“Feels a lot like the summer of 2020.”

Then again…

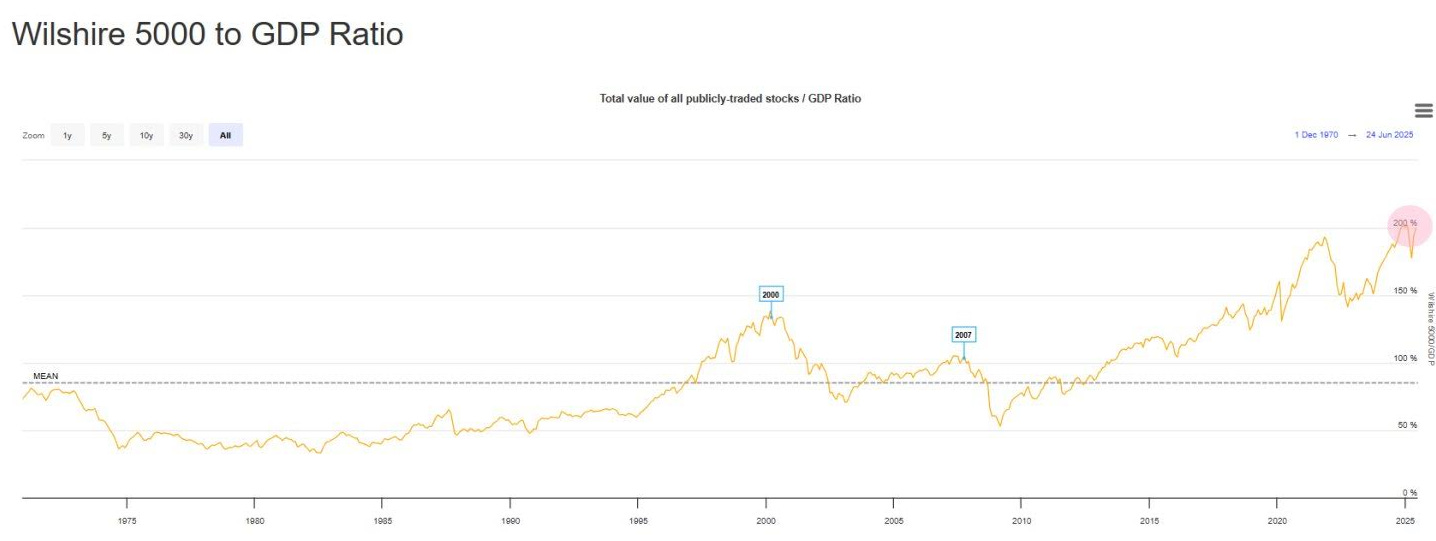

Fortunately, valuations continue to be irrelevant in a world of price-insensitive “passive” investing(?).

Central Banking 101

“As I look back [he confided to another American friend with an acrid nostalgia], it now seems that, with all the thought and work and good intentions which we provided, we achieved absolutely nothing…

I think we should have done just as much good if we had been able to collect the money and pour it down the drain…

By and large nothing that I did, and very little that old Ben [Strong] did, internationally produced any good effect—or indeed any effect at all except that we collected money from a lot of poor devils and gave it over to the four winds.”

Montagu Norman, Governor of the Bank of England from 1920 to 1944

The “Ben” above is Benjamin Strong, who served as Governor of the Federal Reserve Bank of New York for 14 years.

“The central banks and the governments have learned that there is one thing - and this is dangerous, obviously - but there's one thing to do. It's all they do anymore, right? Which is they just print money. That’s their savior, especially since '08. It's all they do. Anything gets weak, print money, Anything. It's all liquidity, liquidity, liquidity, liquidity. That's all they know how to do anymore, so that's going to be beneficial for gold over time.”

Gold, The Pet Rock

As an aside, having been on a number of podcasts and a few Spaces, the guest - in my experience - never has any say on the podcast title, which often has little or nothing to do with the guest's views, so keep that in mind. There are some great, sincere podcast hosts out there, and then there are a few who are just interested in using the guest for clicks. Fortunately I’ve only run into one of the latter (not included on my Substack).

And now, a Sarah Palin knife!

D vs R is Destroying Our Brains

So I'm told that "a stablecoin is a type of cryptocurrency that is designed to maintain a stable value, typically pegged to a specific reserve asset like a fiat currency such as the US dollar."

Well, that's not very stable, is it?

I guess this is an unstable coin. It’s worth a lot more now than $20.

Anyway, stablecoins hurt my brain, but Marvin Barth writes recently about them if you’re interested.1

“All price discovery is being done in server farms and dark pools by financial firms that haven’t had a losing day in many years.”

The usual eclectic mix below. Weekend beach reading.

“If you went long grift, you have made a bloody fortune, and the more freakish the grift, the more you made money. We're not really grift people, but we were very cognizant of the fact that that was going to be front and center in the Trump administration.”

"The powers of financial capitalism had another far-reaching aim, nothing less than to create a world system of financial control in private hands able to dominate the political system of each country and the economy of the world as a whole. This system was to be controlled in a feudalist fashion by the central banks of the world acting in concert, by secret agreements arrived at in frequent private meetings and conferences.

The apex of the system was to be the Bank for International Settlements in Basle, Switzerland, a private bank owned and controlled by the world's central banks which were themselves private corporations. Each central bank, in the hands of men like Montagu Norman of the Bank of England, Benjamin Strong of the New York Federal Reserve Bank, Charles Rist of the Bank of France, and Hjalmar Schacht of the Reichsbank, sought to dominate its government by its ability to control Treasury loans, to manipulate foreign exchanges, to influence the level of economic activity in the country, and to influence cooperative politicians by subsequent economic rewards in the business world.”

Carroll Quigley, Tragedy and Hope: A History of the World in Our Time

Paul Tudor Jones on A.I.

“…the unemployment rate for recent college graduates stood at 5.8%, topping the national level for the first and only time in its 45-year historical record. It’s an alarming number that needs to be considered in the context of a recent warning from Dario Amodei, CEO of AI juggernaut Anthropic, who predicted artificial intelligence could wipe out half of all entry-level, white-collar-jobs and spike unemployment to 10-20% in the next one to five years…

As someone who has spent nearly half a century as a professional risk manager, every alarm bell in my being is ringing, and they should be in yours, too…

I recently attended a small conference with some of the titans of tech. There, four of the top AI developers agreed with the hypothesis that “AI has a 10% chance of killing half of humanity in the next 20 years.” One modeler even stated that in a world with no guardrails, AI will make it infinitely easier to weaponize a viral epidemic.

So what should we do? First, we need to stop delaying efforts to make AI safe for humanity. And that means removing the ill-considered AI enforcement moratorium from the Big Beautiful Bill.

Second, we need to pass a federal law that says all AI must be watermarked so we know when the content we are consuming is AI generated. We also need to criminalize AI fraud and intent to harm. Humans will become irrelevant in the world we are headed for if we don’t demand human authenticity.

Third, we need to create a new U.S. bipartisan commission to address the crucial issues of productivity sharing, so we are proactive as AI bears down on us.

And finally, we need to initiate bilateral talks with China to start establishing shared AI safety protocols to protect the entire world from mistakes and bad actors.

None of this is radical. It’s rational. The unemployment data on entry-level jobs is a call to action. The first signs of the societal disruptions of AI are already here.”

Howard Marks on Tariffs:

“Tariffs are, primarily, an effort to cause goods to be made domestically even when equivalent foreign goods are cheaper or better (or both). Governments can make that happen by erecting barriers that keep foreign goods out or make them more expensive. That protects domestic industries and domestic workers, but at the expense of domestic consumers (and global welfare). That’s a tradeoff – the kind of thing free markets require and leaders who would mandate economic outcomes would prefer to ignore.”

Via Jim Grant’s Outfit

Mr. Market turns up the temperature: The speculative-grade credit market is operating at a blistering pace, as more than $10 billion of new U.S. leveraged loans launched yesterday by Bloomberg’s count, the busiest single session since March 3. That slate of a dozen transactions included nine refinancing or repricing deals, with another pair of borrowers earmarking proceeds to fund dividend payouts for their p.e. promoters.

Similarly, eight high-yield bond sales launched Monday, marking the most active day since January. Among that cohort: an offering to help fund 3G Capital’s leveraged buyout of footwear concern Sketchers U.S.A., which includes $2.5 billion in unsecured pay-in-kind toggle notes permitting the borrower to defer cash interest by adding to the principal balance. [this sounds like an FHA program - rh]

Overall month-to-date junk bond supply of $26 billion stands nearly 50% above that seen throughout June 2024.

The Fed is too restrictive!

Lacy Hunt

“If we're not in a recession now, we will be. It's kind of hard to have confidence when such a critical variable as payroll employment is so grotesquely overstated relative to the business employment dynamics, which is your full sample of 12 million firms.”

“Whenever you have a prolonged period of stability in markets, and a lot of debt creation, and perhaps risky debt creation, there is an increasing risk of what people would call a Minsky moment2. Now a Minsky moment is very difficult to project, but there are two studies that I would recommend people read that have just recently come out. One is from the Boston Fed on the systemic risk to the banking system from their lending to the private credit sector, and a similar study from the IMF on this in systemic risk that may may link the banks to the private credit. Now keep in mind the the entire increase in bank lending over the last year has been to one sector, net, and that is to the non-depository financial institutions, which is your private credit.

Now these folks right now have good credit ratings, but they are lending to very risky borrowers, and they're leveraging3 those loans. The Boston Fed is saying there's a systemic risk. The IMF is saying there is a systemic risk. There are a lot of instances in the past where we've seen similar types of behavior, and as Minsky said, stability leads to instability. Now you you can't predict that, but this pattern um of systemic risk is something that has me concerned, something that cannot be predicted, but it it certainly in my view is in the system.”

“What happens some empires, when they are debt overheavy, too much in interest expense, they do resort to money printing at the end, and the money printing then just makes things worse. People always say, "Well, we can always inflate our way out." No, we cannot. We tried heavy money printing during the pandemic, and what happened? The inflation rate surged, and the tragedy of that inflationary surge during the pandemic, and in 2021 and 2022 and early 2023, is that the burden fell most heavily on our modest and moderate income households. The majority of our people are heavily robbed by inflation. Virtually no one except the the most wealthy of us have the resources to protect themselves. So when when you get into these highly over-indebted situations, empires have tried to go the money printing route, and that occurs shortly before the violent end.”

Hunt on David Hume:

Hume’s “recommendation for successful government was to always run budget surpluses, so that when you have a national emergency, you don't have to go into debt to pay for it, we’ve done exactly the opposite.”

“The U.S. has become a major global empire, when many of the people in the United States don't want to play that role.”

Albert Einstein and David Hume

“From the very beginning it appeared to me intuitively clear that, judged from the standpoint of such an observer, everything would have to happen according to the same laws as for an observer who, relative to the earth, was at rest. For how, otherwise, should the first observer know, i.e., be able to determine, that he is in a state of fast uniform motion?

One sees that in this paradox the germ of the special relativity theory is already contained. Today everyone knows, of course, that all attempts to clarify this paradox satisfactorily were condemned to failure as long as the axiom of the absolute character of time, viz., of simultaneity, unrecognizedly was anchored in the unconscious. Clearly to recognize this axiom and its arbitrary character really implies already the solution of the problem. The type of critical reasoning which was required for the discovery of this central point was decisively furthered, in my case, especially by the reading of David Hume’s and Ernst Mach’s philosophical writings."

CRE

“We've transitioned our portfolio, 20% of it already, to fixed-financing that's 20 years or greater. It's hard. It's more expensive, but it's a defensive position.” - Paul Daneshrad

Commercial real estate distress hit $116B in March, up 23% YoY, the highest since the financial crisis, per MSCI. Green Street reports delinquencies are still rising, though more slowly. The FDIC noted past-due and nonaccrual loans are now at their highest level since 2014, with multifamily loans becoming a bigger concern.

JPMorgan Re-Packages Bonds Tied to Apartment Loans Into New Debt in Rare Move

“JPMorgan Chase & Co. has bundled the riskiest portions of over a dozen Freddie Mac mortgage bonds tied to small balance apartment loans in what appears to be the first time this sort of debt has been securitized not once but twice.”

“Known as a resecuritization, the deal pools together 18 bonds created by Freddie Mac, each of which is backed by apartment loans of up to $7.5 million…The roughly $500 million of mortgage bonds included in the deal are tied to Freddie Mac’s Small Balance program, which offers loans of between $1 million and $7.5 million for apartment buildings with five or more residential units..”

“In the new deal, the credit investor Axonic Capital contributed all 18 of the underlying mortgage bonds, the offering documents show. It’s the first time that this type of Freddie Mac debt has been re-packaged into new bonds and received credit ratings, according to Matt Weinstein, co-chief investment officer at Axonic.

“Our [alleged] motivation was to take advantage of the strong demand for mortgage credit, in particular multifamily debt,” Weinstein said in an interview, referring to real estate deals focused on apartment buildings.

A spokesperson for JPMorgan declined to comment. [probably wise]

While Freddie Mac provides a financial guarantee on the bonds tied to the small balance program, the backing doesn’t apply to the riskiest bonds, known as the B-Pieces, which are the first in line to take losses if the underlying loans fail. It’s these risky bonds that Axonic contributed to the resecuritization, the offering documents show. Axonic focuses heavily on commercial real estate debt and owns roughly half of all the B-Pieces tied to Freddie Mac’s small balance loans, according to Weinstein.”

I don’t know - maybe I’m too skeptical - but multifamily in general is having a tough time right now…

"If it's such a great trade, why are you offering it to me?"

Not CRE

Austin: -22.1%

Oakland: -20.3%

New Orleans: -18.1%

San Francisco: -15.3%

Washington DC: -10.8%

Denver: -9.0%

Portland: -8.9%

Phoenix: -8.8%

Fort Worth: -7.7%

San Antonio: -7.6%

Some perspective:

For the linear folks:

“Case-Shiller home prices fell 0.3 percent in April after declining 0.1 percent in March. The lead chart puts things in perspective:”

“Owners’ Equivalent Rent (OER) is the price one would pay if they rented their own house, unfurnished, without utilities, instead of owning it.

No one pays OER. And on that basis many claim the CPI is overstated. From the point of view of those wanting to buy a home, the CPI is very understated…This is a mess entirely of the Fed’s making. And it’s what happens when the Fed, and economists in general do not count home prices as inflation.

Home prices are not directly in the CPI or PCE. The latter is the Fed’s preferred measure of inflation.”

Check back to last year, when David Dredge explained that what the Fed wanted “was to sort of break the dichotomy between their dual mandate - that you could drive growth through the wealth effect of asset inflation, and then not measure assets in your measure of price stability, and you could then do both, and if you think about really what's happened during the sort of low-volatility of inflation era, that's exactly what was going on the monetary policy.

“Investors accounted for 10.8% of home sellers last year, the highest share ever measured by Realtor.com.”

“Investors continued to buy more homes than they sold, a trend that has existed through more than two decades of data, the Realtor.com report said. Investors made up 13% of homebuyers in 2024, up from the prior year but slightly off their 2022 peak.”

“The report also found that investors bought less expensive homes in 2024 in order to boost potential rental revenue. The typical investor paid $282,000 for a home purchase in 2024, more than $70,000 below the national median sale price.

“This trend highlights how investors tend to concentrate in lower-priced metros and in the lower-priced segments of the market, where homes are more likely to generate positive rental returns,” the report said. “ As a result, budget-conscious buyers often find themselves in direct competition with investors for the most affordable properties, a contest many are unable to win.”"

Best & Worst-Run Cities in America (2025)

Via Charlie

“The spread between the highest & lowest yield among 5 major US asset classes is now less than 1%, the lowest on record:

BofA US Corporate Bond Index: 5.19%

30-Year Treasury Bond: 4.90%

S&P 500 (earnings yield): 4.72%

10-Year Treasury Bond: 4.38%

-3 Month Treasury Bill: 4.32%”

Generation Twee

“For this study, we surveyed 1,000 American employees, capturing insights across participants' age, gender, and location. Participants were asked to identify which workplace perks they considered to be absolute must-haves when evaluating job opportunities.”

Paid overtime was revealed as the most in-demand employee perk in America, with 76% of professionals saying it is a must-have.

A third of Gen-Z workers argue that a compressed workweek should be a non-negotiable perk, more than any other generation.

Female professionals prioritize inclusive and supportive benefits, such as maternity/paternity leave and DEI training, more than their male colleagues, who prefer financial benefits such as stock and investment options.

Nap Rooms

Fun rooms, such as spaces with games like ping-pong and other recreational activities, are popular amongst Gen-Z, with 18% saying that they’re a must-have in the workplace. This compares to 14% of Millennials, 6% of Gen-X and only 1% of Baby Boomers. This highlights that younger employees view fun and relaxation as an essential part of workplace culture. Similarly, the study found nap rooms to be popular amongst Millennial workers, with 17% considering them an essential, and 13% of Gen-Z agreed.

“Pet-friendly offices have also risen in popularity, especially among Gen-Z (20%) and Millennials (14%), who increasingly view the ability to bring pets to work as a quality-of-life benefit that fosters a more relaxed and supportive office atmosphere.”

What is this - the New York Fed??

Map of Middle Eastern countries that the US has bombed since 2016

“We also glory in our sufferings, because we know that suffering produces perseverance; perseverance, character; and character, hope.”

Paul

Something has to happen to change the direction…

Spooks: The Haunting of America - The Private Use of Secret Agents

I came across this 1978 book by Jim Hougan after listening to a podcast on a different book, on the secret history of the “Anglo-American” establishment. In that book were footnotes, one of which pointed me to this book - which I intended to use to research Donald Trump’s involvement with Resorts International in the late 1980’s. However, while skimming the book, I got distracted by the passage below.

This is generally how I come across things.

Here is a small excerpt, from one chapter, but still, quite a few bombshells:

The most interesting link between Richard Nixon and Robert Vesco is one alleged by former Howard Hughes aide Johnny Meier. A business associate of Donald Nixon Sr.’s, Meier told me that on a business trip to the Dominican Republic the President’s brother confessed that Vesco was in charge of secret bank accounts belonging to himself and Richard Nixon. Admittedly, Johnny Meier is not an impartial observer. A friend of Marlon Brando’s, he shares the actor’s liberal views, supported Senator George McGovern for President, and was active in raising funds to defend former CIA officer Daniel Ellsberg in the wake of the Pentagon Papers’ release. But Meier was also an employee of Howard Hughes’s, responsible for a number of sensitive matters. Besides lobbying to eliminate nuclear testing in Nevada, he served the billionaire in a realtor’s capacity, helping to arrange the purchase of abandoned mining properties.

In the performance of this latter assignment, Meier came under investigation by a number of private and federal agencies, including Intertel and the IRS. Before long, indictments were brought against him in California, charging that he’d bilked Hughes of millions in the course of buying up worthless properties. Currently in exile in Vancouver, Meier claims that he’s the victim of a political frame-up and points to a campaign of dirty tricks supposedly carried out against him.

According to an affidavit written by one “Virgino Gonzalez,” who purports to be a retired CIA officer, Meier was the victim of a political conspiracy involving a host of crimes by the CIA and other agencies in the United States and Canada. The affidavit alleges that Meier was the target of constant (and illegal) surveillance; that his house and hotel rooms were burglarized by authorities; that judges were suborned by the CIA; that the Agency intervened at the Wall Street Journal, “funding” some reporters and bringing about the transfer of others who were friendly with Meier; that the CIA manipulated the courts and the national press to destroy Meier’s New Mexico campaign for the Senate; and that the Agency was deemed to be too witting for his own good. In short, the Gonzalez affidavit is a bombshell. Almost parenthetically, the author makes devastating accusations, to wit: “During 1968/ 1969 I had been told to drop all investigations into Sinclair Weeks and his movement of monies abroad for political funding and first came into contact with John Meier in April 1969 in Las Vegas. At about 15.00 on April 25 Sen. Edward Kennedy arrived at Las Vegas and was to give a speech that night. With other agents I arranged with Jack Entratter of the Sands Hotel to fix a girl for Kennedy and for pictures to be taken for future use. Kennedy fell for the situation but the full use of the operation was ruined when Meier had heard something of it. I learned later that he had contacted Bill Haddad, Larry O’Brien, Joseph Napolitan and Steve Smith and warned them of a problem.” (Italics mine.)

Elsewhere: “. . . Meier [had] met with several CIA agents in Nevada. It had been thought by them that Meier was informed regarding agency cooperation with the Hughes organization and [Robert] Maheu’s company. It seemed that Meier had stepped into the Ecuadorian situation as well as obtaining a list of politicians whom we wanted funded thru Hughes.” “October 16 Meier again called Paul Schrade in California. And when he talked to Stan Sheinbaum at McGovern’s HQ (213) 469 9061 on October 31 the call was traced and we knew Meier’s new home.” (Italics mine.) In other places, the affidavit describes CIA meddling in Canadian political affairs and, almost incidentally, refers to CIA surveillance of Playboy publisher Hugh Hefner.

It’s a stunning document, ten pages long, and virtually every other sentence contains a bombshell. Did the CIA tap McGovern’s headquarters, as the affidavit implies? Did the Agency plan to have Senator Edward Kennedy seduced for reasons of blackmail? Did the Agency provide Howard Hughes with a list of politicians that it wanted to support—and, if so, did the money come from Hughes or, indirectly, from the Agency itself? If the Gonzalez affidavit is to be believed, the United States is a police state run by a dangerous consortium of CIA officers, private intelligence agencies, and White House entrepreneurs.4 And the affidavit is not entirely unconvincing. It names names, gives dates and places, and provides a flock of unlisted telephone numbers belonging to movie stars and politicians alike. It also reports the nature of conversations that were thought to have been private—and does so throughout in the first person.

In short, the affidavit is for the most part verifiable. And one would have little choice but to believe it if one could only find its author, “Virgino Gonzalez.” He, however, has disappeared after delivering his affidavit to the court. Whether Gonzalez was, as he claimed to be, a fifteen-year veteran of the CIA, or someone else is uncertain. The Agency will not comment on whether it has ever had such an employee, and sources within the spooks’ milieu claim never to have heard of him. “Virgino,” however, is a most unusual name, even for someone who claims to have been born in Cuba. And, interestingly, the alias “Virgino Gonzalez” has been used by a sometime CIA agent—a Cuban exile whose real name is Max Gorman. Years ago, Gorman was arrested in Miami in connection with the theft of an automobile and gave his name as Virgino Gonzalez. Today, however, Gorman denies having written the document that bears his peculiar alias.

Reporters familiar with the case are themselves divided over the affidavit’s authenticity. Some think that Meier may have written it himself in an effort to further his own legal cause. As a participant in many of the events described in the affidavit, Meier could easily have forged a report of his own surveillance, attributing it to a disgruntled CIA agent. On the other hand, Max Gorman is just such a fellow: a clandestine operator and a friend of Watergate burglar Frank Sturgis, Gorman is sufficiently angry at the CIA as to have filed suit against it, charging that the Agency betrayed himself and his friends on secret missions into Cuba.

If there was nothing more than Johnny Meier’s report of Donald Nixon, Sr.’s, ‘admission”’ that Vesco controls offshore bank accounts belonging to Richard Nixon, one would have to ignore the charge. And yet there is other evidence of the truth of the allegation. Norman Casper, the Tums-popping private eye known to friends and foes alike as “the Friendly Ghost,” discovered that evidence while investigating the Castle Bank & Trust5 of the Bahamas and Cayman Islands. A nervous, thickset spook with a gentle way about him, Casper earned a curious living as a sort of bounty hunter for the IRS. His quarries were illicit bank accounts and bogus loan transactions carried out in the Caribbean by vest-pocket banks in behalf of American tax evaders. Providing the IRS with proof of such accounts, Casper (or “TW-24,” as his IRS contacts knew him) would receive an informant’s fee. It wasn’t much in proportion to the amount of money involved—Casper might get five thousand dollars on every million—but it paid the mortgage on his house in Key Biscayne and kept him in Bloody Marys at the Jamaica Inn. Besides, there was always the possibility that he would actually “break a bank,” revealing all its illegal transactions, and earn a million of his own. Formerly a detective with The Wackenhut Corporation, the Friendly Ghost had good contacts in the Miami and Caribbean areas. Through a banker friend he met Samuel Pierson, then president of the Castle Bank, at the Miami airport in October, 1972. Hinting that he was a DEA agent searching for evidence of narcotics transactions, Casper obtained Pierson’s business card with a message scribbled on its back: “HMW: give this man anything he wants.” HMW was H. Michael Wolstencroft, resident manager of the Castle Bank.

Why Pierson cooperated with Casper is something of a mystery, but it probably has to do with the strange nature of relationships between banks like Castle and their customers. Like many other banks in the Cayman Islands, Castle had no guards, no tellers, and no vaults. Like Vesco’s Standard Commerz Bank in Switzerland, it had no need for cameras or alarms, and hardly ever were its storefront doors invaded by the physical presence of a customer. Castle Bank had neither checking accounts nor savings accounts. Virtually all of its assets were kept on deposit with other banks in the United States, its headquarters in the Caymans serving only as a repository for the bank’s records. No one knows exactly how many such banks there are in the Bahamas and the Caymans, though it’s been pointed out that the Cayman Islands alone have more than 14,000 telex numbers (the instrument of most banking transactions) and fewer than 13,500 residents. According to the IRS, more than fifteen billion dollars per year flows through these banks—and a good deal of it is funny money.

An old alchemist gave the following consolation to one of his disciples : "No matter how isolated you are and how lonely you feel, if you do your work truly and conscientiously, unknown friends will come and seek you."

Carl Jung, Letter to Miguel Serrano, September 14, 1960

“From 1950 to 1966, the military performed open-air testing of potential terrorist weapons at least 239 times in at least eight American cities, including New York City, Key West, and Panama City, FL..."

“Pending US legislation officially sanctioning stablecoins would usher in a profound shift in the US financial system towards a “narrow banking” model. Narrow banking, or the “Chicago Plan” as it is sometimes called, was an idea hatched by a group of prominent University of Chicago economists in the early 1930s to replace fractional reserve banking with a combination of “narrow” fully reserved depository institutions whose primary function is payments, and merchant banks that fund lending from equity and long-term debt rather than deposits. Full reserving of the former would insulate against runs and separate both the payments system and money creation from the credit creation (and crises) of the latter.1

Stablecoins are, for all intents and purposes, narrow banks. Their primary function is as a depository payments system, a feature I address in greater depth below. In theory – though not always in past practice2 – stablecoins are fully reserved, that is backed one for one with safe assets to ensure their value. The US legislation requires full backing by specifically defined high-quality liquid assets (HQLA), regular auditing – the STABLE Act even requires daily asset transparency – and repayment of depositors at par. This is effectively a narrow bank, but the legislation leaves out two critical features of a true narrow bank: (1) access to lender of last resort support from the Federal Reserve; and (2) legal status as money, which leaves stablecoins inferior to money under both tax and bankruptcy law.3 I should also note that I’m not the only person thinking this: hats off to Charles Calomiris at Columbia University for seeing stablecoins as a narrow-banking future as early as 2020 (and to Kathleen Hays for bringing it to my attention before I published on this topic).4

Yet, there are intriguing signs in the legislation that they are a first step towards true narrow banking: among the allowable HQLA – in addition to T-bills, repo, currency, FDIC-insured bank deposits, and government money market funds – are reserves at the Fed, i.e. that same Fed the legislation doesn’t (yet) give them access to. This likely reflects banks lobbying and a measure of prudence so as not to undermine the fractional reserve banking system too quickly.”

“The term [Minsky Moment] refers to the end stage of a prolonged period of economic prosperity that has encouraged investors to take on excessive risk, to the point where lending exceeds what borrowers can pay off. At that point, Minsky wrote, there’s an increase in “speculative and Ponzi finance.” When a destabilizing event as simple as an increase in interest rates occurs, investors can be forced to sell assets to raise money to repay loans. That in turn sends markets into a spiral amid a demand for cash. There have been attempts to distinguish between a Minsky moment and a Minsky process that leads up to it.“

By the way, my Substack is titled, “A Havenstein Moment” in honor of Minsky.

“I'm happy having ninety percent of my net worth in Berkshire stock. We're going to try to compound it at a reasonable rate without taking unreasonable risk or using leverage. If we can't do this, then that's just too damn bad.” - Charlie Munger

This passage strongly echoes Bruce Hemmings’ comments I mention in my October 2022 post, “The ends justify the means”

I also mentioned Castle Bank in “The ends justify the means”

I can't believe that you don't have the Numbah One stack in all of stackdom. I am amazed by what you throw at the wall, every piece of spaghetti (Ramen?) sticks. None of it slides down. This takes the cake, or to keep my metaphors straight, lasagna, kinda like cake...https://x.com/sadvalueinvestr/status/1937907507747336583/photo/1

I did not have Robert Vesco on my HM Bingo card. That's a name from eons ago! Rudy, you might be as old as I am!

Thanks for the linear chart! U R D Best!