"Insanity is repeating the same mistakes and expecting different results."

Narcotics Anonymous, November 1981

“Millions of Americans are beginning to ask themselves this question: Is the Federal Reserve a competent central bank, or a terminally compromised regulator that simply does the bidding of Wall Street’s mega banks to the peril of average Americans and the U.S. economy?”

“The very low interest actually exacerbated inequality.”

…when interest was very low, the rich man would go to the bank and say, I'll take your low interest. And he would use the money to make money from it. So he would enhance his fortune, whereas the poor man would go to the bank and the bank would tell him to scarper1 and say that they weren't going to lend him the money even at low low interest. And that's exactly what happened. You know, after the global financial crisis, as you know, interest rates were taken to zero by the Federal Reserve.

Those with good connections, Wall Street, the private equity guys and the like, were able to borrow very cheaply and enhance their own fortunes. And so you find, you know, mid last decade that you know that if you look at the the ranks of the top earners on Wall Street, they're almost all private equity guys. Whereas the poor, the poor people were dubbed, you know, subprime and they're, the rates of interest were actually raised after global financial crisis in order the banks didn't suffer further credit losses. So as I argue in the book, the very low interest actually exacerbated inequality.

“The results indicate that monetary tightening strongly decreases the share of national income held by the top one percent and vice versa for a monetary expansion, irrespective of the position of the economy.”

This paper examines the distributional effects of monetary policy in 12 OECD economies between 1920 and 2016….The results indicate that monetary tightening strongly decreases the share of national income held by the top one percent and vice versa for a monetary expansion, irrespective of the position of the economy…Our findings also suggest that the effect of monetary policy on top income shares is likely to be channeled via real asset returns.

“Since rich people are the only ones who have sufficient collateral to borrow massive amounts of cheap money, their first access to the money printer allows them to buy and bid up assets in a virtuous cycle.”

(That Tom Owens link is an excellent book review of Chancellor’s The Price of Time. Highly recommended.)

So the Federal Reserve owned ZERO mortgage-backed securities in 2008. Today they have monetized $2.6 Trillion. If you look at the chart below, what jumps out at me is the massive surge in mortgage originations during 2020, 2021 and 2022, overwhelmingly to people with 760+ credit scores, unlike prior periods.

The Federal Reserve itself says, “A high level of income–credit score correlation would suggest that most of the variabilities of consumer credit risks are income related, and income can serve as a reasonable approximation for credit scores.”

The Fed’s MBS buying overwhelmingly benefited the wealthiest Americans.

QE "1, 2 and 3 really did not lift the economy. The academic studies show that. The Fed won't accept that, but to me, the nasty aspect of the quantitative easing is that as it came in, it exacerbated the income and wealth divides." - Lacy Hunt

Hey, whaddya know? Bond-market’s most deeply inverted gauge is pointing to ‘large slowdown in economic growth’ and ‘deep recession’

Eurozone “core” CPI reaches 5.7%, “the highest level since records began in 2001.”

EZ “Headline” CPI was only 6.9% though, so all is well. The EZ policy rate is 3.5%.

Meanwhile, the “cost of food In the Euro Area increased 17.30 percent in February of 2023 over the same month in the previous year.”

Friends of the show Marc Cohodes’ and Porter Collins’ recent ‘Spaces’ Podcast with Robert Hanson, Former S.E.C. Branch Chief of Enforcement (Fast forward to 11 minutes in. These “Spaces” are often very glitchy.) The S.E.C. sounds pretty ineffective against big, protected guys like Elon.

If you’re pressed for time, I’d instead check out Cohodes’ recent tour de force, The Stock Market Is Not A Game.

Speaking of Porter Collins, here he is with Michael Gayed. I agree with his comment on how good “The Big Short” movie was - I was surprised how accurate it was allowed to be. Also points for calling out “the glass jaw crowd,” (e.g., Barry Sternlicht), for saying Alan Greenspan should go down as the worst Fed Chair ever, and for stating the fact that the Fed has no credibility, especially on bank regulation.

“What’s happened is, instead of the banks being nationalized, the Treasury has been privatized.” - Michael Hudson

My Dotcom-Bubble mentor, Bill Fleckenstein: The Bond Market Is Taking Away The Fed's Printing Press

It’s amazing that the brick and mortar (and shareholders) at Goldman Sachs - to give just one example - are involved in so many nefarious activities on an ongoing basis, yet no human in the C-Suite ever seems to go to jail.

Janet Yellen is fifth in line to the U.S. Presidency.

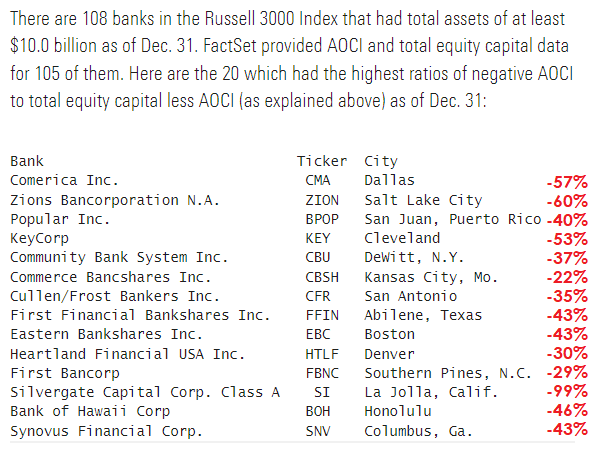

There was a March 10 Marketwatch article titled: 20 banks that are sitting on huge potential securities losses—as was SVB

I checked these banks’ current (4/6/23) prices and compared them to their highs of the last couple years - in some cases all-time highs - many of which were reached in early 2022.

No position in any of these.

I’m reminded of this great piece: What I've Learned the Past Decade by PdxSag:

“I underestimated perfidy of the financial elite”

Apartment-Building Sales Drop 74%, the Most in 14 Years

“Sales have plummeted because the math for buying an apartment building makes a lot less sense now.”

When rents were growing at blistering speed, “it was OK to be less discerning in your operations”

“Nobody wants to take a loss when they don’t have to”

“We’re in the very early stages”

The net operating income of New York's rent-stabilized buildings dropped by nearly 14% between 2016 and 2021, according to the city’s Rent Guidelines Board as the double-whammy impact of rent regulations and the pandemic weighed heavily on landlords.

Which is why U.S. taxpayers are stuck with $11 billion of this junk just from the Signature Bank collapse.

Bullard laid out a system where every American would be tested every day and would wear a badge with their negative result, similar to the ones people wear after they vote.

"I think I'm 19 out of 20 shorting CEO's who wear a wig." - Marc Cohodes

From the New York Fed:

No delinquency problem, so far…

“The world is not driven by greed. It’s driven by envy.”

One less visible risk is the damage to CRE multifamily landlords by government's rent stabilization and rent forbearance burdens. For those who have seen this before, the result will be deterioration of the properties when maintenance gets squeezed out when income drops. NYC and some CA cities come to mind, there are probably more. Deterioration in most cities going forward looks baked in

"...the very low interest actually exacerbated inequality." Known intuitively by any high school student and incomprehensible to every econ PhD at the Fed and every politician in D.C.

"...income can serve as a reasonable approximation for credit scores.” Unless you're a too TBTF or Central bank.

This "forecast" person you keep referring to should be fired...