Trainspotting.

We are colonized by bankers.

“The potential macro-economic benefits of easing the Zero Lower Bound constraint appear to be significant.”

- Bank of England Chief Economist Andy Haldane, November 2010

“Negative rates are probably the dumbest idea in the entire history of finance and we’ve just been living through it.”

- Financial Historian Edward Chancellor, September 2022

Are there any clawbacks on Andy Haldane?

What current Chief Economist of the Bank of England Huw Pill doesn’t say here is that the people in the UK are poorer largely because of the policies of the Bank of England.

Bank of England apparatchik Huw Pill reminds me of a scene from the 1996 movie, Trainspotting:

Tommy: Doesn't it make you proud to be Scottish?

Mark "Rent-boy" Renton: It's SHITE being Scottish! We're the lowest of the low. The scum of the f**king Earth! The most wretched, miserable, servile, pathetic trash that was ever shat into civilization.

Some hate the English. I don't. They're just wankers. We, on the other hand, are COLONIZED by wankers. Can't even find a decent culture to be colonized BY. We're ruled by effete arseholes.

I’m not British, forgive the profanity - but I love the word Wanker. It’s very fitting and concise, like Putz.

Unelected, unaccountable central Bankers like Huw Pill now rule the world.

We are all colonized by wankers.

“The greatest enemy of authority, therefore, is contempt, and the surest way to undermine it is laughter.”

Hannah Arendt, On Violence

A timely podcast from the great Grant Williams with Brendan Ballou, author of the upcoming book, Plunder: Private Equity’s Plan to Pillage America.

The plague of private-equity locusts in America was a frequent topic on my Twitter account (plus the tendency of their CEO’s to be buddies with Jeffrey Epstein.)

As you may know, Jerome Powell is a private-equity guy, which I wrote about in We need to talk about Jerome.

Ballou: Are there specific industries where private equity seems to be particularly enamored? And so there have been some headline industries that I think your listeners are probably familiar with, whether it’s nursing homes, physician staffing companies, and health care more broadly, prison services, single-family rental homes, and mobile homes housing generally. And I think one of the interesting discoveries of this project, and there are a lot of nuances to this, is that, in a lot of ways, many private equity firms target businesses, not ones that cater to the rich, but rather that ones that cater to the poor, which was an interesting discovery. And I think part of the reason is those are the industries where the firms are going to have a large ability to raise prices and potentially decrease quality care without consequence because the customers really don’t have an alternative.

Reminds me a bit of Elizabeth Warren’s 2010 FCIC testimony1 (before she went full identity-politics): “a far more profitable model of lend widely, and in large amounts, and reap large short-term profits from people who have only a marginal capacity to repay.”

This is interesting: Zimbabwe’s central bank to issue gold-backed digital currency

We may have to invade Zimbabwe soon to prevent this. Bring ‘em some freedom and democracy.

Investors Lost Money on 14% of Homes They Sold in March—Nearly the Highest Share Since 2016

But they made it up in volume!

Roughly one of every seven (13.5%) U.S. homes sold by an investor in March sold for less than the investor bought it for. That’s comparable with February’s 14.5% rate—the highest since 2016. It’s also nearly triple the share of a year earlier and compares with a record low of 2.8% in May. By comparison, 4.8% of overall U.S. homes that sold in March sold at a loss…Roughly one in five (20.8%) homes sold by flippers in March sold at a loss, higher than the 13.5% share for investors overall. For the purposes of this report, we define a flipper as an investor that bought a home and resold it within nine months…

In Phoenix, 30.7% of homes sold by investors in March sold at a loss—the highest share of the 40 metros Redfin analyzed and more than double the national rate. Next came Las Vegas (28%), Jacksonville, FL (20.9%), Sacramento, CA (20.2%) and Charlotte, NC (17.4%)…“Most of the investors I see selling now are mom-and pop-investors,” said Las Vegas Redfin real estate agent Shay Stein...

While a lot of large investors are holding onto their properties, iBuyers (instant buyers) are the exception, according to Stein. Many iBuying companies, including RedfinNow, ceased or slowed operations in the last two years and are now trying to offload inventory. That’s likely part of the reason that some markets where iBuyers had a large presence, including Phoenix, Charlotte and Las Vegas, have seen an uptick in the share of investor-owned homes selling at a loss. Redfin shuttered its iBuying operation, RedfinNow, in November 2022…

Investors owned 10.1% of new listings on the market as of December, the most recent month for which listing data is available. That’s down from a peak of 12.4% a year earlier

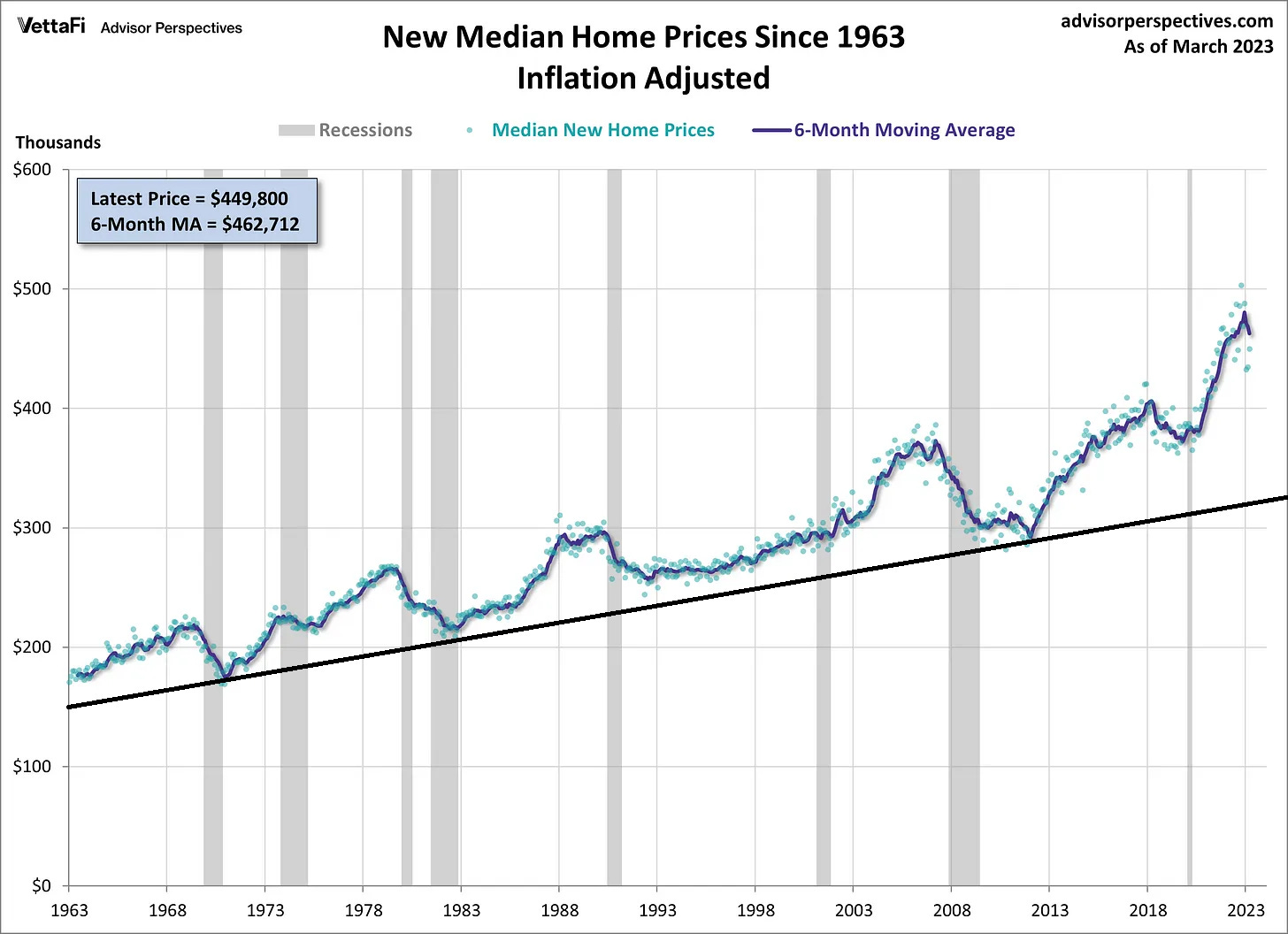

New Home Sales Surge 9.6% in March

So far new home sales, while down, seem sort of middle of the road historically, although on a population-adjusted chart, we’re down to early 1980’s levels, but not 2011 levels.

I’m not trying to do technical-analysis on a home price chart below, but for what it’s worth, there is a clear black trendline (which I added), and we are far above it. Then again, central bankers and politicians seem much more reckless and profligate than they used to be.

FHFA House Price Index Up 0.5% in February, Higher Than Expected

U.S. house prices rose in February, up 0.5 percent from January, according to the Federal Housing Finance Agency (FHFA) seasonally adjusted monthly House Price Index (HPI®). House prices rose 4.0 percent from February 2022 to February 2023.

There are a number of house price indices floating around, and they all seem to have slightly different numbers. Still, it seems overall that nationally house prices are still rising, just not at the insane, Fed-induced 20% annual rate that some people - mostly those who profit off of higher house prices - want you to think is normal.

FHFA U.S. House Price Index, nominal and real.

Now here’s the problem with reducing nominal down to “real”: There’s an assumption somehow that everyone’s purchasing power also rises along with the CPI rate. It does not.

There’s an assumption that the CPI reflects that actual cost of living. It does not. Heck, the CPI methodology has changed a several times over the years, always to reduce reported CPI.

As I pointed out yesterday, before 1971 no one said, “adjusted for inflation.” The U.S. currency changed.

An economist would look at this chart and say, oh well, adjusted for inflation, home prices are just slightly elevated. That’s nonsense. House prices are much higher today relative to incomes than they were 20 or 40 years ago.

Again, to me LEVELS matter more to normal people than rate of change.

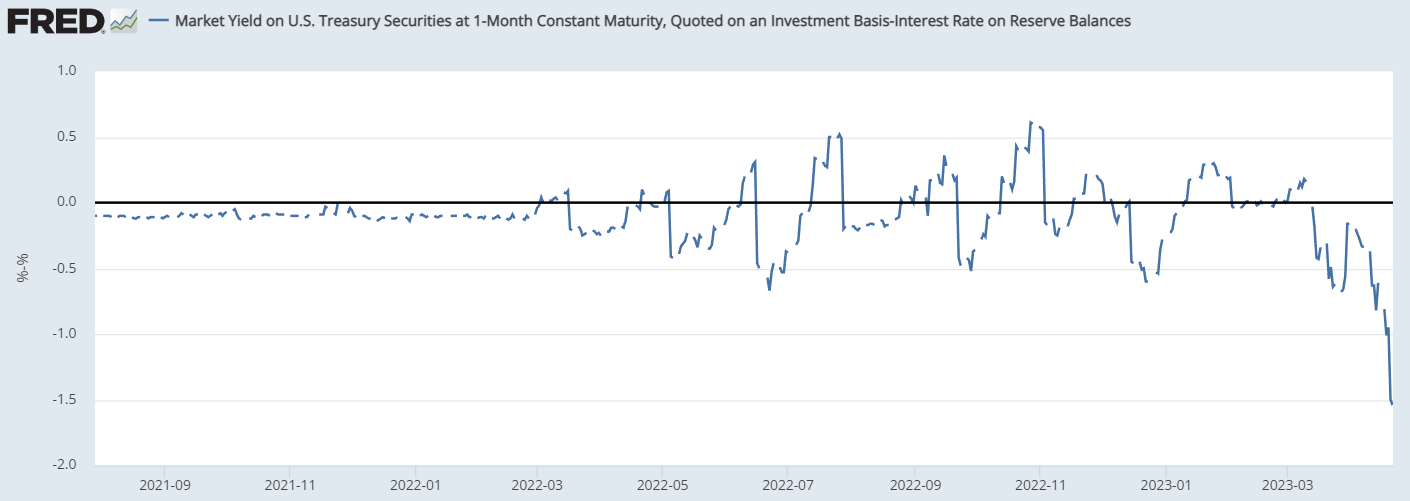

I don’t have a longer-term chart, but this is what Jeff Snider has been talking about as evidence of a strong demand for the most safest collateral - the 1-month T-bill yield minus the Interest on Reserve Balances, which is now 4.9%.

Apparently Bitcoin block number 666,666 from January 18, 2021 has a line from Romans 12:21:

“Do not be overcome by evil, but overcome evil with good.”

Good advice for all of us.

The other thing I noticed from the article was this:

Are we really still doing the NFT thing?

“…under conditions of terror most people will comply but some people will not, just as the lesson of the countries to which the Final Solution was proposed is that “it could happen” in most places but it did not happen everywhere. Humanly speaking, no more is required, and no more can reasonably be asked, for this planet to remain a place fit for human habitation.”

- Hannah Arendt, Eichmann in Jerusalem: A Report on the Banality of Evil

“...it would be important to think about the increasing economic fragility of middle-class families, starting in the 1970’s: a combination of flat wages for fully-employed men, and rising core expenses in housing, in healthcare, in transportation – put a lot of pressure on middle-class families.

Many families responded by sending, if they had two parents in the household, sending both parents into the workforce. That kept family income rising, but it was taking two earners to get them in a position where one earner would have been a few years earlier. Core expenses continued to rise, families stopped saving, and began to take on more debt, to make ends meet until the end of the month, or deal with emergencies that came up. The consequences of job loss or unexpected medical bills became harder and harder hits on the family...

That’s the position that families are in when they hit the, really the late 1990’s. So, families are taking on more debt. The consumer credit market is largely deregulated starting in about 1980. Credit cards are effectively deregulated – when I say “deregulated”, the usury laws were the “tent pole” of consumer regulation since the Code of Hammurabi in the 15th century B.C. through Biblical times through Colonial times in America, through every state in the union. That tent pole of usury is knocked out, effectively, first for credit cards in 1979 and then explicitly by Congress on mortgages in 1980.

It takes more than a decade for the industry to begin to adapt new business models, but the old model, of screening customers carefully, and only lend to those whom you have a fair amount of confidence will be able to repay, gave way to a far more profitable model of lend widely, and in large amounts, and reap large short-term profits from people who have only a marginal capacity to repay.”

I listened to Grant’s conversation with Brendan Ballou last night and am chomping at the bit to read the book when it appears in two weeks time. Meanwhile I was rivetted by the same quotation citing PEs focus on lower income segments whose power to resist was immeasurably more constrained than the rest, that you quoted. I also reflected on the fact that a similar British insult is “You pillock” or in the shortened version “You pill” which is a slightly politer way of calling someone a wanker. I think the Welsh spelling is “Huw Pill” or something like that.

I too use Wanker fairly often. It is one of the best UK contributions to the insult lexicon. Ever since Jim Kunstler referred to Krugman as a 'fatuous wanker' the label stuck and I use it every time I reference anything Krugman.

'Plonker' and 'tosser' a good ones I like to toss out occasionally. And of course, Shakespeare had some priceless gems, 'three inch fool' and 'beef-witted' to name two of the best. No one does English insults better than the English. I wish Americans could cuss and belittle so eloquently.

https://anglotopia.net/anglophilia/british-english-the-top-50-most-beautiful-british-insults/