’re Jamie Dimon.)

I’m not sure what it means but it struck me in some way.

I’ve read Webb’s book. Listened to some of his interviews. He’s obviously got some interesting ideas. In all likelihood he’s correct about some things, and incorrect about others. The real question is, does it matter.

As a basic premise, his basis for the “great taking” relies heavily on what happened with Lehman. But that was more than a decade ago and, it’s never happened again, individual retail account holders eventually got their money and equity investments returned. So as a basis for the ‘great taking’ and projecting forward he is factually incorrect.

Second, his premise is essentially based on the singular occurrence that your broker goes belly up. And once your broker is insolvent, your beneficial interest stands near the end of the line. And that instead of what ‘should’ happen (and has been the historical norm), that your equity interests are transferred to a different broker, and your cash accounts are insured by the SIPC, your equity interests (and maybe your cash) are siezed to pay secured creditors.

However, outside of Lehman, he cannot point to a single time this has occurred. And in actuality, it did not happen with Lehman, other than as a temporary measure. Inconvenient? Yes. Deveststing? No. Although it did take longer, an analogy can be drawn to what occurs when a bank fails. The FDIC comes in, and a period of time goes by where bank clients cannot access their accounts. This is not new, yet he treats it as a revelation.

But even if one casts all the fact in a light most favorable to his position, then it all essentially comes down to the health of your broker. Is Fidelity going belly up? Robinhood on the verge of a Chapter 7? Ameritrade filing a reorganizing 11 tomorrow? If not, then his entire premise is destroyed because it takes the destruction of a broker to trigger everything he claims will follow.

In the end, for me, after reading his book and listening to multiple hours of interviews I concluded that I had wasted my time. He could be correct. He could be incorrect. But in the I learned nothing that my dad hadn’t taught me decades ago.

. Don’t put all your eggs in one basket. Multiple brokers. Multiple banks. A CU for good measure. Gold at home. Gold vaulted. Silver at home. Silver vaulted. Cash at your brokers. Cash in banks. Cash at home. Cash and gold buried on your kids 40 acres.

Just like investing, actual diversification is critical. If he’s proven correct I’ll still have resources available. If he’s incorrect (which is where I come out) then I’m paying for insurance I don’t need. Which is exactly what we hope for when we buy insurance.

Favorite Agatha Christie quote: "where large sums of money are concerned, it is advisable to trust nobody"