"The Lazy Tax"

"A parasite on a parasite."

"Energy availability determines where GDP growth is going to be."

S&P 500 Snapshot: Index Closes Above 5000 for First Time Ever

Just four years ago, the $SPX touched 2191 during the Covid panic.

Here’s how the S&P 500 has done since the first rate hike on March 17, 2022:

Seems like the market is mocking Jay Powell.

Here’s since history began on March 9, 2009:

Janet Yellen strikes again

Again, I’d love see her (or Krugman, Wolfers et al.) wander around a supermarket and say the goofy things she does. Yellen’s comments lately are a rich source of material.

"You’ve got a Treasury in the form of Janet Yellen who has one single job this year. It’s not about funding the US government, it’s about getting Joe Biden elected"

- Julian Brigden with Grant Williams

"Capitalism without bankruptcy is like Christianity without hell."

Frank Borman

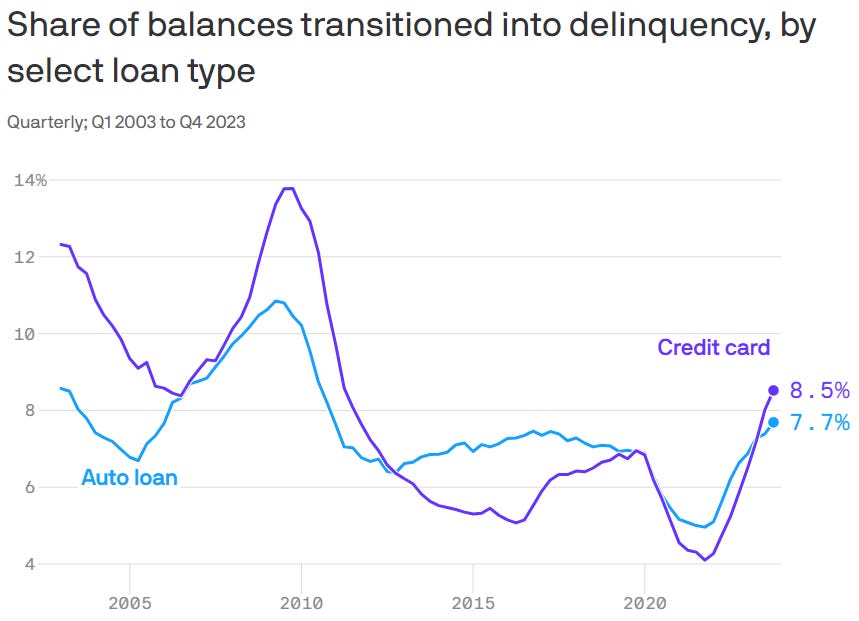

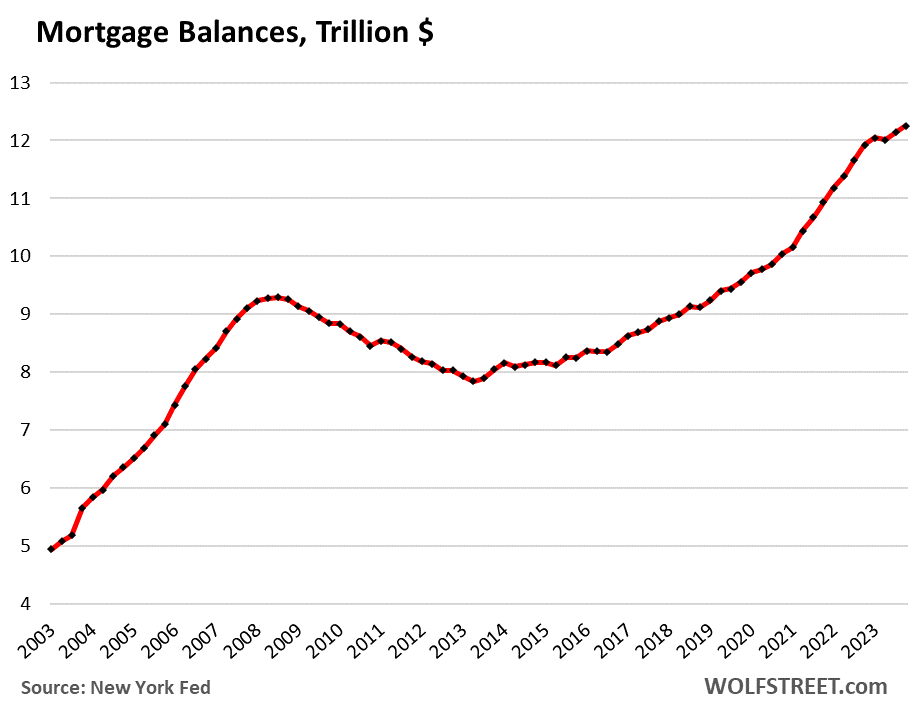

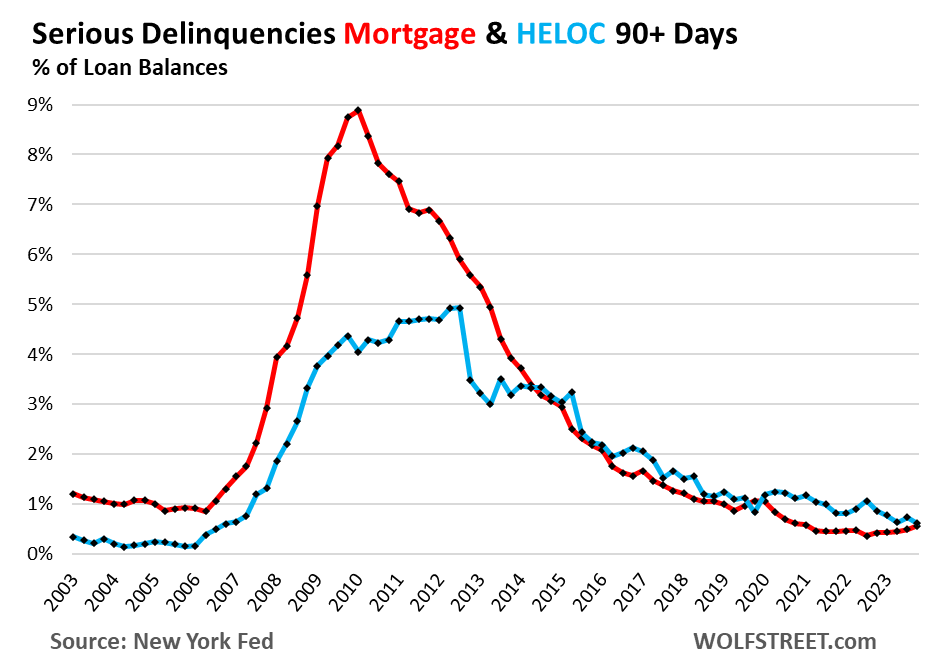

Tuesday Headlines from the New York Fed

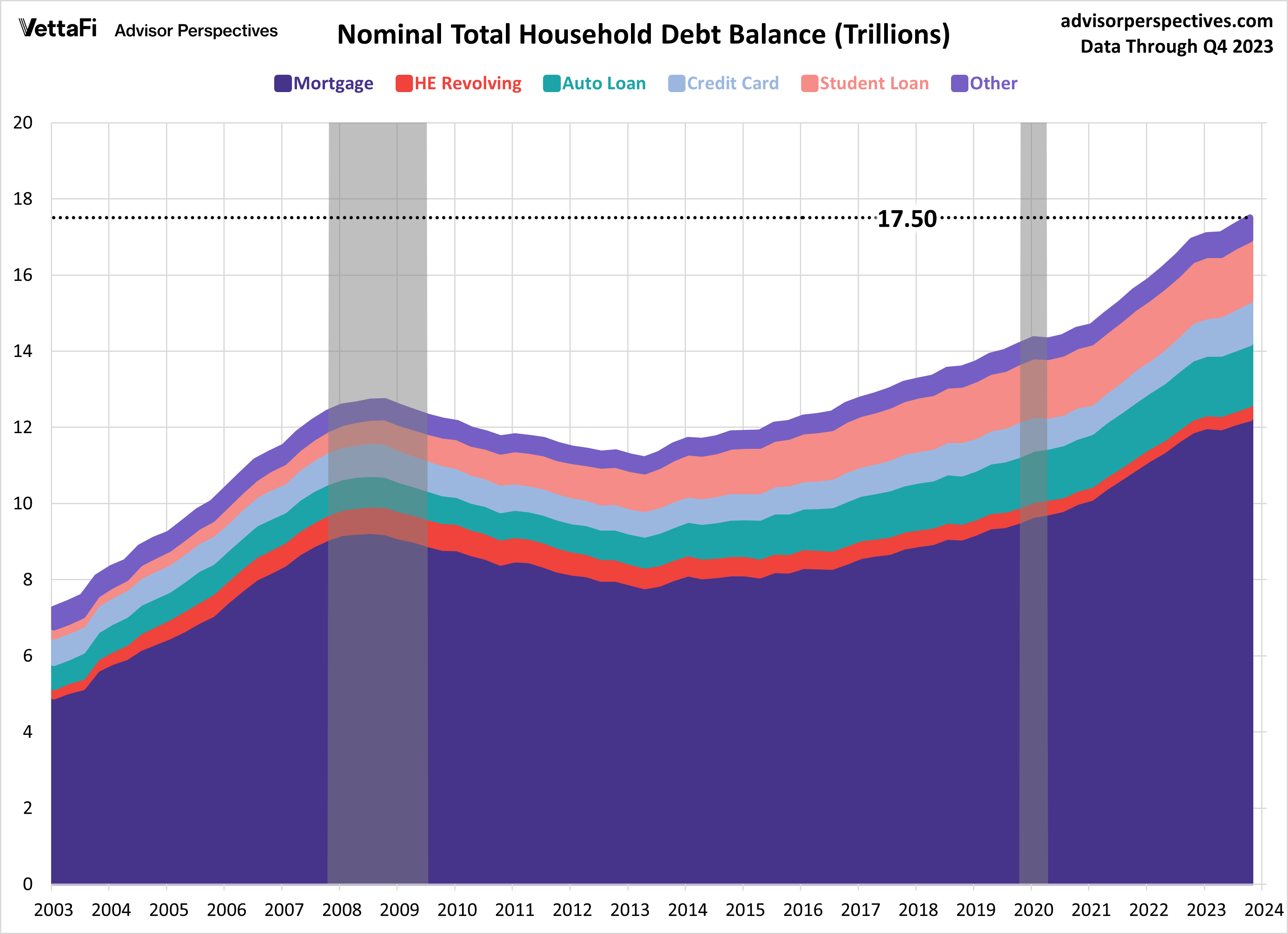

CREDIT CARD BALANCES UP $50 BLN TO $1.13 TRILLION IN 4Q 2023.

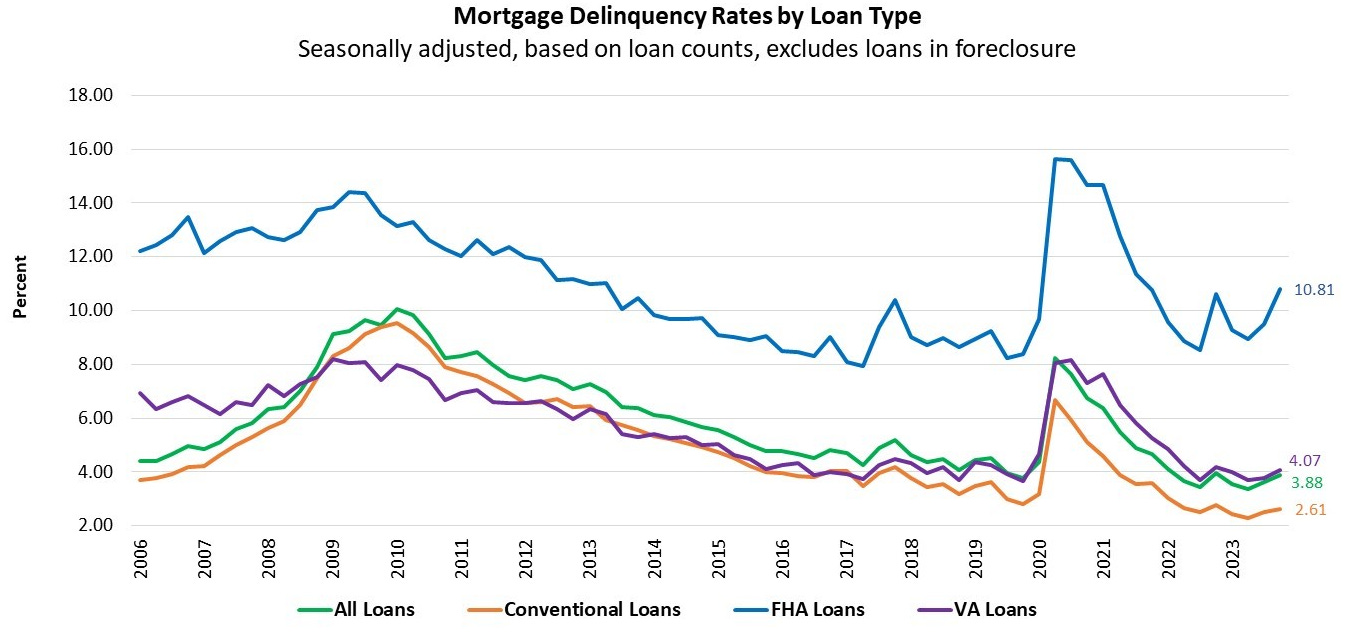

THE DELINQUENCY TRANSITION RATE FOR MORTGAGES ARE UP, BUT ARE STILL HISTORICALLY LOW.

STUDENT LOANS LITTLE CHANGED IN 4Q 2023 AT $1.6 TRILLION.

MORTGAGE BALANCES UP $112 BLN IN 4Q 2023 TO $12.25 TRILLION.

DELINQUENCY TRANSITION RATES ARE UP FOR ALL BORROWING TYPES EXCEPT STUDENT LOANS.

TOTAL HOUSEHOLD DEBT UP $212 BLN TO $17.5 TRILLION IN FOURTH QUARTER OF 2023.

DELIQUENCY RATES ROSE IN Q4 2023, BUT REMAIN BELOW PRE-PANDEMIC LEVEL.

3.1% OF DEBT WAS IN SOME TYPE OF DELINQUENCY DURING 4Q 2023.

As Melody Wright often points out, delinquencies should be low after years of government programs designed explicitly to prevent them (some of which have now expired.)

“Household debt rose by $212 billion (1.23%) to $17.50 trillion in Q4 2023. All debt categories increased from the previous quarter for a second straight quarter.”

“Net profit at the world’s biggest packaging business, Amcor, fell by almost 60 per cent in the first half of the financial year, leading to the company axeing 2000 jobs, about five per cent of its workforce, as it seeks to reduce costs.”

Volumes dropped by a record-breaking ten per cent

I’m noticing the Anti-McDonald’s sentiment growing…

The last two times I went to mcdonalds starving and lazy, I looked at the menu, and just left without buying anything. I just don't bother any more. I can get 5-10 meals at costco for the price of one meal at mcdonalds. The lazy tax has become too much for me, and I'm just not willing to pay it any more.

I liked that phrase: “the lazy tax.”

Meanwhile, the stock has done very well…

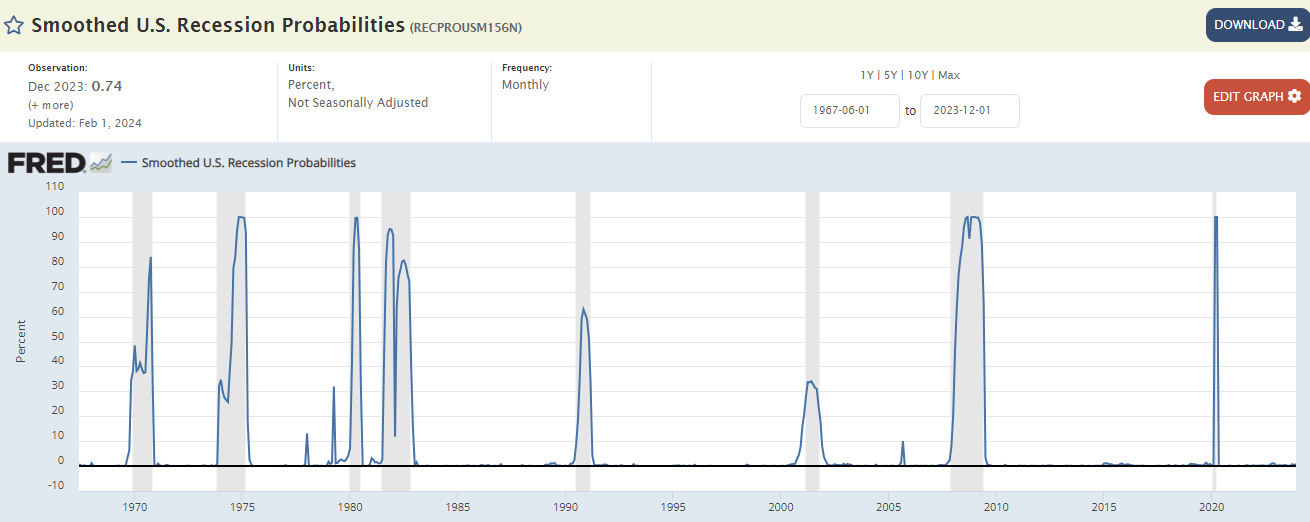

I always get a kick out of certain Fed data series like this one: “Smoothed U.S. Recession Probabilities,” which tend to get very, very low right before they get very, very high (currently at 0.74). I don’t see any predictive power, but then again I don’t have a math PhD. This series alone probably keeps a number of people employed.

Fun with models:

Smoothed recession probabilities for the United States are obtained from a dynamic-factor markov-switching model applied to four monthly coincident variables: non-farm payroll employment, the index of industrial production, real personal income excluding transfer payments, and real manufacturing and trade sales.

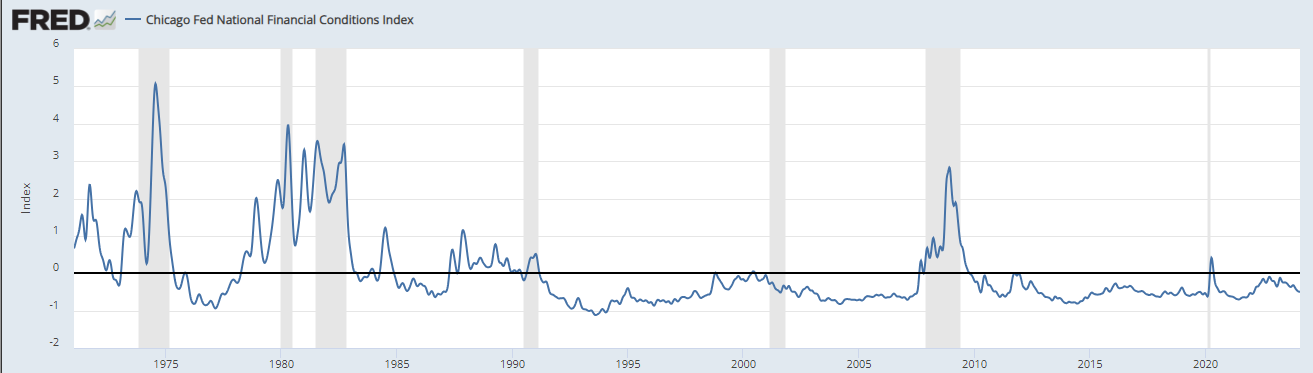

By this measure, financial conditions are looser than average. So…rate cuts, and end QT!

The Chicago Fed's National Financial Conditions Index (NFCI) provides a comprehensive weekly update on U.S. financial conditions in money markets, debt and equity markets and the traditional and "shadow" banking systems. Positive values of the NFCI indicate financial conditions that are tighter than average, while negative values indicate financial conditions that are looser than average.

“US Property Fears Send German Lender Bonds Plunging”

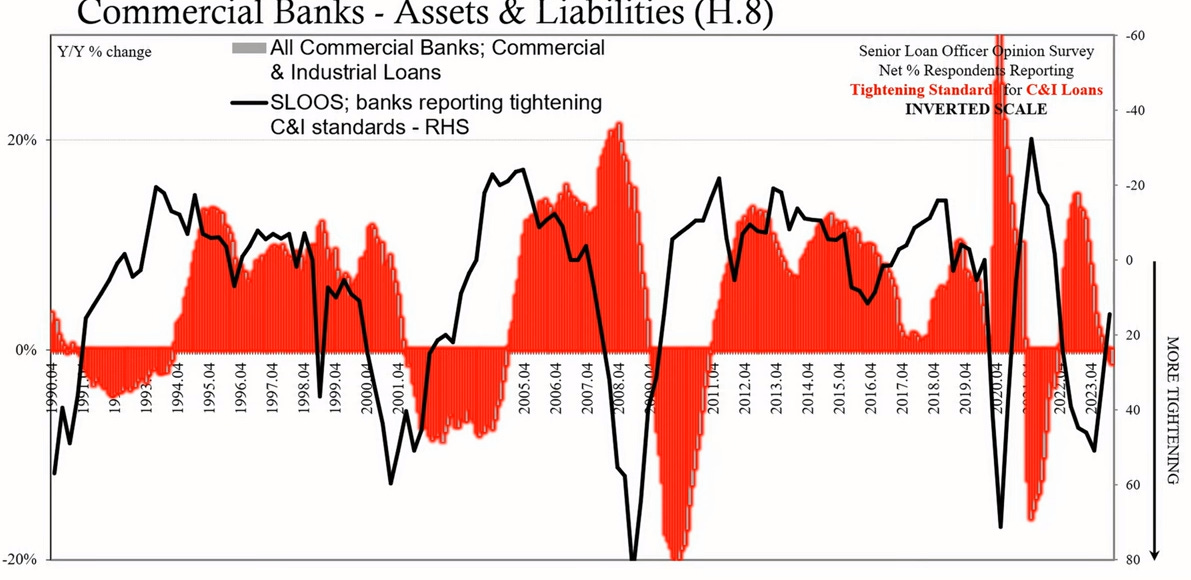

”It takes time for [tighter] lending standards to become lower levels of lending”

Snider: “We start with these two really strong cyclical charts that have been validated through various cycles over the last three-plus decades. Banks have tightened their lending standards, and within 18 months we should see the full effect of that in commercial and industrial loans, and as the commercial and industrial loans get become hard to come by, there is either a related or simply just a corresponding relationship with unemployment, which means this is still a business cycle, and the worst part of it remains just in front of us. Maybe by the end of this year we'll finally get to that point.”

Over 22,000 New Condo Units Are Going Unsold In The Greater Toronto Area — A “Record High”

“Affordability challenges reverberated through the Greater Toronto Area’s (GTA) new condo market in 2023, and new data shows that buyers simply weren’t biting as the year drew to a close…”

Unsold Inventory Reaches Record High

“With sales slowing much faster than new supply entering the market, total unsold new condominium inventory increased 41% year-over-year to 22,477 units in Q4-2023, representing a record high. Inventory was equal to 21.2 months of supply — roughly double the 10-12 months considered to be a balanced level. The 15.5 months of inventory in the 905 Region was substantially lower than the 26.7 months of supply in the City of Toronto….As of Q4-2023, a 31% share of pre-construction projects in the GTA sold less than 30% of their units, more than doubling the share in Q4-2022 (14%). Two years earlier in Q4-2021, there were no pre-construction projects that were less than 30% sold…Condo completions are expected to continue to ramp up in 2024. [New starts, however, have plunged - rh]

The overall average asking price for remaining unsold new condominiums in the GTA was $1,403 psf, decreasing 2% annually to reach a two-year low. Unsold prices were down 4% annually in the City of Toronto to an average of $1,524 psf, while increasing 1% annually in the 905 Region of the GTA to a record high $1,186 psf.”

Well over $1k per square foot - wow. Who can afford that? I mean, besides the Fintwit people?

Some reddit comments on the above:

The widely accepted market balance point is 6.5 Months Of Inventory, not 10 or 11 months. So, the problem is deeper than the developers want to let on. But the banks ain't fooled; they will stop lending on similar condos or require 50% down payments.

The bigger problem is those condos are priced at $500,000 to $1,500,000 US for 1 BR 1 BA and 2BR 2BA units. Who even knows what the monthly condo fee is!

I live in Singapore and sadly that's comparable to condo prices here... the cheaper option is public housing.

[Comment on the Singapore comment above] Dude how do you even compare. Private condos are a luxury, not a necessity. If you can't afford a private condo, HDB [Housing Development Board] flats are always available. If you cant afford a condo in Canada you're sleeping on the streets.

We have entered an era where construction costs far outweigh the ability for people to afford the final product. This will lead to a further increase in housing shortages. I’m in Philadelphia and my realtor friends tell me there is a growing inventory that isn’t renting or selling. Yes, mortgage rates are part of the equation but new rentals are just too expensive…Philadelphia has more available properties for sale than I’ve seen in the last 4 years and nothing seems to be moving, even as people are dropping prices. I look at 5 cities daily and what’s happening in Philadelphia seems to be the norm. Florida is even worse. There also seems to be an increase in portfolio selling of multiple homes.

I don't think labor has kept pace with the increase in the cost of housing. Sure, it has gone up and so has the cost of building material but I don't think those are the main drivers. We are replacing the roofs in my condo complex, before covid each roof (12 units in each building) cost about 55k, now it costs about 90k. The Spanish speakers that are doing the work are not commanding 65-70% more in hourly pay, you can bet on that.

Again, as usual, these are random comments from Reddit. Caveat emptor.

Across the 50 largest U.S. office markets, repair and maintenance costs increased 12.3% on average from 2021 to 2022.

Insurance prices are growing faster for multifamily than any other commercial real estate asset class, with national operators reporting a 26% rise in insurance costs on average from 2022 to 2023 and some being hit with 300% and 400% increases.

Report: 80 Percent of CMBS Office Loans At Risk of Default or Workout in 2024

“Moody’s Analytics study finds $5.6B of CMBS office maturities failed to pay off in 2023 and more are on the way in ’24…That 35 percent payoff rate is the lowest the CMBS office market has seen since 2009 – the nadir of the Global Financial Crisis – when only 37 percent of CMBS office loans were paid off. In 2022, even amid the rising interest rates, 78 percent of CMBS office loans were still paid off at maturity.”

Salt Lake City: A record amount of storage and distribution facility space became available in the last two years…50% of that square footage delivered in 2023 remains available. That is one of the lowest absorption numbers seen in the market in over a decade.

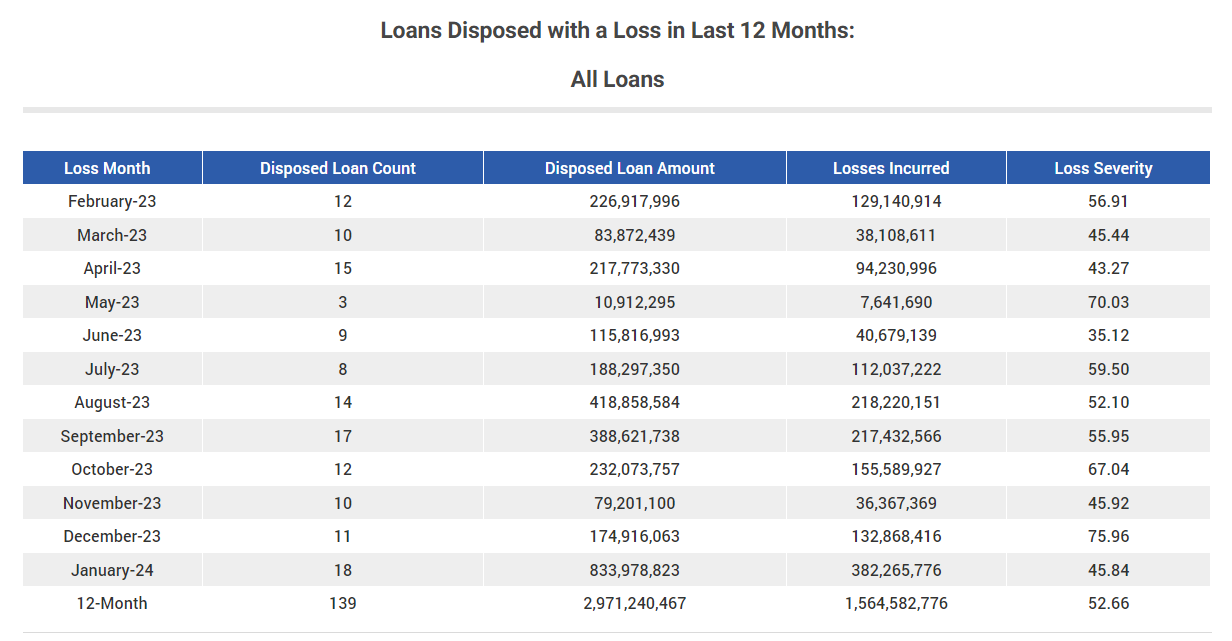

Trepp CMBS Loan Losses in the last year Those loss severities remain impressive.

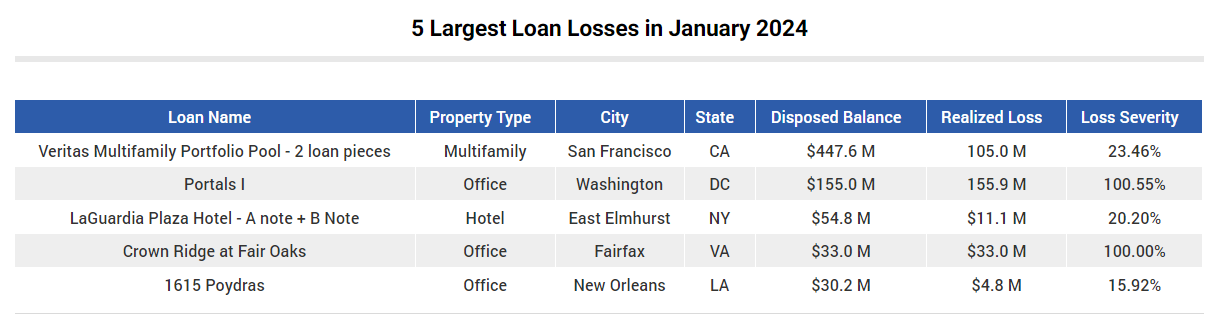

Five Largest Loan Losses in January 2024

Apartments make up 41% of the KKR REIT’s portfolio, its biggest share of loans by asset class. Matt Salem, the trust’s chief executive officer, said this week he expects distress in his firm’s portfolio will be limited, because its loans mostly went to higher-quality apartments.

“We are not really anticipating that much trouble within the multifamily portfolio,” he said on Wednesday’s earnings call. “But there’ll be a little bit of noise here and there.”

I note that insiders were buying shares almost a year ago near these levels. We’ll see if they add more now. [Update: They did.]

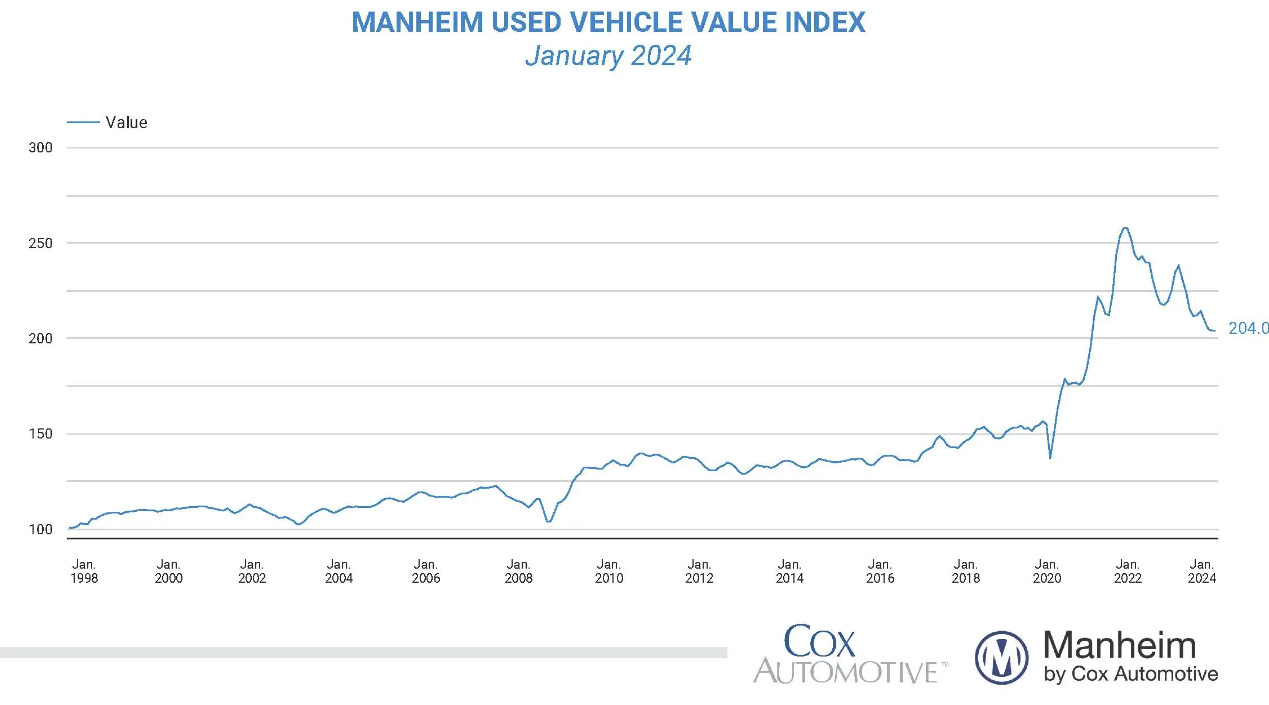

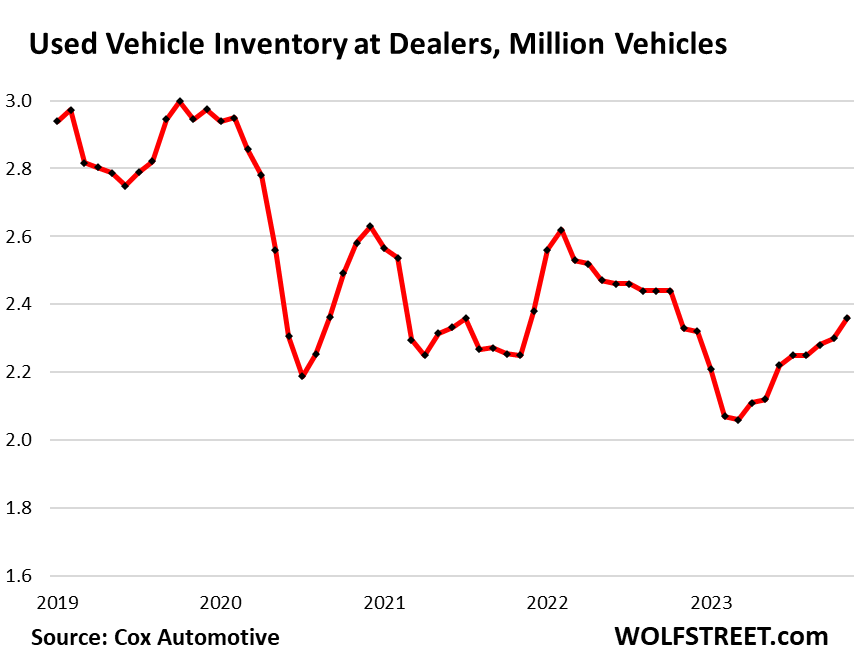

Wholesale Used Car Prices "Flat" in December; Down 9.2% Year-over-year

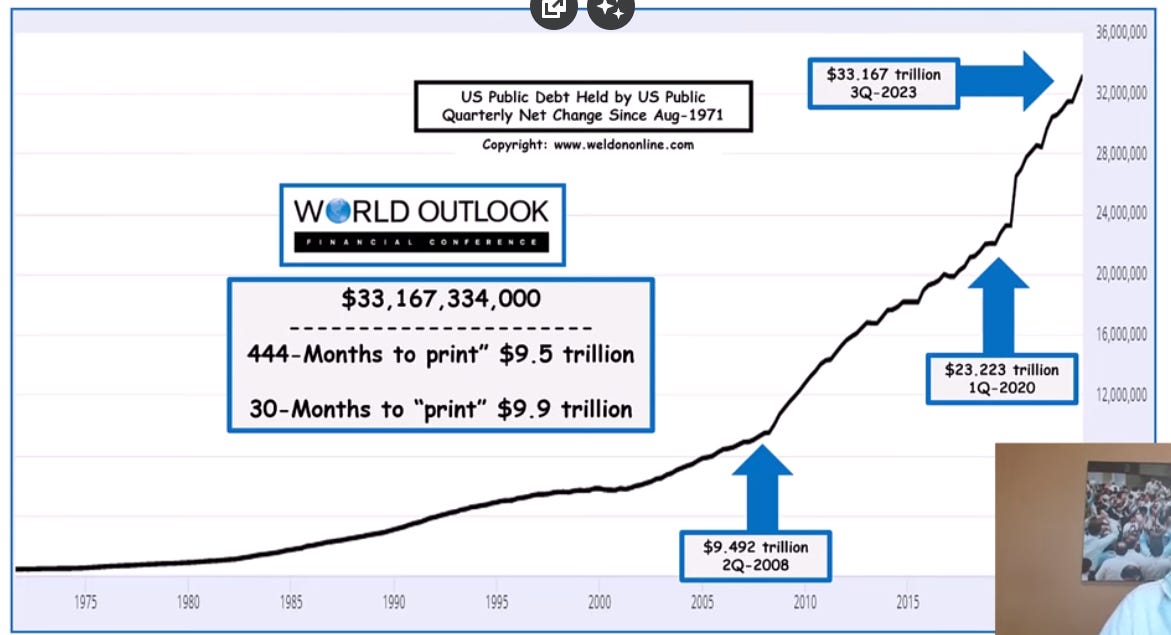

Greg Weldon pointing out some numbers…

Actually, the above chart is already outdated. As of Feb. 8, the number is $34,228,699,143,453.34.

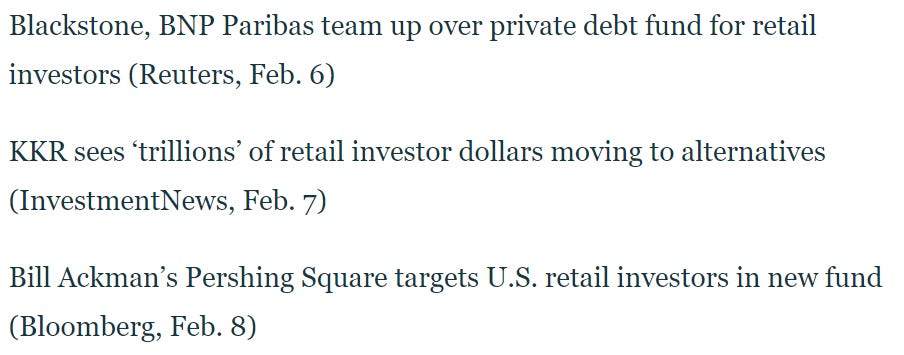

The private equity sharks are angling for retail fish…

Stewy: I have a shell company attached to his private equity fund. I'm a parasite on a parasite.

Kendall: You should have disclosed that to me when I brought you in.

Stewy: You are one hundred percent correct about that. I should have done that.

Succession, Season 1, Episode 81 (I just started watching)

Via Grant’s…

Behold a trio of headlines illustrating the unfolding “democratization of finance”:

Apollo CEO Marc Rowan, meanwhile, had this to say on yesterday’s earnings call regarding opportunities that high-net worth investors present to the alternatives industry:

We are in the earliest early days of this. [It] hasn’t even started. This is a $65 trillion market that ultimately has the potential for private markets investors such as ourselves and our peer group to be as large, if not larger, than our institutional market.

Asked about the roughly $12 trillion in global wealth stored in 401(k) retirement plans, Rowan replied thus:

I do see an opening in the 401(k) market. . . You’re seeing the first baby steps as fiduciary managers in 401(k) begin to mix in private [strategies] into their heretofore public solutions, simply to get better outcomes and better diversification.

It seems as if American citizens repeatedly rank last in terms of the priorities of our elected officials. People notice this after a while.

Gee, where did the weird populism come from?

Hyperinflation IS a default - a dishonest, regressive default.

“Here's the currency we owe you. It's worthless.”

“Yesterday saw Nikki Haley comprehensively lose a Republican Nevada primary where Trump was not on the ballot to ‘none of the above’, which says something about the gaps between what big political donors and actual voters want.”

- Michael Every of Rabobank

“In a typical private equity structure, the PE firm (Stewy) has a host of investors (Limited Partners). Each of these partners has a capital commitment and they get a proportionate share of ownership. For example, if you invested 10M in a 100M fund, you would own 10% of that fund’s ownership in any company they acquire. But with a 3B purchase, this likely violates Stewy’s PE fund’s investment guidelines, meaning that the Waystar stock is too large a percentage of the total portfolio value.

What Sandy has is a special purpose vehicle attached to Stewy’s fund. So when Kendall approached Stewy to take a piece of Waystar to fix the debt situation, Stewy approached Sandy to set up the SPV, which is a truly separate entity from the PE fund, and use it to acquire the Waystar stock from Kendall.”

“We are not really anticipating that much trouble within the multifamily portfolio,” he said on Wednesday’s earnings call. “But there’ll be a little bit of noise here and there"

This is going to be wild to watch

Excellent post

Love Yellen's..."wages are going up" The third job has been a savior for people.

Memories of the Jimmy Carter days: "You ever want to smoke a $100 cee-gar, stick with me"