Trust is everything

There are no bond vigilantes. None.

"Those at the top have become so disconnected from reality that they don't appreciate how wide spread the the pain really is today."

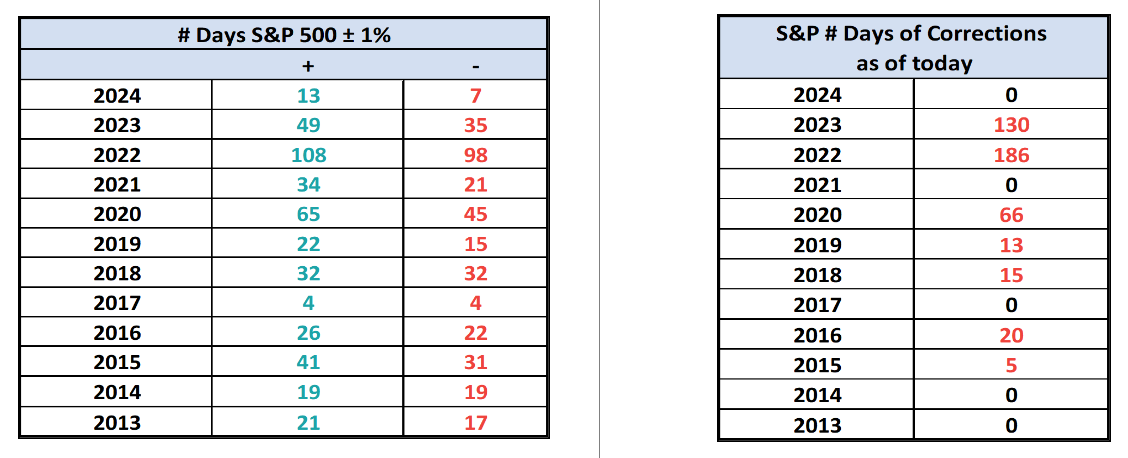

Here's a table with the number of days of a 1% or greater change in either direction and the number of days of corrections (down 10% or more from the record high) going back to 2013.”

I was talking the other day to AT&T support, and the guy who was helping me was very chatty and friendly. He asked me what I did and for some reason I just said, “Real Estate,” and he started telling me about his small Tennessee town, and how expensive it had become in the last few years, partly due to an influx of outsiders. I asked him how much housing had risen over that span, and he said - ballpark - a 2BR, 2BA had gone from $150K to $250K, and a 1 BR apartment had gone from $400 to $650. I asked if wages had gone up and he laughed. Barely. He said they never really had a homeless problem and now they do. People can’t afford housing any more. He’s union, so he’s doing better than most, but his community has been permanently altered, and not for the better. We talked for a long time.

He hopes the new arrivals won’t vote for the same policies of the states they left. He also mentioned that his very sleepy downtown had a number of fancy new businesses spring up, peaking in 2022. Most are now closing. Nobody local has the money to support them. I tried to offer him some hope of a return to normalcy (meaning some housing deflation, or at least a retreat from utter insanity), but that’s all it was - hope. Now multiply my conversation by thousands of communities across America.

“There are no bond vigilantes. None.”

If you don’t get the paid version, and are curious. go through my substack archive and check out all the free stuff I have written (the ones without a padlock.) I started in 2022 and there’s a bunch of free stuff, including a number of single-topic writeups. I previously had done daily emails to friends and friends’ friends from from 2009 to 2021 (and even before that to a much smaller audience.) Those emails were similar to what I do here on the Substack.

With the paid version, you get lots of eclectic charts, interviews, news, music you don’t like, odd pictures, and brilliant commentary! (from other people, not me.) Each edition should generally tide you guys over for a week or so. No rush. It’s a buffet, not a shot. Believe me, I leave a lot out.

I try to include things that pop out to me, but aren’t done to death in the MSM (e.g., I don’t pore over things like “the jobs numbers” much.) Like my Twitter (which is even more eclectic and weird), I try to post stuff I’d like someone else to post for me to read. Mostly it’s financial-related, but not always. To be honest, as a skeptic (not a cynic), I tend to have a glass half-full - but cracked - view of markets (by the way, this does not necessarily mean a bearish view) - but if you want Bubblevision® (thank you, Bill Fleckenstein), there’s always CNBC.

I think next I’ll work on Part 2 of “Before the Deluge.” I may un-paywall Part 1 shortly. Stay tuned. Also I may eventually write something short on Stefan Zweig’s, “The World of Yesterday,” and may do some short housing-anecdote posts. It’s mostly stream of consciousness, like Kamala Harris.

Thank you all for thoughts and prayers. I am recovering nicely after just one week. I feel very encouraged and positive about a 100% recovery.

A Search reminder:

Paulo Macro with Grant Williams and Bill Fleckenstein

“Politicians, if you tell them, “These [debt] numbers are catastrophic,” they’ll say, “Well, where’s the ten year?” And you say, “Oh, four and a half.” And they go, “Okay, so what’s the problem?” They’re not going to do anything. You got to take that 10-year to 6%, 7%, 8%, and really scare the pants off of them, maybe even get them to lose their jobs with the next guys who come in when people get fed up at the problems that this is creating in society, and country, and the economy.”

“There’s this moment when we kicked the gold standard entirely, and closed the window under Nixon, that people forget that pressure that was building up in the late ‘60s, because the French were getting the joke that we were doing something else, that we weren’t going to start paying our bills ever again, maybe. And just the introduction...Can you imagine lending money to America on and off for 200 years, and always getting the money paid back, and the debt being zeroed, and then, suddenly, you have this gradual awareness and awakening after a few years in the ‘60s, like, “Maybe these freaking guys, they’re just going to borrow without any intention of ever paying us back, and they’re going to just find ways to not do that.”

“Generative AI is going to be the biggest f***ing airball in financial history.”

“America's becoming Brazil. That's sort of the way I think of it.” - Demetri Kofinas, summarizing Paulo’s position

(fyi Paulo’s latest substack post is titled: “Sorry Jerome: I see the 'Stag' and the 'Flation'“)

Here’s a new podcast Paulo Macro and Le Shrub with Demetri Kofinas. The boys mentioned copper in the second hour:

Stop signs replace some Oakland traffic lights to deter copper theft

“Oakland has removed the traffic lights from one intersection and replaced them with 4-way stop signs due to people stealing copper and then tampering with an electrical box…"It's just telling us that the city is giving up on us," said Tam Le, owner of Le's Auto Body & Engine Repair, located at the corner of the intersection. Neighbors said the lights that were there before hadn't worked in months, either blinking red or being completely out…"If you really want to fix the stop sign, I think you really have to clean up this homeless encampment," said Le.”

Surreal.

A favorite quote of Paulo’s from the memoirs of Herbert Hoover:

“During this new stage of the depression, the refugee gold and the foreign government reserve deposits were constantly driven by fear hither and yon over the world. We were to see currencies demoralized and governments embarrassed as fear drove the gold from one country to another. In fact, there was a mass of gold and short-term credit which behaved like a loose cannon on the deck of the world in a tempest-tossed era.”

“I love that notion that the President of the United States had this understanding that capital flows across borders started to go haywire as whole countries began to feel uncertain about their savings and their positions and where their surpluses were being parked, for lack of a better term.

This ties in a little bit to the geopolitical angle, which is not a specialty of mine. I think people still today wildly underestimate the damage that we may be doing by confiscating Russia's FX reserves and then threatening to turn around and use them to give them to Ukraine. The uncertainty that this creates for whole governments in parking their money in the deepest pool there is, which is the US treasury market, cannot be overstated.”

Paulo Macro

“Maybe the real yield is wrong.” - Paulo

“Maybe the real yield is wrong. Maybe real yields are negative. What if inflation actually is running 6%-8%, but we all buy into this CPI, heavily-adjusted?”

Paulo: I think that, in general, people feel like they're being screwed with on some level and they can't quite diagnose why. Inflation is a big part of it.

Demetri : They feel like they're being gaslit, economically gaslit.

“I mean the fake data doesn't help.” - Shrub

“I mean the fake data doesn't help. So let me just give you an example that I thought was quite funny. If you remember, there was a CPI report a couple of weeks ago, and the CPI report was hot, and then the next day, there was a PPI report, and the PPI report was cold. So the market ripped on that. I was like, oh, that's quite strange. So I went to look at what was happening, and I think the gasoline price inside the PPI report was down month on month.

I know from our commodity - I track commodities - gasoline was actually up like 6% on the month. So I'm like, how can they mark down gasoline month on month? Actually, in real life, it's up 6%. I checked the details, and it was a seasonally adjusted gasoline price. I'm like, how can you make a seasonally adjusted gasoline price [lower] in the inflation print month on month when, in real life, it's up 6%? I jokingly said, Guys, to my American friends, when you go to the gas station, just please ask for the seasonally adjusted gasoline price.”

Shrub

“That's why I'm happy to be running a parody publication, because through parody we can identify that the whole market is a parody. Right?” - Shrub

Rice. Nobody eats rice, right?

“Underwriting the system isn't just dollars - dollars rely on this other thing called trust”

David Lin: Are you concerned about another financial crisis now?

Mehrsa Baradaran: Absolutely. We've been on the ledge of financial crisis, I would say since SVB. We are at a point where capital’s search for yield has reached kind of the beyond the point of it being profitable. It is now turned in on itself, there is so much risk,and capital still needs to make yield like over 6%, year after year, and the risks have mounted sufficiently on those balance sheets that they really are being supported by the Federal Reserve at this point. I think the Fed's going to keep pushing that button. They've showed that they're never going to let the thing fail, and they there's plenty of money, right? Money can just be printed, so I'm not worried about that. I am worried, though, that the fed and the banks misunderstand. The thing is, underwriting the system isn't just dollars, dollars rely on this other thing called trust, and when trust goes it evaporates quickly, and we saw precursors to it during the financial crisis.”

“I was out to drinks with a buddy last night, he's Turkish actually. So the two of us were having a hearty laugh about EMF-ification, and we were talking about how consumers and individuals' behavior changes as the currency is screwed with under the covers, and remembering that the dollar is really just a placeholder or a chit for a handshake. The trust is everything. You cannot exchange one thing for another without having something that you can put behind the handshake.”

Paulo Macro

The Consumer

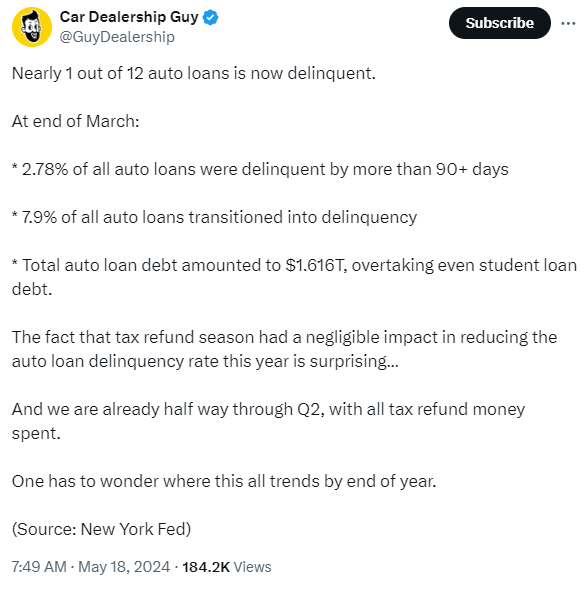

“NY Fed out with their quarterly household debt report just now for Q1. Here's what we're looking at: slope, not levels. Reminder: Student Loan delinquencies are not being reported until Q3 (for now).”

“Those who are maxed-out, are increasingly delinquent.”

Philadelphia Fed: Large Bank Credit Card and Mortgage Data 2023 Q4 Narrative

“Credit card performance further deteriorated at the end of 2023, with firms recording the worst 30+, 60+, and 90+ account-based days past due levels in the reporting series.” [which dates back to 2012]

Below is from the St. Louis Fed. Pretty remarkable, considering how wonderful the economy is for Paul Krugman:

The above is “the percentage of people with delinquent credit card debt.” My first thought was that we are near all time highs in all categories except the richest 10%. Not surprising. My second thought was why wasn’t 2008-2009 the worst?

The second chart - the percentage of credit card debt - provides some insight. The percentage of credit card debt delinquent in 2008 was the worst, all around.

Then again, from the Kansas City Fed:

Stephanie Pomboy: Exhausted Consumers Are "Spent Up & Lent Up", So Economy Will Slow “Total real consumer spending in the first quarter was up $97 billion…in real terms, $74 billion of that was non-discretionary - stuff like…housing, healthcare and insurance. Real incomes in the same quarter were up 44 billion, so you had incomes of $44 billion spending of $97 billion, and so what you're seeing is consumers are clearly drawing down their savings, running up credit card balances as we know already, to support just the basic lifestyle.”

From friend of the show Paul M.

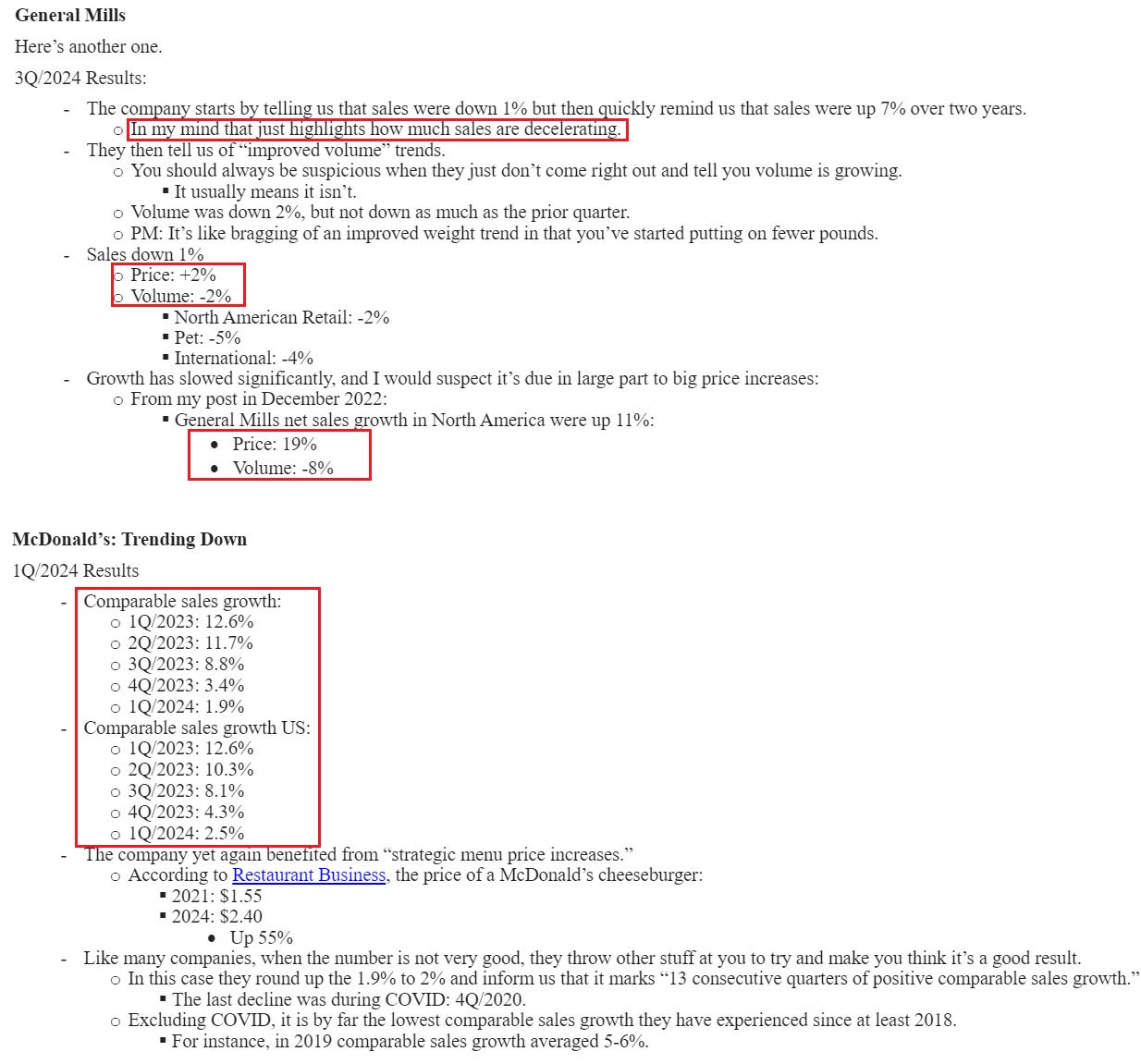

General Mills and McDonald’s. I highlighted some things I’ve been watching for a while now:

Discover Financial credit card net charge-offs spike

Commodities are out of vogue

Record Lows: real assets relative to financial assets since 1925

Hedge Fund Exposure To Energy Historically Low

Natural Gas as an A.I. Play

“If you really kind of dig in, it becomes very clear, very quickly that large language models and A.I. are going to need either natural gas, coal, or or nuclear power to power. Renewables simply won't cut it, and it's not just because they're intermittent day and night. Even if the sun is shining straight on and there's no clouds in the sky the variation in the solar radiation that hits the earth, and the variation in the dispatch just second to second - the quality of the power is not suitable to run it through these really sensitive electronics, so even these green data centers, they basically buy green credits, and then run their data centers on natural gas.

So natural gas, coal, or nuclear has to be the answer to these things, and it's not going to be coal I don't think in the United States. I think it's going to be very difficult to permit new coal-fired power plants. In fact, I would say it's almost impossible, and it'll probably be gas.”

Jim Grant is the best.

Here’s his introduction of Sean Fieler, president and CIO of Equinox Partners.

“I'm going to put it this way - we were talking earlier about how to characterize your investment career, apart from distinguished, and I would draw a distinction. There's a kind of Wall Street career that one might describe as kind of the 72 degrees Fahrenheit career. It involves obtaining of a CFA Charter certificate, it involves perhaps a couple of years in the training program at Goldman Sachs, on to one of the big management companies, mostly long the S&P 500, and retiring at the age of 47 with about $65 million. That's one way to go. It's not the way for Sean Fieler to go.

Sean chooses another way, which is to pick the most obscure countries that you wouldn't want to visit, invest in them, and buy gold bullion instead of Bitcoin, and then come on the Grant's podcast. That's Sean Fieler.”

Sean Fieler:

“I think Treasury and the Fed have become very adept firemen [and arsonists - rh]. I think their ability to paper over anything that looks like it's going to go wrong right away - even before it happens, even before we see it - they've gotten very good at that, and I think inflation is ultimately the check against that, and that's the world I think we're moving into, and I don't think markets have priced that in.”

Housing

Phoenix Housing Inventory Back to 2019 Levels

“You literally could be buying a home in a subdivision and be competing against BlackRock…it used to be that real people that were moving into a neighborhood - you had a real neighborhood. Now it's very very different. You've got short-term, you have long-term, you got Wall Street in there, and then of course you got this whole swath of of people looking to buy second places and renting them out by the night, and you know that the whole industry has just boomed and that's actually made it worse for the single family home buyer…

I'm in escrow right now on a big project in Las Vegas, 357 units. We get all the data, and we're starting to see people not paying, delinquencies, so when you start to see delinquencies, you start to see what we call skips, where they move out and they owe balances, you start to see high collections, and you start to see a rise in evictions and those kinds of things in some of these markets, which is stuff that I watch. We're in Oklahoma, we're in Austin, we're in Houston, we're in San Antonio, we're in Dallas -we we're all over uh Texas. These are different in each market, but the patterns are not. The people are getting squeezed.”

John Rainey used the word “Stretched” during the Walmart Conference Call:

“Many consumer pocketbooks are still stretched, and we see the effect of that in our business mix, as they're spending more of their paychecks on non-discretionary categories and less on general merchandise.”

CRE

Mike Comparato: ”Five-hundred to one-thousand bank failures? Absolutely…there’s going to be another 500 to 1,000 bank mergers, where banks are going to have to shore up balance sheets by combining, cutting costs, cutting personnel. I really don’t think the general populace appreciates how bad bank balance sheets are right now. I don’t think most of the banks understand what’s on their balance sheet. I don’t think the banks understand how bad what’s on their balance sheet is, and they’ re basically being told what to do by Federal regulators, and that’s equally as terrifying.”

“Office is really bad. It’s really, really bad, and we’re seeing the trades, we’re seeing it happen, and the market is kind of ignoring it, and I don’t understand why we’re ignoring how bad it is. You’re seeing office assets in L.A. trade for less than $100 a foot. You’re seeing office assets in Chicago trade for $50 a square foot. When you’re the building across the street, and you’ve got $150 a square foot debt, and the one across the street traded for $50, what do you do? We’re just pretending like this isn’t happening. It’s happening. The trades are happening, the foreclosures are happening, the REO sales, the bad loan sales are happening, values are down 70% or 80%, and we’re pretending like it’s not happening. It’s bizarre to me. How do you value an office building today? I asked the CEO of an office REIT how do you value an office building today. Historically there are two answers to that, NOI and Cap Rate. Those words were not used in valuing the office building. You don’t know how to value an office building today.”

The KBW Bank Index vs the S&P 500 since 1995

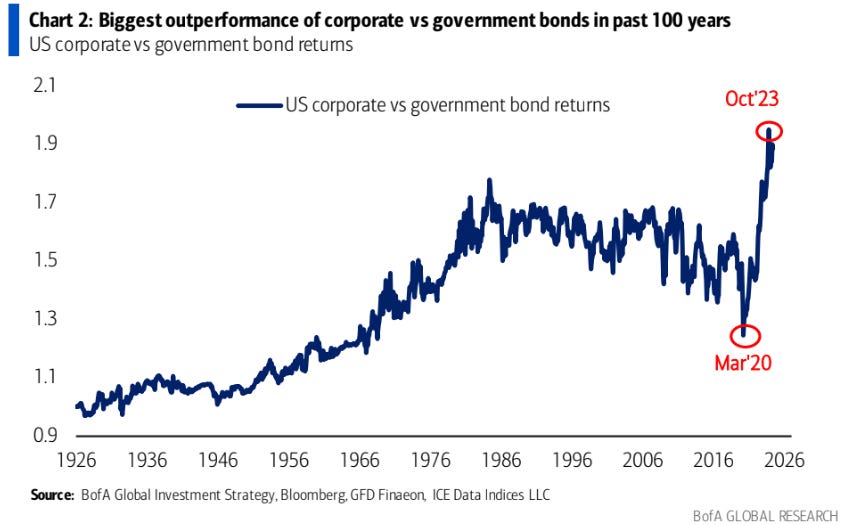

Corporate Bonds vs Government Bond Returns

Starwood’s $10bn property fund taps credit line as investors pull money. “Heavy redemption requests come as fears rise over real estate valuations”

“Starwood Real Estate Investment Trust (Sreit), one of the largest unlisted property funds, has drawn more than $1.3bn of its $1.55bn unsecured credit facility since the beginning of 2023 following heavy redemption requests…

At the current pace of redemptions, Sreit would run out of credit and cash in the second half of this year unless it borrows more or sells more property assets. Both Starwood’s fund and a larger rival run by Blackstone Group raised and invested tens of billions of dollars in commercial property shortly before US interest rates began to rise in 2022, generating substantial fees for their private equity owners and financial advisers who sell the funds to wealthy clients.”

“US apartment rents could be under pressure this year as a record supply of new homes hits the market in 2024, according to Yardi Matrix, a real estate data provider. Such forecasts have weighed on the valuations of public Reits invested in US multi-family housing, with shares of Mid-America Apartments and Camden Property Trust, down more than a third from their late 2021 peak.”

I will note that in the latest Trepp podcast (#257) the perennially bullish CRE show actually - for the first time I’ve noticed - mentioned “B and C multifamily” in addition to “office” as being in big trouble.

Keith Dicker tells a joke: “How you know when a central Banker is lying? Their their lips are moving.”

Very good discussion and charts on “The Business of War” by The Mad King (paywall)

“In 2022, the US spent $811 billion on military expenditures, while the combined total for the other 31 NATO members was $370 billion. This significant gap is challenging for the US to justify, especially when it comes to agreeing to fight alongside its allies if needed.”

“To get the screwworms out, the USDA to this day maintains an international screwworm barrier along the Panama-Colombia border. The barrier is an invisible one, and it is kept in place by constant human effort. Every week, planes drop 14.7 million sterilized screwworms over the rainforest that divides the two countries. A screwworm-rearing plant operates 24/7 in Panama. Inspectors cover thousands of square miles by motorcycle, boat, and horseback, searching for stray screwworm infections north of the border. The slightest oversight could undo all the work that came before.”

: it looks like a fantasy novel place and it really exists. It's called Ball's Pyramid.")

“A man identifies himself with the unit of his money ; doubt cast on it offends him and, if it is shattered, his self-confidence is shaken. He feels slighted and humiliated by the lowering of the value of his monetary unit and, if this process is accelerated and inflation occurs, it is men who are depreciated until they find themselves in formations which can only be equated with flight-crowds. The more people lose, the more united are they in their fate. What appears as panic in the few who are fortunate enough to be able to save something for themselves, turns into mass flight for all those others who have become equals by being deprived of their money.”

Elias Canetti, Crowds and Power

The savings rate topped out 2 years ago with pandemic handouts and inflation topped out 2 years ago with supply chain issues. Corporations successfully used this to manage higher prices while the economy was in flux and that advantage has expired. Absent further stimulus, flat / negative volume growth will soon be met with flat / declining inflation and corporate sales will decelerate faster than most expect, resulting in the next recession.

The kicker: if the Fed keeps rates 4-6% (I think they should) even with a slowing economy, that $500K house that went to $1M 2 years ago, will need to come back to $500K before it's all over. My expectation is that they'll cave and housing won't come back enough to save the current generation of household formation.

Glad to hear your on the road to recovery. Also, speaking of defense spending, check out this chart on NATO spending: https://www.visualcapitalist.com/breaking-down-1-3t-in-nato-defense-spending/. Seems like influence peddling costs a pretty penny.