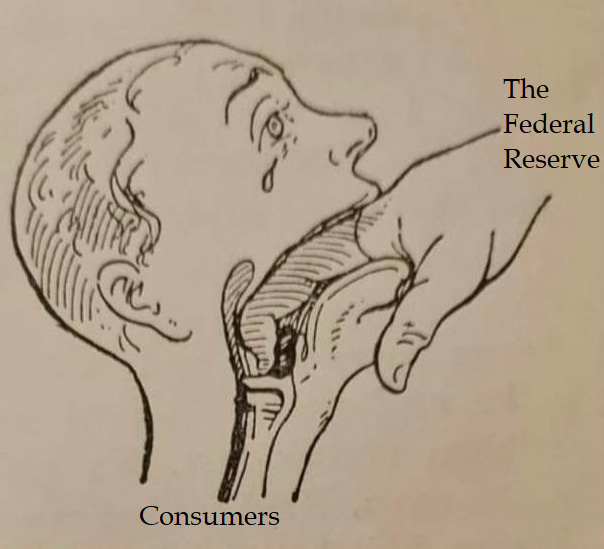

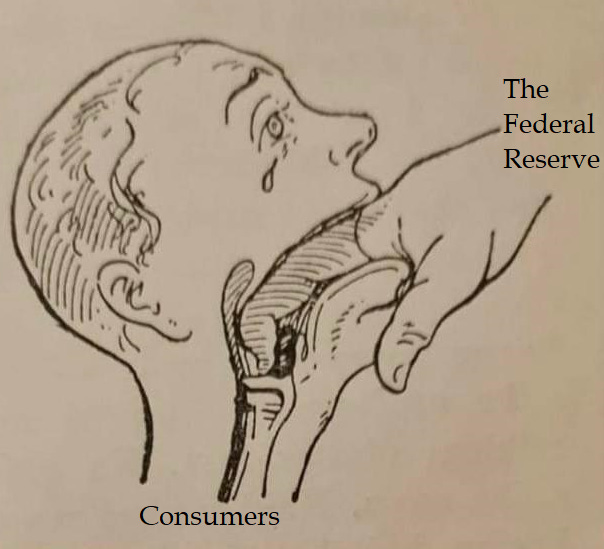

The inflation number is not good.

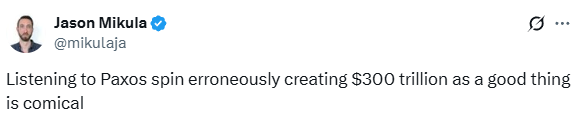

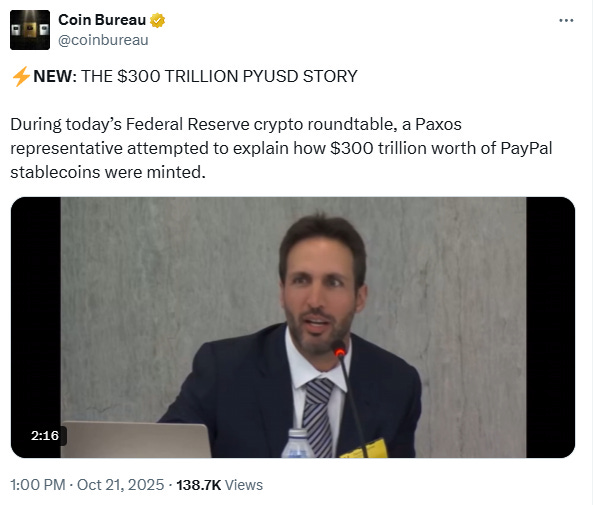

Finding a new market for exit liquidity

“Dives sum, si non reddo eis quibus debeo.”

(I am a rich man as long as I don’t pay my creditors)

Titus Maccius Plautus

Happy Halloween!

Nvidia grew over $4 trillion in 4 years.

October 29, 2025:

A couple of $4 Trillion Dollar Babies:

Jim Grant talking about short-seller Nate Koppikar of Orso Partners:

“You cannot be afraid of new technologies. I think that this tenet passed Warren Buffett by. As he is the greatest investor of all time, I think it’s important to recognize that if he were not afraid of product cycles and obsolescence, he would have made much more these last few years than he did. Now I know we shouldn’t criticize someone of his unbelievable prowess, but we must also recognize that it was wrong, just wrong, not to include technology stocks in the portfolio. Wireless plays such as Qualcomm (QCOM) and optical plays such as JDS Uniphase (JDSU), which stands for Just Don’t Sell Us, are simply creating too much wealth to ignore.”

Jim Cramer, January 2000

“Gold, unlike all other commodities, is a currency. And the major thrust in the demand for gold is not for jewelry. It’s not for anything other than an escape from what is perceived to be a fiat money system, paper money, that seems to be deteriorating.”

Gary Bohm reminded me of this:

“Worldwide speculation pushed up the price of gold by more than $3 today to a record $72.30 an ounce on the open market.

Dealers on the bullion market here reported that trading was frantic. “Orders are flow was frantic. “Orders are flowing in from all directions, creating chaos on the floor,” a gold dealer, Johnson Mathey said.”

SUBCOMMITTEE OF THE COMMITTEE ON BANKING AND CURRENCY, HOUSE OF REPRESENTATIVES, Washington, D. C., Thursday, December 19, 1912

The original John Pierpont Morgan Sr. talks about money vs. credit.

Mr. UNTERMYER. I want to ask you a few questions bearing on the subject that you have touched upon this morning, as to the control of money.

Mr. MORGAN. Yes.

Mr. UNTERMYER. The control of credit involves a control of money, does it not?

Mr. MORGAN. A control of credit ? No.

Mr. UNTERMYER. You do not think so ?

Mr. MORGAN. What I call money is the basis of banking.

Mr. UNTERMYER. But the basis of banking is credit, is it not ?Mr. MORGAN. Not always. That is an evidence of banking, but it is not the money itself . Money is gold, and nothing else.

Mr. UNTERMYER. Do you not know that the basis of banking all over the world is credit rather than gold?

Mr. MORGAN. It is the basis of credit, but it is not the basis of money.

Mr. UNTERMYER. I say, the basis of all banking is credit, is it not, and not money?

Mr. MORGAN. No; I do not think so .

This was all Monday, October 27, the day before the Fed Meeting began.

Isn’t this yield curve control?

Powell on Fed Day

“Our obligation is to ensure that a one-time increase in the price level does not become an ongoing inflation problem.”

Powell January 2021:

Since January 2021, using their models, CORE CPI is up 22.2%. Powell is either a liar or a fool.

This FT headline blew my mind.

“The inevitable is certain, but not necessarily punctual.”

Jim Grant, quoting some unknown person

Greg Weldon

“The point here is that the inflation number is not good. I mean, they’re talking about it being soft because the monthly rate was up only 0.3%. Well, 0.3% is 3.6% annualized…That’s not soft, 3.6%.”

“Let’s look at food. Food away from home is 3.7%. Full service meals away from home, aka restaurants, 4.2%. That’s more than double the Fed’s target range. Food and employee venues 3.8%. Mobile food trucks and vending machines 6.3% year-over-year. Other food away from home 5.3%. This is not soft. This is hard. This is choking.”

“We’re ‘yes, but…’ people in a ‘gee whiz’ world. People say we’re always bearish - that’s not actually true - but we are almost invariably skeptical…These markets run over the skeptical mind.”

Joseph Wang

“Central banks in general today are much more powerful than they were in the past, and when you look at the political issues today as a society, one of the most pressing ones is home ownership, right? A whole bunch of people can’t afford homes because home prices have gone up, in part because mortgage rates are low, and of course it’s wealth inequality. People who own financial assets they’re doing pretty well. We have this K-shaped economy.

So some of the most important distributional things in our society are basically determined by a a small group of people sitting at the central bank. If you believe that we should have a democratic society, it seems to me that it makes sense for the public to have some say in matters that have huge distributional impacts on the society. You can make the argument that because central banks today are much more powerful than the past, they have to be less independent, or you could pare them down, maybe separate regulatory power out, maybe make them single mandate, inflation only, and so forth. So I think you can make a good argument that the central bank is too powerful to not have any kind of democratic say.”

“I don’t fight the Fed. I’ve made my life throwing hard jabs and left hooks at the Fed, and occasional right at the Fed, and they never hit back, except sometimes I feel the blow.”

Steve Diggle

“Everyone assumes that they’re going to be able to get out of what they want, when they want, at the price that, you know, they may not like, but it’s going to be acceptable. There’s no guarantee for that. When markets really become dysfunctional, they become illiquid, and you get discontinuities. Unless you already have that position in your book, unless you have that put option, or you have that offsetting position, there’s no guarantee that markets will be able to give it to you just because you’ve changed your mind.”

“The number of participants - from retail to passive - who would be trying to sell in a severe downturn could just overwhelm the markets.”

“You’re always at risk of sounding like, you know, the old man. I am an old man…in a bull market you want someone who’s fearless…So the person you probably want to be running in a bull market is a 23-years old, and a man, because men take more stupid risks than women…the number of bull market geniuses out there right now is frightening, but none of them are particularly interested in what you and I have to say about risk management, because look at their returns over the last six months or 12 months compared to mine. They’re like, “Ah, this is just some stupid old man who doesn’t get the world’s changed.” And I say, “Well, yeah, the world’s changed, but humans haven’t.” At some point, someone’s got to be wanting to take a profit, and when everyone starts queuing up, there may not be people on the other side to get you out of your investment.”

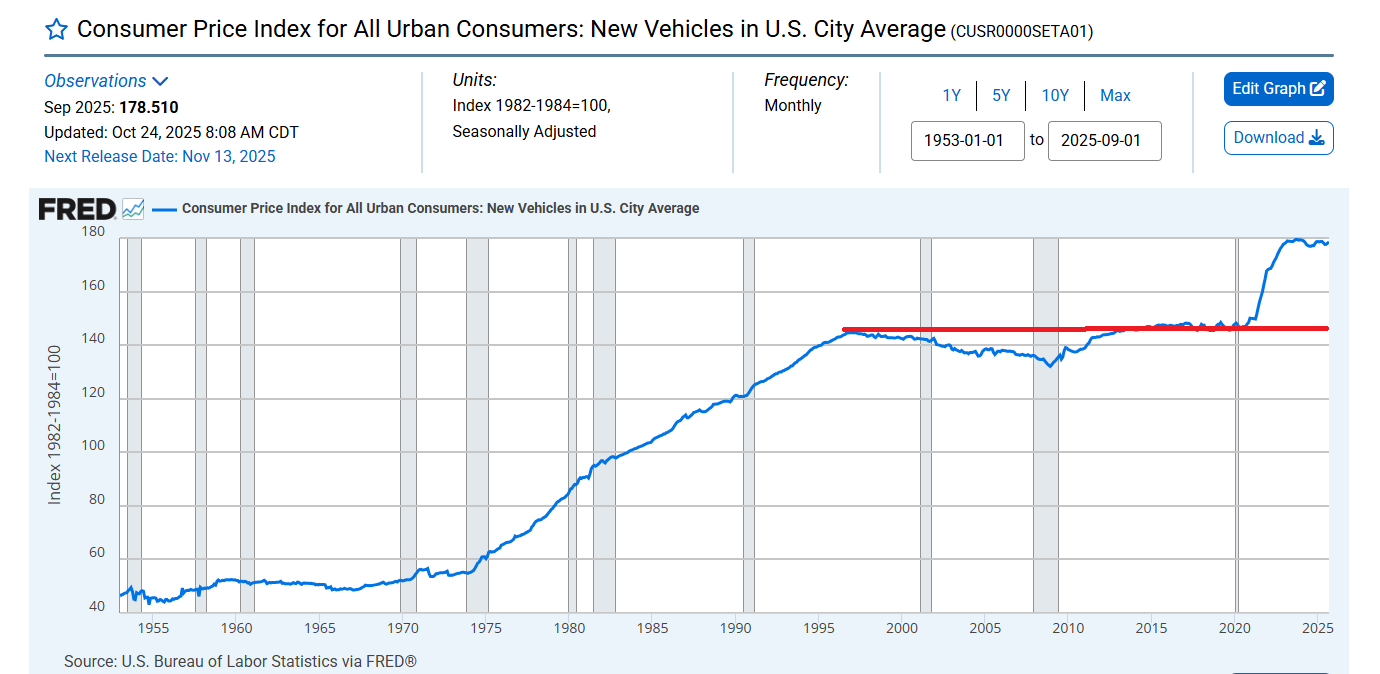

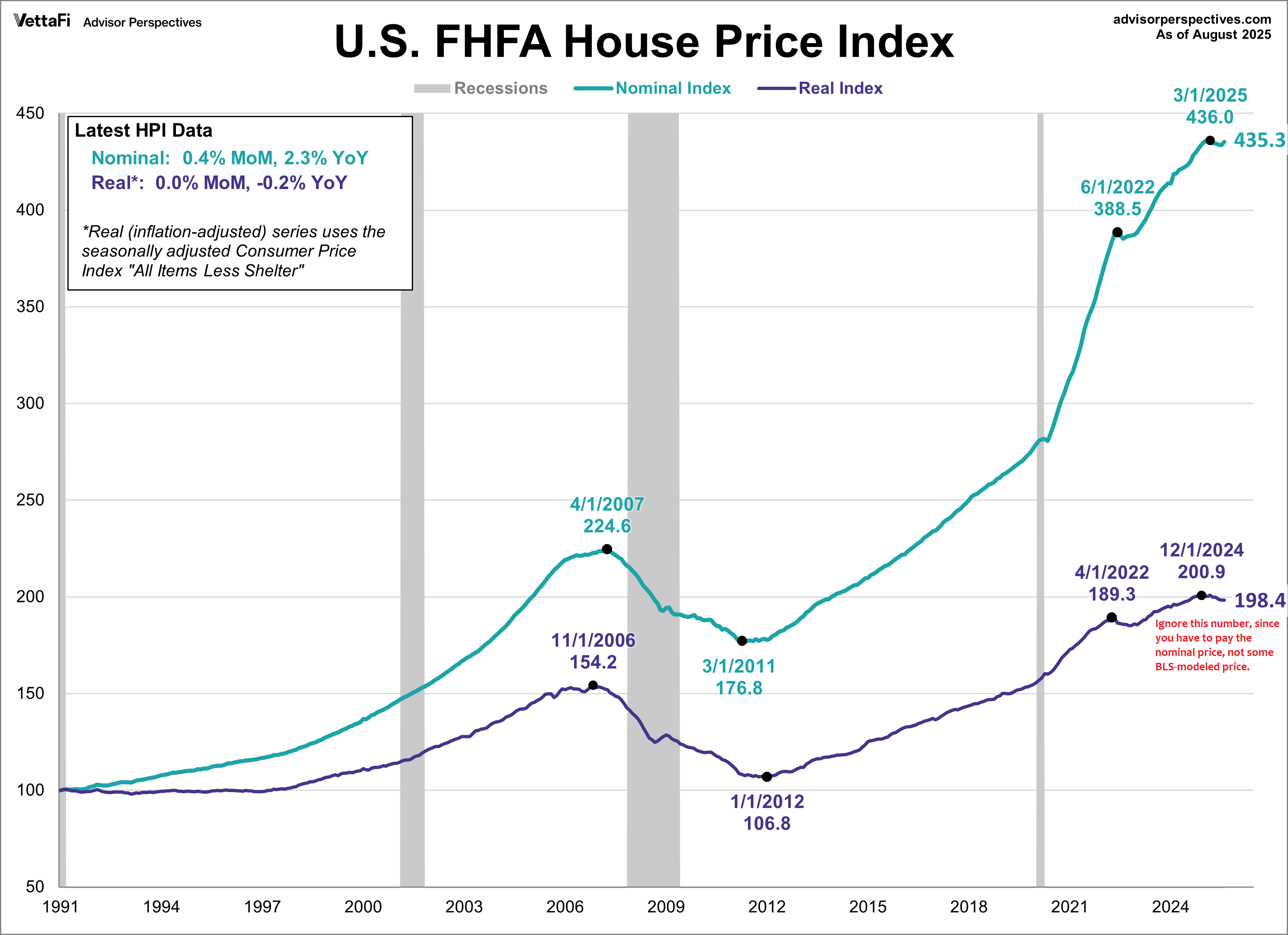

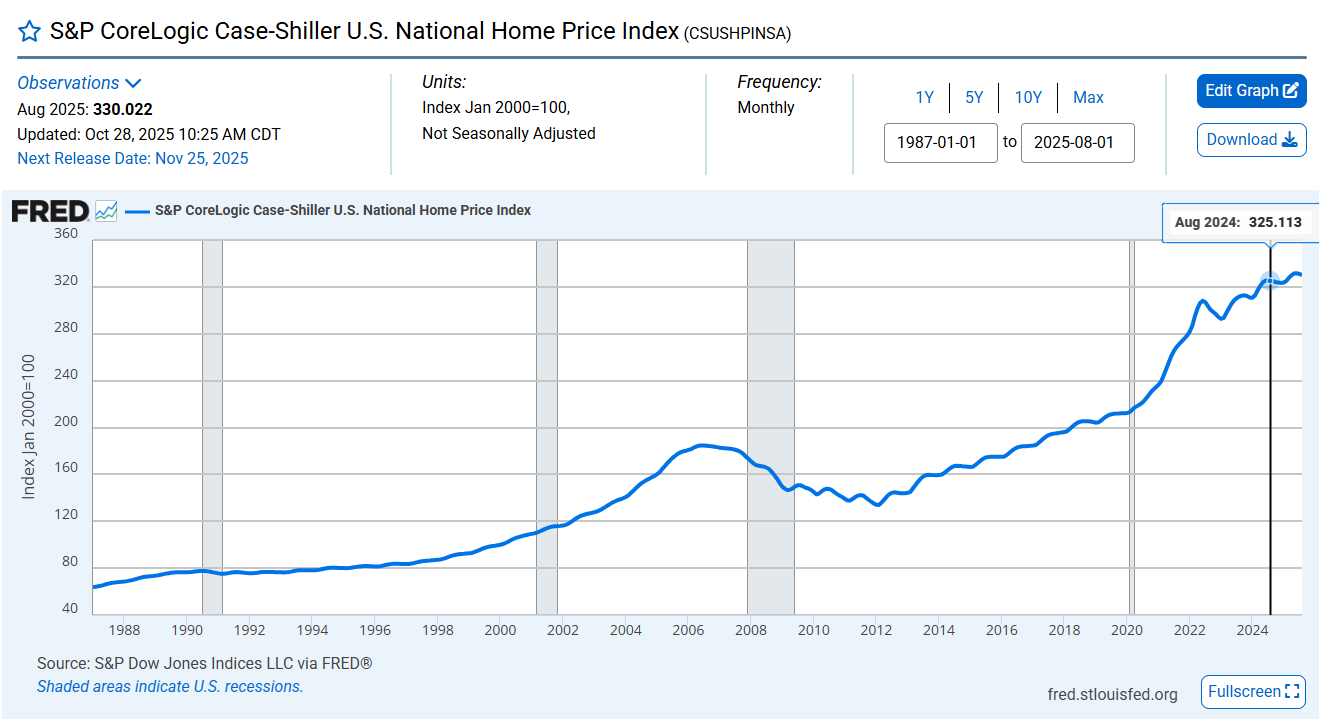

Just a reminder that from 1995 to 2020 (25 years) new car prices - according to the BLS CPI model - did not go up at all.

“If the invention of interest was the greatest invention in finance back five millennia ago, then negative rates are probably the dumbest idea in the entire history of finance and we’ve just been living through it.” - Edward Chancellor, 2022

Why is this the case if everything is awesome?

Is this true? I don’t know.

SNAP participation and average monthly benefit per person:

May 2022: 41 million, $228

May 2023: 42 million, $174

May 2024: 41.7 million, $185

May 2025: 42 million, $188

For perspective (thanks to TARP), here’s the 2008 Failed Bankster Bonuses:

The Cake-Shaped Economy:

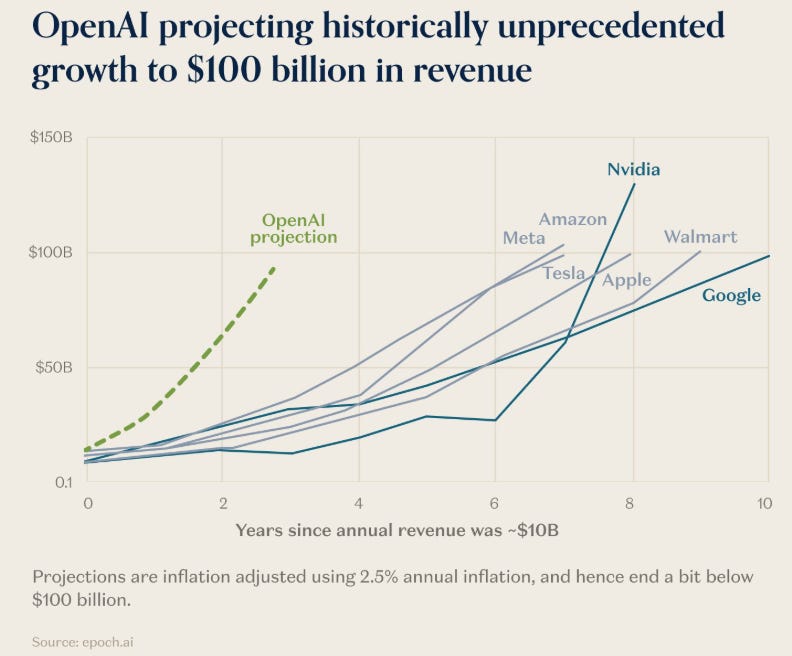

Just saving this for future historians: looks like OpenAI’s revenue projections are for $100 billion by 2027.

“What is really going on, is that the big tech companies are under massive profit pressure as they spend on LLM AI, a monopoly rent they see as necessary to preserve their monopoly positions. There are many ways they can hide the immediate effect of lossmaking LLM investment on profits, most notably by depreciating the chips they buy over 6 years rather than the 30 months or so of their useful lifetime, or by offering cloud services for equity in an LLM provider and booking those cloud services as revenue (as Microsoft has done with open AI). But, as anyone who has looked at examples of this type of creative accounting in the past, especially the slow depreciation, inevitably, over time, you have to pay the piper. And if your revenues and profits from direct LLM AI investment, or on chipsets fall short, as they are clearly doing, then you have to find another way. And that way is cutting jobs.

So what these companies are doing is cutting workers, from interns to juniors to programmers to middle management, getting an LLM to run a first pass on their workload, and then setting up a base of much cheaper workers offshore, to clean up and complete the mess that the LLMs have created. As ‘offshoring’ is a dirty word in the current Trump administration, the companies are concealing that bit in ‘contracts for services’ which don’t legally have to specify where the work is being done.

…as soon as LLMs stop getting better with training, (and they have stopped getting better), then the big companies no longer gain economic rent (the benefits of maintaining monopoly power) from investing in them, especially in training. So, even though LLM AI has never been very good, and won’t ever be very good, it’s good enough for Google, Microsoft and Amazon, and for other monopolies and quasi monopolies that can afford to cut costs at the expense of quality, that need to divert traffic onto their own platforms, and that are happy to cheapen content to cut costs and drown out the competition. Think “Google Gemini” versus “ChatGPT Atlas”...no competition, they’re both horrendous.”

“Using ChatGPT to write an essay reduces the cognitive engagement and intellectual effort required to transform information into knowledge, according to a study. The study also showed that 83% of AI users were unable to remember a passage they had just written for an essay.”

Subprime lender PrimaLend Capital Partners files for bankruptcy protection

Jeff Snider: “PrimaLend becomes the latest roach. “You’re going to lend hundreds of millions of dollars to a company and not open the hood to see how it looks inside? Is money that free?” Clarke asked. Yep, that’s exactly what happened for years. Everyone assumed Jay Powell knew what we was talking about, which is why when he said the labor market was solid they all believed him - until two days later it wasn’t and then Powell suddenly changed his tune. So all these ABS and private credit lenders lent to anybody they could while demanding collateral they didn’t bother to really nail down simply because they believed they’d never need it. Now everything is coming out: “Until we get intellectually honest about the risks that we face and the need for more robust due diligence, we are vulnerable.” And that’s what is happening right now all over the credit markets which is why even central bankers are spooked (see: BoE). Jamie Dimon doesn’t know sh&% about inflation, but give him cockroach credit here.”

Bankrupt Telecom Business Accused Of Fraud In Receivables Financing

Jeff Snider: “$500mm evaporated. This one in the telecom space is accused of - get this - faking invoice collateral. This is starting to appear endemic. At some point the big boys who have been financing all these redistribution finance schemes thinking they were all protected have to just yank everything from the market. Credit crunch and then some. And it won’t just be for subprime. Man, collateral is the last thing that you want to mess with. But everyone seems to have done it.”

“The 2019 restart to QE - the course we are on now - was one of the dumbest and most obvious examples of what the Federal Reserve really is. Fed buys Treasury notes and bonds, then its QE money printing super-accommodation. Fed buys only bills, it’s just some technical repo finetuning related to the systemic level of reserves. This is not a serious enterprise.

Stocks didn’t care, it was an excuse to buy so shares soared anyway. After the repo mess in Sept ‘19, Powell wanted to find a way to increase bank reserves without it seeming to be a QE so that he could sell the public this repo mess was nothing more than just a technical matter related to the systemic level of bank reserves, and that the Fed was doing nothing more than fine tuning a few things. That is where not-QE QE came from. Policymakers decided that if they only bought Treasury bills, and not notes or bonds, somehow that would be a not-QE.

In this one stupid episode you can really see what the Fed’s main tool is, or what the Fed would like to believe it is: psychology. To believe what Jay Powell was selling meant to also believe the very same act of buying Treasuries to create bank reserves ended up with different results solely because the Fed intended them to be different. It was pitifully stupid, yet the mainstream media swallowed it hook, line, and sinker. And so to this day the vast majority of the public has no real idea what happened.”

From Investment to Savings: When Finance Feeds on Itself

With nearly $2 trillion deployed, private equity funds must generate distributions for their LPs. According to Zito’s estimate, they should be looking to return $1 trillion over the next year and are $850 billion short of that goal. Funding distributions through a form of private credit-financed dividend recapitalizations is an increasingly attractive option.

As a result, private equity firms have gotten more creative in what they will lend against and how they structure such loans. That has meant an intentional foray into asset-backed lending. Banks and other institutional investors have historically financed debt related to education, car loans, equipment, and credit cards. Private capital is looking at assets like music royalties, movie rights, and hard assets like airplanes and GPU clusters. According to an April Bloomberg report, asset-backed deals collateralized by “unusual collateral” have risen considerably in the post-pandemic era…

In May, Blackstone, alongside several other private funds, originated a $12 billion loan to CoreWeave. CoreWeave launched in 2017 and began amassing Nvidia Graphical Processing Units (GPUs) ahead of the boom in artificial intelligence (AI) investments. While CoreWeave’s original business plan focused on mining cryptocurrency, they shifted their model in 2020 to focus on the burgeoning AI space. The company claims to be the largest private operator of Nvidia GPU clusters in the United States, with over forty-five thousand chips.13 The new capital will go toward buying thousands more.

Unlike a traditional loan in which the debt is serviced from company cash flows, the Blackstone loan moves the chips into a “metaphorical lockbox, housing all of CoreWeave’s AI chips. Any revenue the company generates from clients using those chips, the most advanced of which cost tens of thousands of dollars each, goes first toward paying its lenders. Any excess cash after making the loan payment flows to the company as net revenue.” The loan itself is collateralized by the chips and not all company assets…

A dystopian view might be a world where there are no savings-funded investments; rather, savers purchase insurance products like annuities. Those insurance products are fed by the debt created from savers’ levered consumption. While not inherently calamitous, this transformation carries risks for economic vitality. By favoring debt, collateral-based lending, and guaranteed returns, the system may direct less capital to productive equity investments. In this debt-centric paradigm, real economic growth plays a shrinking role in justifying ever-larger pools of investment capital. The upshot is a finance industry that thrives, not on discovering new opportunities for value creation, but on feeding its own self-perpetuating demand for yield—a modern-day ouroboros that may gradually erode the dynamism of the real economy.

How Affluent Investors Are Using Options Math to Borrow on the Cheap

In a box spread, two sets of options with matching strike prices — call spreads and put spreads — create predictable cash flows that closely mimic fixed income. By selling one, an investor receives a lump sum of cash upfront, and agrees to pay a preset amount at maturity. It’s a strategy that behaves predictably — until markets act up.

The gap between what the investor receives upfront and repays at maturity determines the effective interest rate — now roughly 5 to 20 basis points above comparable Treasury yields, according to Vest Financial, a $54 billion derivatives-based asset manager that officially launched its synthetic‑borrow platform this week.

“We have taken the financing that’s embedded in the option market, which is institutionally priced, and we’ve delivered it” to the retail market, said Karan Sood, Vest’s chief executive officer…

“It’s a low-interest-rate loan against your own assets with some interesting bells and whistles,” said Chris Whitaker, chief wealth manager at Apriem. One of his clients recently used the strategy to finance a boat…

But the math only works if the market does. If stocks fall, so does the value of the collateral. That triggers margin calls — the same mechanism that has unraveled countless trades in past downturns. If the client can’t post more collateral, their portfolio gets liquidated. The promise of frictionless money becomes forced selling.

Private loan credit ratings may be ‘systematically’ inflated, warns BIS

“Credit ratings on private loans held by US insurers may have been systematically inflated, the Bank for International Settlements has warned in a new paper on the growing risk of “fire sales” during periods of financial turmoil.”

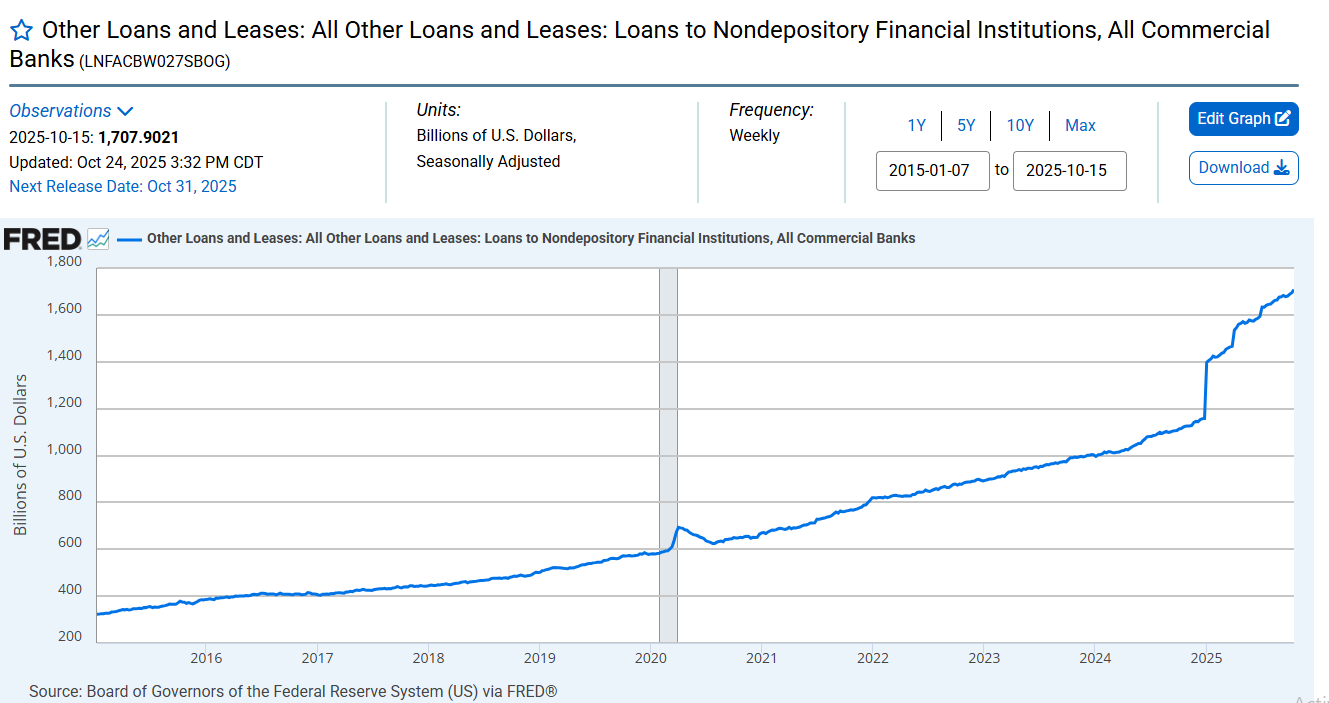

From Grant’s:

“U.S. bank loans to non-depository financial institutions (NDFI), which include private equity and direct lending outfits, reached $1.2 trillion as of June 30, a Tuesday report from Moody’s Ratings finds, equivalent to 10.4% of their total loan books. A decade ago, that share stood at 3.6%. “Aggressive growth and competition could weaken [bank] underwriting standards and elevate credit risk,” the rating agency warns.”

Moody’s, an outfit that generally shows up at a fire after the building has burned down…

“Is NBFI the new Alt-A? Banks’ tone reminiscent of 2007”

“In short: it is virtually certain that the private credit blow up will begin in the Non-Depository Financial Institutions category, largely due to its opacity and the fact that nobody appears to have done much if any due diligence where all this money is going. Still, at the macro level, the private credit space is hardly a time bomb that will go off tomorrow. In fact, ask yourself this: why is Jamie Dimon almost eager to start a panic selloff in the private credit space? The question has a simple answer: every time there is a banking crisis, JPMorgan always, always ends up picking up the best assets while stuffing taxpayers with the toxic sludge courtesy of the FDIC: it happened in 2008, it happened most recently in 2023.”

“Private equity has spent decades tapping new sources of cash. First, it was junk bonds, then pensions, then endowments, then sovereign wealth funds,” he said.

“Then they entered the era of circularity with private credit. Every move they’ve made has been to further centralize risk with existing investors, rather than syndicating risk into the system.”

After tapping “every major institution on the planet for your equity and debt needs, there’s only one well left: the retail market,” he said.

[Nate] Koppikar noted that this approach is often described as “democratizing access.” But, he said, “let’s call this what it is. The institutional well has run dry and they need a new source of flows. This isn’t about democratizing returns; it’s about finding a new market for exit liquidity.”

The industry calls the new retail class the “mass affluent,” which it defines as people with as little as $100,000 in liquid assets. These investors “should probably be in low-cost index funds, not opaque, illiquid alternatives,” according to Koppikar.

“The $81.61 million CMBS loan against the 804-unit Muse apartment property in Dallas and the 197-unit Eden Pointe in Houston was reclassified as being more than 30 days late this month. The loan was originated just two years ago.” - Trepp

“Lenders right now - what we’re seeing is that they’re doing everything possible to prevent some transaction event that their internal credit committee or the regulators look at and say, “Okay, you got to write this down.” If they foreclose, they have to. If you went for a receiver, you have to. They’re trying to do things, play the game of Twister to to make the loans still look good as long as they can.”

Workout specialist Norman Radow

“Supply creates its own demand. There is no latent demand for five-times levered ETFs from thoughtful individuals who are interested in actually executing a well thought out investment policy. There’s a ton of demand for hard eights at a craps table, right? It’s not a good bet, but we facilitate it because it transfers more money into the casino’s pockets on average. And that’s really the motivation for Graniteshares or candidly almost anyone, myself somewhat included, in the industry. I want to get paid, right?”

”The reliance on the Internet for smart bed products from Eight Sleep resulted in people being awoken by beds locked into inclined positions and sweltering temperatures.”

“Fiat money has no place to go but gold...Gold is the canary in the coal mine. It signals problems with respect to currency markets. Central banks should pay attention to it.”

Sorry Kids!

“Barack Obama got elected - people forget this, oh, he ran he ran as a moderate - that’s a bunch of horseshit. He didn’t run as a moderate. He ran as a populist in the middle of the financial crisis and he got in and he converted hope and change into more of the same, siding with Wall Street…I don’t want to rehash all that, but the point is that I think the reason why the 2009 and 2010 moment was so enduringly pivotal to what we’re living through now is because people’s hopes were raised, and then they were destroyed.”

“In the HUD meeting, which was FHA, VA and all that, they basically straight out told us that in 2026, 2027, foreclosure activity is going to spike high. They said most of it’s going to be driven from the loans originated from 2022 to 2024.”

“If Larry Fink and the boys decide it’s game over for Bitcoin - if they make that call - you’re done. I’m positive. And what you’re counting on is that those guys decide not to destroy it. And this is the same community that were sort of hyper-libertarian, saying, you know, those guys can’t touch us. Now they’re saying those guys won’t touch us. That’s a different story.”

(Note: If you vehemently disagree with Dave’s quote above, please do not reply to me. I don’t care if you agree or not, I just found it to be an interesting comment. Believe me, the twitter bitcoin bot-people already yelled at me. - rh)

Tom: You know what they say about wisdom, Kath?

Kath: No.

Tom: It’s knowing what to overlook.

“When you observe an extreme outlier, you should usually vastly reduce your credence in the model with respect to which the event counts as an outlier.”

From Jim Grant’s newest book, “Friends Until the End: Edmund Burke and Charles Fox in the Age of Revolution”:

Edmund “Burke observed that Britain was far from the first nation to conquer India, but the Arabs, Tartars, and Persians who had preceded the English were “very soon abated of their ferocity, because they made the conquered country their own.”

The English had no such designs. “Our conquest there, after twenty years, is as crude as it was the first day,” Burke said.”

The natives scarcely know what it is to see the grey head of an Englishman. Young men (boys almost) govern there, without society, and without sympathy with the natives. They have no more social habits with the people, than if they still resided in England; nor indeed any species of intercourse but that which is necessary to making a sudden fortune, with a view to a remote settlement.

Animated with all the avarice of age, and all the impetuosity of youth, they roll in one after another; wave after wave; and there is nothing before the natives but an endless, hopeless prospect of new flights of birds of prey and passage, with appetites continually renewing for a food that is continually wasting.

A passage from the 1807 book, The Life of the Right Honorable Charles James Fox, still applicable today:

Currencies untethered from precious metals—which are inherently limited in supply—paved the way for free-spending governments to indulge in redistributive policies. This much, at least, was consistent with the writings of Hayek’s teacher, Ludwig von Mises, who valued gold for “its ability to act as a brake on the tendency of democratic states to spend beyond their means.”

Suzanne Schneider

“Nothing puts the fiat-money era in starker relief than the fact that it took the US 222 years to borrow what the efforts of Presidents Biden and Trump achieved in not quite 8 years. So we can be equal opportunity in blaming different parties for the history of recklessness here.”

William Green, quoting Jim Grant

A couple related tweets I found amusing:

“If the phenomenon can create physiological constructs, if it can make something real, and then make it not real the next second, then ufology as a field may not really exist.”

”AI Now Claiming to Be God”

“Instead of going on long pilgrimages or driving to the closest place of worship, users can simply turn to AI chatbots to seek spiritual guidance.”

I felt honored when Ben Hunt asked me a while back to write something for a new project called Panoptica, so this is what I wrote:

If anyone has too much Bitcoin and would like to send me some, I’m willing to help.

Thank you for your attention to this matter: bc1qkvxy0f8tnxnjddwtyg3jshwgck4e9haw8e8kf9

I like that quote. The rest of the interview is very far out.

The cake shaped economy meme is the best!

Loved your ‘Ben Hunt’ essay. I’m just a few years older than you, but my experiences were much the same. What I remember most is that during summer vacation (from school) Mom fed us breakfast after Dad went to work. And then kicked us out. We could re-enter the house if one of three conditions were met. Bleeding. Broken bone. Needed to poop. Otherwise we had to figure it out until Dad got home from work.

It was a wonderful life.