This is not 1931

There is no fear.

Sir Thomas More hands Richard Rich a silver cup…

MORE: It was sent to me a little while ago by some woman. Now she's put a lawsuit into the Court of Requests. It's a bribe, Richard.

RICH: Oh…So you give it away, of course.

MORE: Yes!

RICH: To me?

MORE: Well, I'm not going to keep it, and you need it. Of course, if you feel it's contaminated…

RICH: No, no. I'll risk it.

(They both smile)

MORE: But, Richard, in office they offer you all sorts of things. I was once offered a whole village, with a mill, and a manor house, and heaven knows what else - a coat of arms, I shouldn't be surprised. Why not be a teacher? You'd be a fine teacher. Perhaps even a great one.

RICH: And if I was, who would know it?

MORE: You, your pupils, your friends, God. Not a bad public, that…Oh, and a quiet life.

A great point from a reader about the Luke Gromen podcast that got me going yesterday:

I grew up in Israel during the inflation years, what Luke misses is that every worthy asset was priced in $, businesses, houses, land, rent, oil, no one priced their assets in local currency, having the $, allowed the local currency to float and allowed transactions of rare and expensive assets, otherwise, it would've been a total mess.

“The Keynesians and the people who are running government money and have been for the last 50 years are absolutely wrong when their knee-jerk reaction is to drive consumption rather than investment in capital formation. Capital formation is what creates the consumption of the future, no the other way around.”

Steven Wilkinson

(Here’s more on the 18-year property cycle Wilkinson mentions.)

What Does Biden’s Pick for Next World Bank President Augur for the Global War on Cash?

Ajay Banga, in his former senior executive roles at Mastercard, waged a decade-long “war on cash.” Under his tenure, the company did more than just about any other to demonise the role of physical money around the world.

A “Davos Type of Globalist”

the myth of financial inclusion often peddled by Western banks, fintech companies and payment processers…the real motives of the companies seeking to expand digital financial services to the world’s unbanked have much more to do with advancing their own financial interests and promoting a particular ideological worldview, than addressing structural economic injustice

Incentives. Always incentives.

Great March 2020 article I used to have a very long Twitter thread on, before Elon nuked it: The Great Wall Street Housing Grab

Before 2010, institutional landlords didn’t exist in the single-family-rental market; now there are 25 to 30 of them, according to Amherst Capital, a real estate investment firm.

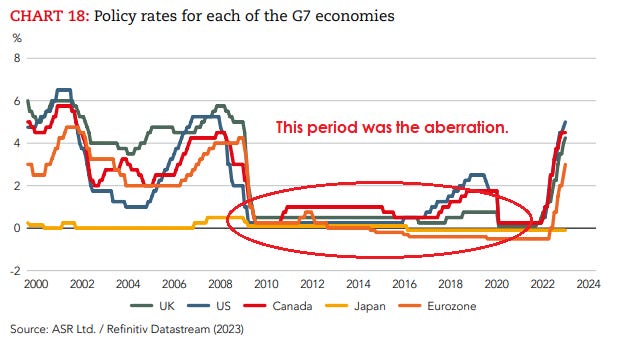

The last time I heard so many “Great Depression” comparisons was in December 2018, when every day some CNBC spokesmodel would come on and say, “this market is the worst since 1931.” Now it’s the money supply.

Look, the S&P 500 is 14% off all-time historic mania highs, and it’s 500% higher than March 2009. This is not 1931.

Speaking of the 1930’s, this is from "The Great Crash 1929" by Galbraith, from a 1932 Senate hearing. Plus ça change.

“If the first visible effect of a panic or depression is the deflation of debt;

then, debt must have caused the panic or depression.”

Freeman Tilden, A World in Debt (1935)

Quoth the Raven #310 - Trader Sang Lucci: “There’s just a lack of fear right now. There’s a lack of fear.”

This is my take as well.

(Lucci nonetheless is very bullish - “melt up” - until fear returns, on stocks and Bitcoin. I expect both to fluctuate.)

I’m not “trader.” I buy infrequently and I sell even less frequently. I guess because of my rants against the Fed some people assumed I was a short. I’m very long and always have been (although my portfolio, and the % of cash I usually hold, would appall 95% of finance types.) The Fed’s insanity has benefited me personally - I’m just not a psychopath.

I haven’t shorted anything since 2009. On rare occasion when I want to hedge against capital gains I’ll buy puts, which generally don’t work out. I don’t like bonds either (except some I-Bonds.)

I once had a guy from Price Waterhouse look at my portfolio and say, quote, “This is insane,” and he didn’t mean in a good way. This was during the DotCom bubble. He told me I should be 100% in ‘High Tech Growth Stocks.” Had I listened to him, I’d likely have lost 80% over the next couple years (and I know people who did.)

Anyway, I used to watch FNN in the 1980’s. CNBC absorbed them in 1991. I’ve had CNBC on in the background since the 1990’s. In the 1990’s tech bubble it was awful, and I’ve saved a lot of clippings from those years. CNBC for me was a barometer of that mania, and yes, Jim Cramer’s advice was just as wrong back then as it is now. So many people destroyed by his advice over the years - and the numbers back then - huge at the time - seem so tiny now.

I knew people who hadn’t heard of stocks three months before suddenly doubling their money on things like JDSU (or, as Cramer would say, “Just Don’t Sell Us.”) They gave it all back eventually. Bill Fleckenstein kept me sane during this time.

During the housing bubble run-up, CNBC would pump just as hard as during the Dotcom bubble. They’d sometimes bring on a housing bear and literally laugh at him or her (Fox Business was notorious for this too.) With the 2008-2009 crash, I was kinda hoping CNBC would become a cooking channel, but no.

Why watch it then? Well, I don’t really “watch” it - it’s just on, now in the background of my ThinkorSwim app, often on mute - but it’s a great barometer of market sentiment and general goofiness over the years.

For a recap of the last housing bubble (before this one), check out the Jon Stewart/Jim Cramer interview:

Besides the humor material, I have gotten some historical screen grabs over the years at crucial market moments, like this one, March 18, 2020:

Anyway, as bad as CNBC has been over the years, it took a turn for the worse in early 2020. CNBC was always an advocate of censorship and authoritarianism, but Covid made them - like so many - insane. CNBC then bent over backwards trying show how fake "woke” they were. It’s now almost unwatchable, mostly a virtue-signaling Wall Street infomercial and promotional platform for scammers. All the worst people rose to the top. I wrote this in June 2020:

CNBC has done nothing this century but cheer-lead the greatest expansion of wealth inequality in history, while putting on an endless parade of criminal CEO's, phony corporatist virtue-signallers, and very close friends of Jeff Epstein & Harvey Weinstein. I hope they're well paid.

But, to get back to the original point, there’s no fear right now. Every other question on CNBC is, “So what are you buying here?”1

Gonna mention Nvidia, since it’s the flavor of year it seems. No position, just a memory.

Nvidia 1999-2002

Nvidia 1999-2016

People get excited.

That 90% drop in 2002 was epic. Note that the 2002 high of $5.56 wasn’t topped until 2007, after which the shares fell 85% (all these are split-adjusted). The 2007 then wasn’t surpassed until 2016. Today the shares are in the 270’s, and everyone who bought in 2002 and has been in a coma for 20 years has a hundred-bagger.

The share prices of other darlings of the Dotcom era like Intel and Cisco are still lower than in 2000, but at least they survived. Countless companies over the years just vanished. Lots of survivor bias in stock markets. People forget, but Intel and Cisco then were like Apple and Tesla today.

Cisco Systems, which supplies much of the infrastructure for the Internet, jumped 333/64 , to 1441/16 , lifting its market capitalization above $500 billion and making it the first company based in California's Silicon Valley to break that ceiling.

This is interesting, from the same article. History repeats:

''It is a fever that has gripped the country,'' said Harry Cohen, manager of the Smith Barney Appreciation Fund, referring to demand for computer and other high-technology stocks that has generated huge wealth and added urgency to the Federal Reserve's efforts to cool off the supercharged American economy so inflation remains in check.

Noting that the Fed, headed by Alan Greenspan, raised interest rates again just the day before, Mr. Cohen added: ''The market is spitting in his eye.''

Top 15 Nasdaq Companies as of March 10, 2000, by Market Cap

Meanwhile, Nvidia’s at over 24x sales.

Net % of banks tightening commercial/industrial lending standards.

This data is from February 2023 - before the collapse of Signature and Silicon Valley Banks. The other times we were at these levels going up were 2020, 2008 and 2000. Quite a group.

For commercial real estate news, the Treppwire Podcast is very good. Just like I’m generally glass half-empty, they’re always glass half-full. Recently I made up a list of podcast suggestions if you’re interested.

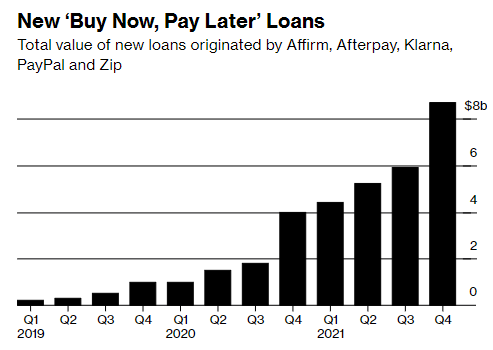

"The fact that a large group of people need to break up a 20 dollar phone charger into four installments is a sign of just how bad things are. I keep seeing these buttons on more and more websites, and for items that cost $20 or even less."

- a comment I saw in 2021 from someone going by ‘thorosaurus’

Then again, what’s $8 billion, 2 days of Fed QE?

Mortgage Delinquencies Hit Record Low in March

Open House. The comments here are interesting.

Some color on the “tax on higher credit scores” story:

the change amounts to a tweak of an existing fee structure in favor of those with lower credit scores and at the expense of those with higher credit scores, but there's no scenario where someone with lower credit will have a lower fee. In other words, don't go skipping those credit card payments in the hopes of getting a lower rate.

It’s still a rule change messing with markets via bad incentives, but oh well.

A federal court indictment claims Miramar’s Carl Charles and his brother, Patrick Charles, got over $2.5 million in COVID-19 relief funds in 2020 and 2021 by claiming pandemic hardship for businesses that had no revenue or existed only on paper before the pandemic.

Broward County property records say Carl Charles and companies run by him bought at least 14 houses during the period federal prosecutors say the brothers ran the scam. Those companies or companies with a connection to Charles still own nine of those homes.

EIDL refers to the COVID-19 Economic Injury Disaster Loan, and PPP is the Paycheck Protection Program. Here’s a link to the subreddit mentioned.

When I quote random, anonymous people like this, take it with a grain of salt, but experience has taught me that this type of bottom-up research is much more useful than listening to, say, Steve Liesman or Janet Yellen.

The poster below says he is in a “Top 20 metro area. Midwest. Suburbs about 20min drive from downtown. A majority of our homes are $1300-1800 rents.”

“I manage 250 single family home rental portfolio. What I’m seeing.

Slower to rent vacant units. They rent, but moving much slower then sale market. We have to drop prices $25-50 after a few weeks on market. Although some units rent within a few days, others take 3-4 weeks. Back when interest rates began to rise, i predicted rental market would boom. Purchasing affordability has been hit hard, so cheaper to rent right? So far I’m wrong, sale market is somehow hotter then rental market.

Houses we bought 2012-2021 are cash flow monsters. These buys have much lower loan rates, rent growth has been massive. Very tough to sell these assets with the cash flow being so high.

Tenants are staying put. Very little turnover. Too expensive to move? Saving longer for a downpayment to buy own home?

Costs are way up! Materials for repairs/turnovers are high. Few years a go doors were $130, now $330. Sure rents have gone up 30% but materials and labor have basically doubled.

Tough to find new buys. Numbers don’t work on anything, unless you fudge them and add in future rent growth which if obviously not guaranteed.

In conclusion I don’t think many landlords will be selling anytime soon, or buying much anytime soon either. Rent growth has also slowed way down.”

The poster adds: “We never go north of 50% LTV. Right now we are around 42%. We do mostly commercial blanket loans that reset every 5 years. However I always opt for the 20 year amortization to help pay down debt much quicker. We always stress test the loans and see what happens if they reset to 10-12% and we will be fine. Keeping total portfolio LTV at 50% max and only doing 20 year amortization is key for safety.”

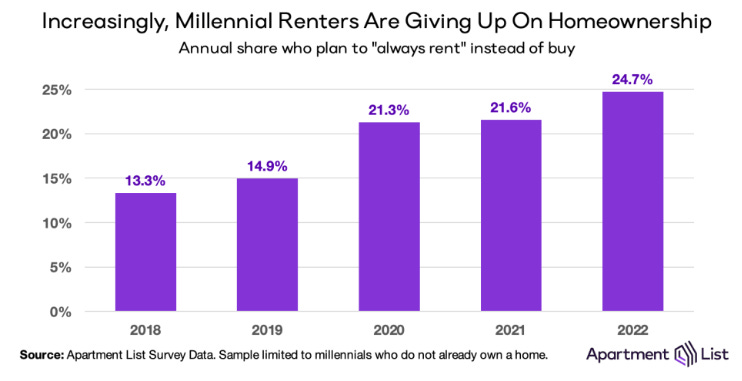

Millennials have reached 50 percent homeownership slower than previous generations

The Global Economic Conditions Survey (GECS) is one of the most comprehensive surveys of its kind, both for its number of respondents and for the range of economic variables it monitors.

An interesting read someone sent me: A Fundamental Explanation of UAPs

“I found things that even more people believe, such as that we have some knowledge of how to educate. There are big schools of reading methods and mathematics methods, and so forth, but if you notice, you’ll see the reading scores keep going down—or hardly going up—in spite of the fact that we continually use these same people to improve the methods. There’s a witch doctor remedy that doesn’t work. It ought to be looked into: how do they know that their method should work?”

Richard Feynman, Cargo Cult Science, 1974

See also: 23 Baltimore schools have zero students proficient in math, state test results reveal

"Don't take any guff from these swine."

I watched an episode of a series called (Re)solved, about the death of Bob Saget. The story essentially is that he fell in a hotel room, hit his head, and then went to bed and died. There was no blood, and his skull was basically bashed in, as if he’d fallen multiple stories, or been hit by a car, according to a couple doctors quoted. Very odd. Here’s an emergency medicine thread on the topic.

During an undercover drug sting this week, Riverside County sheriff's deputies lost almost 60 pounds of methamphetamine when they couldn't catch up with the person they sold it to.

From Tournament Poker for Advanced Players by David Sklansky. I’ve been thinking about these passages after discussing them at a game recently, wondering if there’s an investing angle here. Clearly when I (or you) invest, we’re up against better players. How can we get an edge?

For me - everyone’s different - I think not having clients is an advantage, because I have a habit of looking kind of crazy for periods before suddenly looking very smart. If I had someone calling me daily yelling, “Why the hell are you adding to that position that’s down 20%?!!” I don’t think I’d be managing money very long.

Also, I’m never levered up, and I don’t panic. Those two things always seem to go together, don’t they? Leverage and panic? At least on the way down. Also a sense of humor helps a lot:

In general this book has assumed that you play as well as the best players in the tournament, and better than the rest. But what if you don’t? While this possibility will not be addressed in regard to other games, it could be relevant to no-limit. Suppose, for instance, it occurs that you are better than the average player, but definitely not as good as the top players in the tournament.

If this was a pot-limit, rather than a no-limit tournament, the overall situation would be unprofitable. The edge you have against the bad players would not make up for your disadvantage against the best ones. But no-limit is different. Why? Because you can easily get all-in before the flop.

It turns out that a willingness to do this can be a tremendous thorn in the side of a top player. With the exception of two aces, no starting hand can ever feel that comfortable if all the money goes in before the flop. And, if you feel like you are playing against better players, you can take advantage of this fact.

A Proposition

Suppose I walk up to a world champion hold ’em player and offer him the following proposition: A heads-up $5,000 no-limit hold ’em freezeout. We play until one of us has the whole $10,000. The blinds are $100 on the button, and $200 in front of the button. But now I add a little wrinkle. I will move in all of my chips before the flop every hand! It doesn’t matter what I have. Clearly, my opponent has an edge. But how big is it?

Suppose I tell him I will play this freezeout if he doubles my win when I win. In other words, he pays me a total of $10,000 those times I win, while I lose only $5,000 when I don’t. Should he accept?

Believe it or not, the answer is definitely no. Even if he plays perfectly, he will win this freezeout only about 60 percent of the time. With a little thought you should be able to see why he can’t lay 2-to-1.

Let’s look at this a little closer. Suppose, for instance, on the first hand he is dealt

What should he do? That hand is a favorite against my two random cards, but the problem is that it is not a 2-to-1 favorite. The actual percentage is 57 percent. Thus, if he calls my bet he is laying 2-to-1 on a 57-to-43 or 1.33-to-1 shot. So it would seem like he needs to wait until he has a hand that is much more of a favorite than this one.

The problem, of course, is that he is being ground down while he is waiting. So when he finally does get a good enough hand to play, (which by the way would be a hand that has a less than 66 percent chance once chips are not even) he not only risks going broke on that hand, he also leaves you with chips, sometimes a significant number of them, even when he wins the confrontation.

The point is that no-limit hold em, with all of its skill, is a game where a very aggressive pre-flop strategy can negate that skill. It is like a boxing match where you find yourself against a better fighter. In such a case, since you have little chance of winning a 10 or 12 round decision, you are better off going for a knock-out punch, even if that is not your normal style.

I just learned that their new tagline is “Live Ambitiously”

A lot of great info in this post....feel like I went to housing church this morning :). Thank you.

Invitation has got a real problem with its lawsuit in CA over doing work without permits. https://www.washingtonpost.com/business/2022/07/12/invitation-homes-corporate-landlord-permits/

Lots of insight in this one - as a person who loves her home and always has since a child, I feel for those unable to afford their own. To own one’s own roof is far more than ‘getting on the ladder’, it truly is one’s castle and place of feeling safe. As for the small-time landlords, there is a place for them and I’ve read they play an important role to their community (key word there); it’s the big corporates who’ve turned home ownership into an asset class and feel no obligation to the communities in which they operate who are a pox on society - unless the tenancy laws change to the German style (rental is commonplace in Germany). Despite all the headwinds, there is something hopeful about the ‘optimistic’ consumer confidence data - gotta hand it to Americans - they don’t go down without a fight (or sadly a scam as you also showed).