"The interest rate will not foreclose on you, the maturity will"

"Politicians don't think there's any consequence to any amount of irresponsibility"

“I start from the premise that what the Federal Reserve does really matters, and unfortunately we have an organization that is essentially incompetent running monetary policy.”

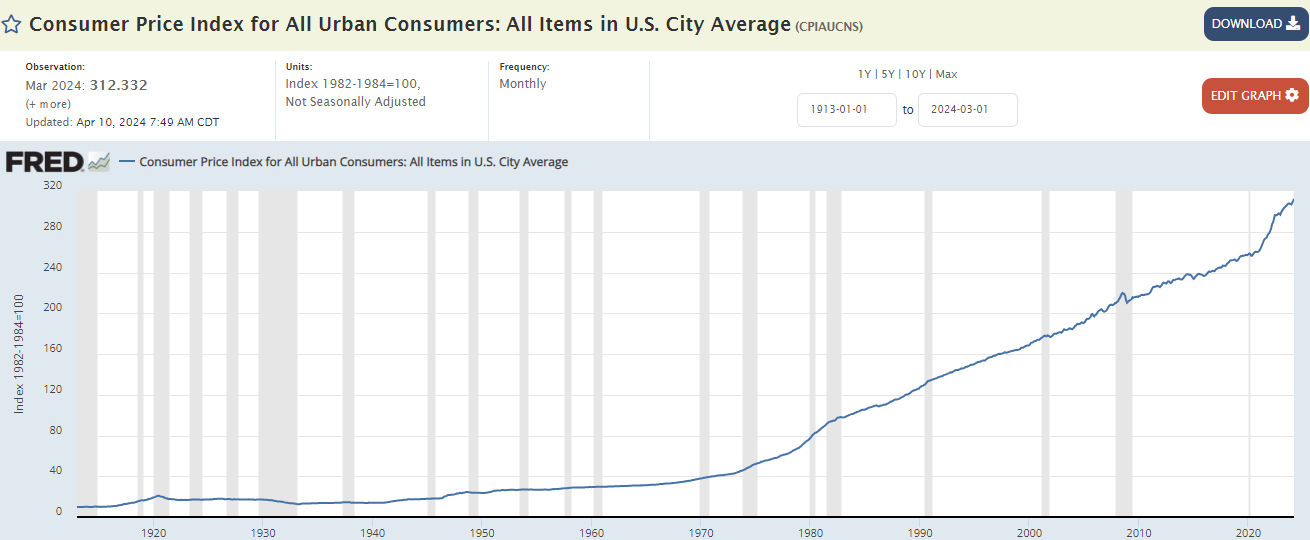

The BLS CPI model has now been above the Fed’s made-up "2% target" for 3 years. The Fed’s legal mandate is “stable prices." This is an extremely regressive tax on 330 million Americans.

Number Go Up!

“The number one thing I think is most most important for society right now is killing inflation. While I am sympathetic, and don't want to see anyone feel pain...I'd take the pain of the recession over inflation, so that's the number one thing.”

"We can never recapture the purchasing power of the dollar that has been lost.”

William McChesney Martin, longest-serving Fed chairman, in August 1955

I have some good excerpts this week (in my opinion, and I’m biased) from the likes of Tom Hoenig, David Hunter, multifamily vets Brian Burke and Charlie Young, Paulo Macro, Porter Collins, Andy Schechtman, Bill Fleckenstein, and other luminaries, plus excerpts from the 1935 book Restless Days, by Lilo Linke, and the usual eclectica, music, and stupid photos, so consider a paid sub if you are so inclined.

I’ve had the paid subscriptions for about a year now, and with the anniversary passing had a few more unsubscribes than usual, which is fine. One step forward, 3/4 steps back. The reason for unsubscribing seems to hang around 60% “time,” and 40% “price.” (Not sure how many are too polite to say, “Total Garbage.”)

Time: As I’ve said before, my format here is generally a buffet, not a 7-course meal you have to consume in order. I have written missives similar to these for over 20 years, and still refer to them for historical items1, but if the emails just stack up and you never read them, I understand. As for price, it is what it is. I put a lot into these things.

I’ve noticed a number of popular Substacks lately are offering “50% off” sales and things like that, so perhaps their paid subs are down. I haven’t done the discount thing, but I understand that times are tough for many. I’d rather have fewer paid subs and less noise in the comments (which I always read). I only want happy people here, and appreciate those who get something out of these posts!

To unsubscribe (paid or not), when you’re on one of my posts, go to the top right, and click the avatar (yours probably won’t look like mine):

You’ll see a screen like this below. Go to “Manage Subscription” at the bottom:

Then scroll down to “Account Actions”, and click whatever the issue is:

Simple!

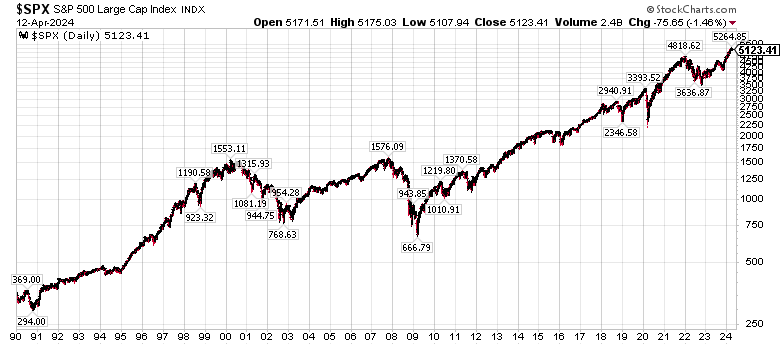

Tragic Week in the Markets Hope everyone survived the carnage.

It’s one chicken wing, Michael. How much could it cost? $99.83?

Gold

Some have noticed that gold is at record nominal highs, or, as I put it:

I heard Guy Adami say that "in 2022, global central banks bought approximately 1131 tons worth of gold for roughly $71 billion,” which sounds like a lot until you realize that’s only about 2.5 weeks of Fed QE, or roughly the market cap of Colgate-Palmolive.

I don’t consider gold an investment, I consider it a currency, the best currency (Bitcoin people - please forgive me here). As a conspiracy realist, I believe the central banks HATE to see gold doing what it’s doing, because it’s really a report card on their incompetence. While I can’t prove anything (until I’m dictator,) I have no doubt the the global central banks and their allies have powerful ways to manipulate gold prices - at least for a while. Lately, not so much.

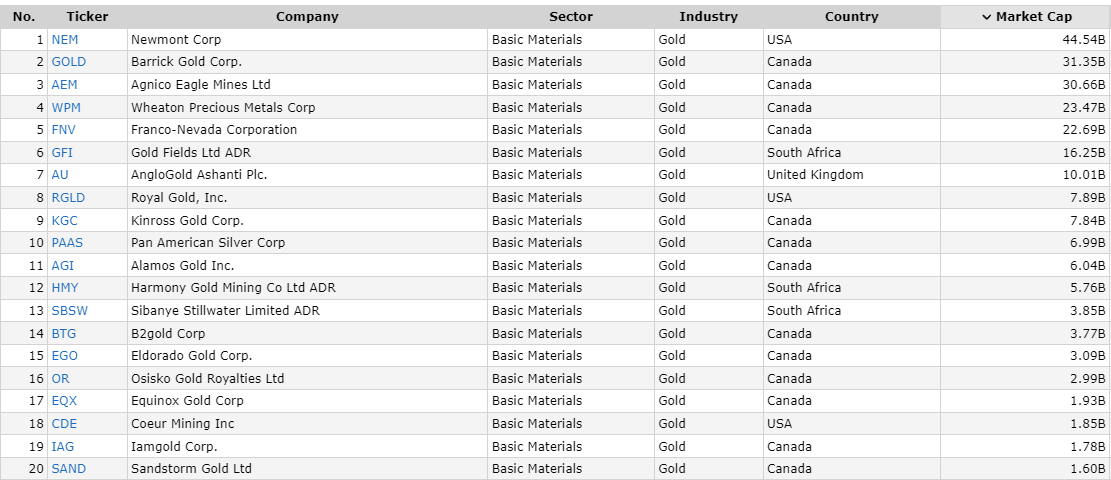

Most Americans don’t own gold, and institutionally, gold’s a rounding error. Take the top 20 gold-related companies by market cap, according to Finviz:

The market caps of all of these twenty combined is about $235 billion, about the same as PepsiCo, or two months of Fed QE. Any move into gold stocks would have a massive influence on prices. Will that happen? Who knows.

For example, I have made some money over the years dating - but not marrying! - a silver stock called First Majestic (AG). It’s run up 80% just since February, as silver itself has risen only about 28%. Yet the last time silver was this high ($28.25), AG was close to $20, instead of $7.52. I haven’t owned any AG for a long time so I missed this latest move. Miners like this can move, but you can’t overstay your welcome or you will get crushed.

Zerohedge was floating this 17-year chart around - it’s gold versus the inverted 10-year Treasury “Real Rate.” They usually move in lockstep. My first reaction is that maybe in 2022 gold began to realize that the “real rate” is nonsense.

I realize this is a non-consensus view, but I think CPI, PCE, and all the other ex-this and sticky-that models have no relation to the basket of goods approach that most non-billionaire, non-PhD Americans take.

The constant, pervasive gaslighting - e.g., goofballs like Greg Ip writing, “It’s you, not the data!” - really ticks off normal Americans (and registered WSJ readers).

For every reply I get on Twitter from some econ sophomore saying, “You know, the BLS numbers are calculated properly,” I get 1,000 people agreeing with me on inflation (i.e., the cost of living.) As I say, I’m not the one having to turn off replies (unlike, say, Paul Krugman, or Claudia Sahm, who lately seems to have folded up her tent and gone home in tears.)

"There is no way there is truth in seasonal adjustments."

You cannot trust the CPI, PCE, PPI or other numbers.

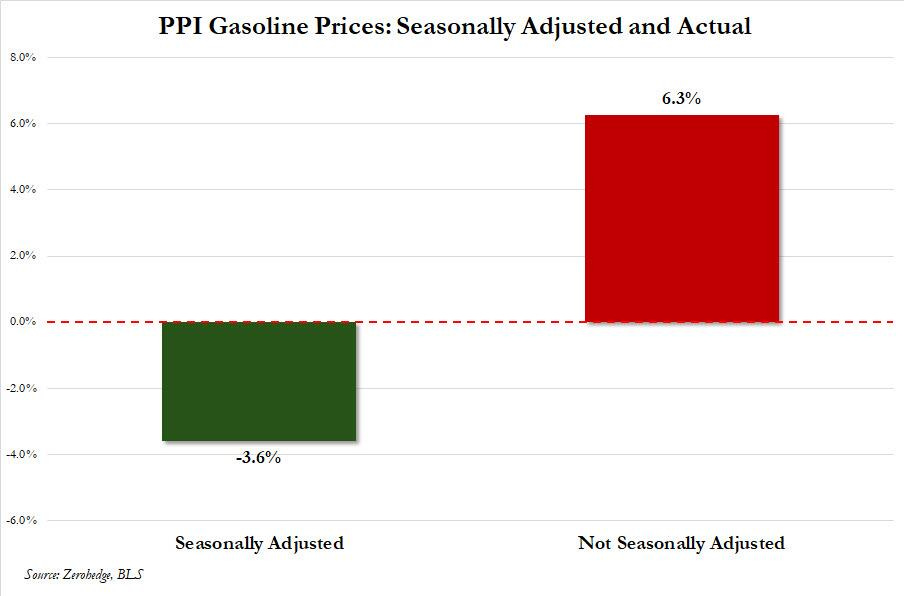

“according to the BLS, the seasonally-adjusted gas price in March magically dropped by 3.6% even though the unadjusted, as in real, gas price rose by 6.3%, exactly what the AAA also reported in its daily summary of what gas prices across the US truly are.”

“Anyone who is a data-nerd in here, and you care deeply about truth, I would throw all of your seasonal-adjusted data out the window, and do the work yourself for the truth.” - Neely Tamminga

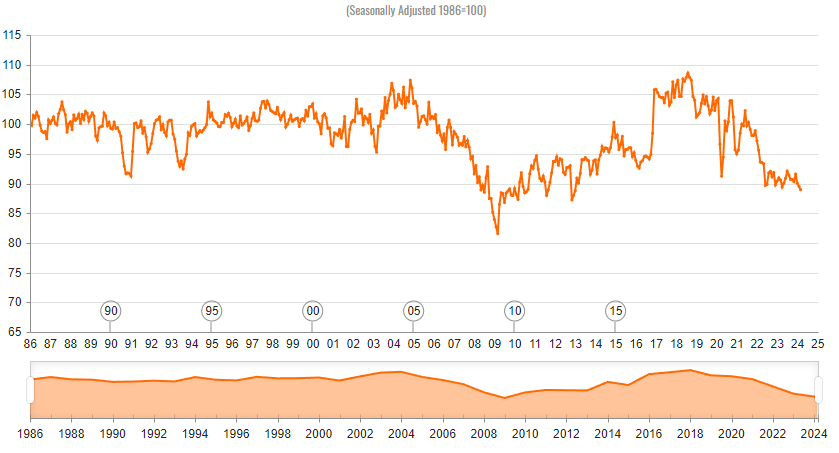

NFIB Small Business Optimism Reaches Lowest Level Since 2012 “This is the 27th consecutive month below the 50-year average of 98.”

CREDIT MARKETS

“Two percent of owners reported that all their borrowing needs were not satisfied, down 1 point. Twenty-seven percent reported all credit needs met (up 3 points) and 59 percent said they were not interested in a loan (down 2 points). A net 8 percent reported their last loan was harder to get than in previous attempts (up 1 point). Four percent reported that financing was their top business problem (unchanged). A net 17 percent of owners reported paying a higher rate on their most recent loan, up 1 point from February. The average rate paid on short maturity loans was 9.8 percent, up by 1.1 points from last month. Twenty-eight percent of all owners reported borrowing on a regular basis, up 3 points from the previous month.”

Doesn’t sound like “high rates” are a major concern.

As for inflation…

"...continued stress in navigating inflation pressures leads as the top business problem. Inflation continues to frustrate owners as a significant share of them still report it as their biggest problem in operating their business."

Meanwhile…

“Everybody is distracted by new highs in the stock market, the presidential election, and wars in Ukraine and Israel. But credit markets are sending signals that the fabric of the overleveraged American economy is under serious strain. Keep your eye on the ball.”

(I actually forgot where I got this quote from. If anyone knows, let me know!)

From friend of the show Paul M…

via Grant’s:

“Behold, the incredible vanishing stock market. Net share issuance from MSCI All Country World Index components stands at minus $120 billion in the year-to-date, relays the Financial Times, citing data from JPMorgan. That figure, which compares to a $40 billion downtick in 2023 and stands to mark the largest such drop since at least 1999, contrasts with JPMorgan’s November prediction of $360 billion in net new supply for 2024.”

“The $2.5 trillion, 13,000 token cryptocurrency category is primed for M&A, Alex Dreyfus, CEO of blockchain firm Chiliz told CoinDesk, arguing that “there are already too many tokens and too many ‘projects,’ for not enough adoption and utility.”

“Get your unicorns in a can: qualified investors can now access the late-stage venture capital universe in one fell swoop, as Tuesday marked the launch of the Forge Accuidity Private Market Index, a collection of 60 of the most liquid privately held firms. The market cap-weighted gauge, which features Elon Musk’s SpaceX as its top holding with a 6.41% allocation, is accessible to those with a net worth of at least $5 million and includes a minimum outlay of $250,000.“

“Seventy-nine S&P 500 members have issued negative guidance as of Friday by FactSet’s count, a tally topped only once since 2006 and well above the 5- and 10-year quarterly averages of 58 and 62, respectively.”

Good news, Bad news, with David Hunter

“I think this move probably takes us to S&P 7000”

“We'll probably be rolling over sometime in the second half of this year, and as you know I'm looking for 80% downside in a bear market that follows the melt-up.”

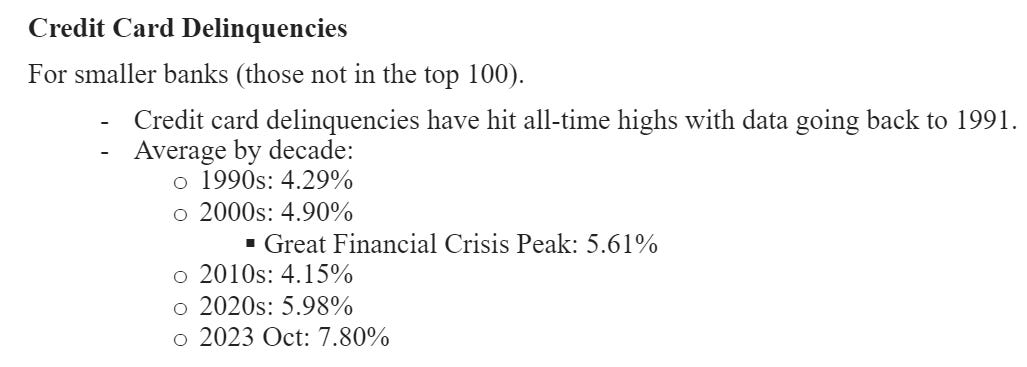

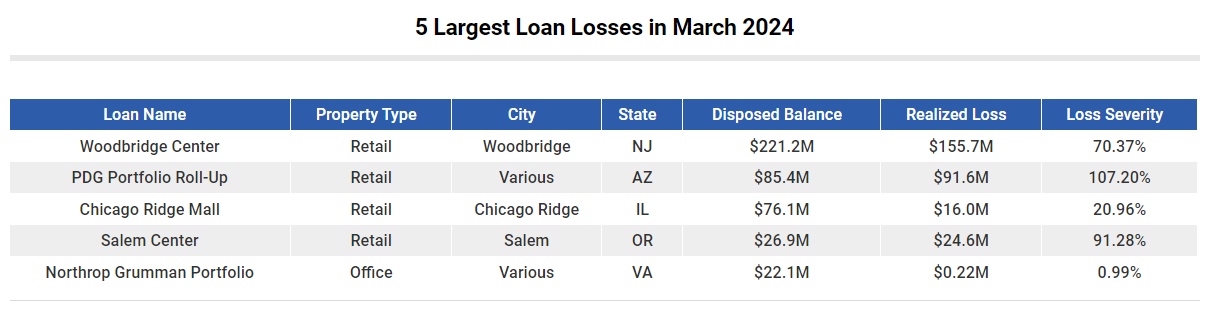

The loss severities continue to impress:

State Farm targets wealthy areas of LA for policy non-renewals “In Brentwood’s 90049, State Farm won’t renew policies for 61.5 percent of its 2,114 policyholders…In Bel-Air’s 90077, the non-renewed policies rise to 67.4 percent, with Pacific Palisades’ 90272 hitting 69.4 percent, or 1,626 policyholders. In Beverly Hills’ 90210, 46.1 percent of policyholders won’t be renewed, comparable to 46.9 percent of Malibu’s 90265.”

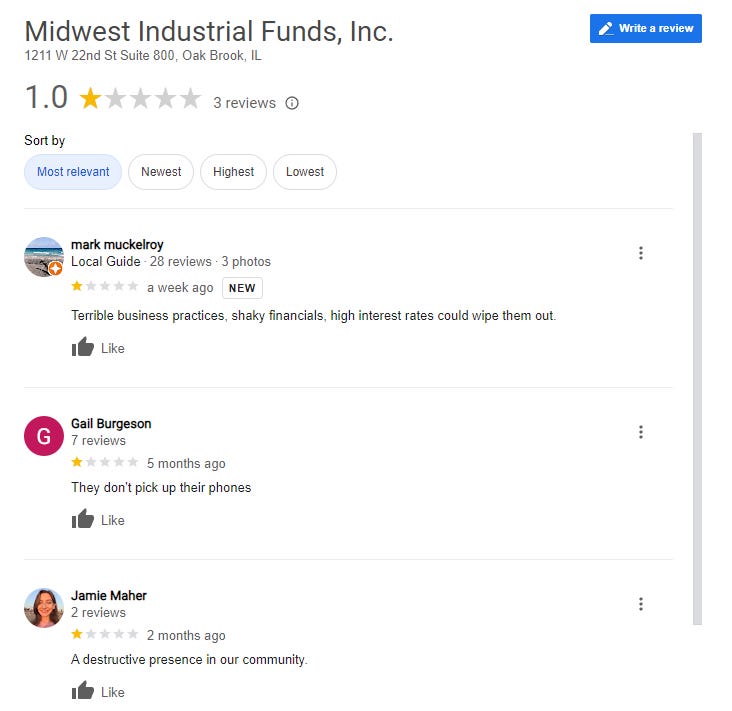

Midwest Industrial Funds moves massive Geneva project forward “Midwest Industrial Funds’ petition to annex 225 acres for development of an industrial complex is moving forward…Oak Brook-based Midwest Industrial Funds aims to rezone the site from rural residential to light industrial use…Community members were irked when the firm removed about 75 burr oak trees, some of which were estimated to be 300 years old. Despite opposition from nature advocates, the area where the trees once stood is designated for one of the warehouses within the planned development.”

I checked their Google Reviews:

Multifamily Mastery: Brian Burke on Surviving Market Cycles

“You don't want to be painted into a corner, and bridge debt is exactly that, you're painting yourself into a corner. You're saying, okay, we're gonna improve this property within the first three years, then we're going to refinance out, but if something happens in that three-year period, there is zero time for the market to recover and come back. There's zero time for you to come up with other plans, or other options. That is where the primary risk is. The primary risk isn't the interest rate, the primary risk is the maturity. The interest rate will not foreclose on you, the maturity will.”

Host: “Yeah, that's that's well said. So let me ask you another question: how many syndicators right now would you estimate are in technical default of their loan covenants, either the DSCR less than 1.25, or LTV greater than 80%, even if the property's performing on occupancy and net operating income? And would a lender foreclose on a deal like that? Are more loans going to be modified or worked out behind the scenes?”

“So I think that's a difficult question to answer because I don't have data, but I'll tell you anecdotally what what I think is happening. I think that any sponsor that bought a property from, let's say, 2020 to 2022, anytime in that period to the end of, say, mid-2020 to the end of 2022, any property bought during that period that was bought with bridge financing at the time greater than 75% LTV is probably fits into that category as you describe. Their rate has gone up dramatically, their maturity is approaching, their rent growth went away, their rate cap replacement cost skyrocketed, if they have a rate cap at all.”

“Everybody wants me to say, oh yeah, the market's going to come back, everything's going to be great, it's going to be a great time to buy real estate, but I can't say that. Let's be real. No, I cannot make a case for investing right now.”

Charlie Young

“I was in New York City two weeks ago, having meetings ,and they're just puckered up, and their underwriting is just not reality, so we'll keep working it all, and we'll just see where it lands

Host: Do you have a sense of when that's going to change?

I'm going to guess like everybody else, so the Fed's going to have to give them some clear direction. One of the things that they need - they need discovery of pricing, and there is no discovery of pricing out there. They need to know what what prices and cap rates are, of which there just have not been any. They need stability in the 10-year, and all of that probably hinges off of what and when the FED decides to provide some clarity for them. We started December, where everybody thought that the Fed was going to cut in March, and then the prints came out hot in January and February [and March]. That got moved back to June, July, and you know it's all over the map, so when things are all over the map, those people have no interest in engaging, but they have an awful lot of dry powder sitting on the on the sidelines ready to go.”

“I was with with a lender in New York when I made my trip up there, and just talking it through, and they do not think they have a problem, and they do have a problem. They don't totally realize they've got a problem, so they're not ready to write things down. They're not ready to be creative about it for the most part. I've heard a handful of stories of people that are getting some creative opportunities, but as a general rule, that's another reason I was going, okay, if we go to the end of the year before they cut rates, some some of those zombies you're talking about will just have to fall down and hopefully create some opportunity.”

Tom Hoenig

“If you look at this Consumer Price Index, since June, since they stopped raising rates, it has not fallen really much below 3%, and core has been clearly 3%, so why are they talking about cutting rates?”

Taggart: “You talked about removing the dollar from the gold standard, kind of removing the discipline, you know, the brake on the system, so obviously since then all that's happened is is the purchasing power of the dollar has declined even faster. The dollar is doing better than most other fiat currencies, right? I mean, are we just staring at the end game here, and it's just going to continue to play out like this, or is there potential for something else?”

Hoenig: “Well, unless we change our ways, we will continue to to devalue the dollar and its purchasing power. I tell people yes - you know they saying, well, on the international level the dollar is strong - and I say yes. If you're grading on the curve - which we are with currencies, because they're all fiat currencies - we're still getting good grades in terms of the relative value, but if you grade on the absolutes, we're getting an F because the value - when you look at the Consumer Price Index, it's really striking. Decades of stable prices until after World War II, until after 1971, when we went off the gold standard.”

If you’ve never read it, this article is a great introduction to Thomas Hoenig: The Fed’s Doomsday Prophet Has a Dire Warning About Where We’re Headed

Restless Days

I briefly mentioned the obscure 1935 book, Restless Days: A German Girl's Autobiography by Lilo Linke in my post A Very Ordinary Life. Since I couldn’t find the book online, I recently bought a first-edition copy, as I sometimes do (unless the books are hundreds of dollars or more, as some of the old ones are.)

These opening passages in the chapter titled “Inflation” are sobering:

“The time for my first excursions into life was badly chosen. Rapidly Germany was precipitated into the inflation, thousands, millions, milliards of marks whirled about, making heads swim in confusion. War, revolution, and the wild years after had deprived everyone of old standards and the possibility of planning a normal life. Again and again fate hurled the helpless individual into the boiling kettle of a wicked witch. Now the inflation came and destroyed the last vestige of steadiness. Hurriedly one had to make use of the moment and could not consider the following day.

The whole population had suddenly turned into maniacs. Everyone was buying, selling, speculating, bargaining, and dollar, dollar, dollar was the magic word which dominated every conversation, every newspaper, every poster in Germany. Nobody understood what was happening. There seemed to be no sense, no rules in the mad game, but one had to take part in it if one did not want to be trampled underfoot at once. Only a few people were able to carry through to the end and gain by the inflation. The majority lost everything and broke down, impoverished and bewildered.

The middle class was hurt more than any other, the savings of a lifetime and their small fortunes melted into a few coppers. They had to sell their most precious belongings for ten milliard inflated marks to buy a bit of food, or an absolutely necessary coat, and their pride and dignity were bleeding out of many wounds. Bitterness remained for ever in their hearts. Full of hatred, they accused the international financiers, the Jews and Socialists—their old enemies—of having exploited their distress. They never forgot and never forgave and were the first to lend a willing ear to Hitler’s fervent preaching.

In the shop, notices announced that we should receive our salaries in weekly parts. After a while, we queued up at the cashier's desk every evening, and before long we were paid twice daily and ran out during the lunch hour to buy a few things, because as soon as the new rate of exchange became known in the early afternoon our money had again lost half its value.

In the beginning I did not concern myself much with these happenings. They merely added to the excitement of my new life, which was all that mattered to me. Living in the east of Berlin and in hard times, I was long accustomed to seeing people around me in hunger, distress, and poverty. My mother was always lamenting that it was impossible for her to make both ends meet, my father—whenever he was at home—always asking what the deuce she had done with all the money he had given her yesterday. A few tears, a few outbreaks more did not make a difference great enough to impress me deeply.

Yet, in the long run, the evil influence of the inflation, financially as well as morally, penetrated even to me. Berlin had become the centre of international profiteers and noisy new rich. For a few dollars they could buy the whole town, drinks and women, horses and houses, virtue and vice, and they made free use of these possibilities.”

"just because you're living in a bubble doesn't mean that EVERYBODY is living in that bubble"

Paulo Macro

"The fact that there's zero political appetite in America to even discuss deficits is a feeling that Brazilians know very well."

“I guess I would put it this way - forward guidance, and all of these guys with their verbal diarrhea out of the FOMC - I mean there were like four of them talking yesterday, three the day before - it's so much noise it stops actually having signal at all, because you know that they're going to do the politically expedient thing”

“we're speaking Portuguese here in America without even realizing it yet”

“the most motivated buyer is…the short seller who's over his skis, and now the stock's starting to move against him in a vacuum”

“We've always known that the short-termism of the election cycle, and the advent of the career politician who doesn't go home to grow his own crops, or run his own business - he is in the business of trafficking in the currency of power and making a living at that over the decades.”

Porter Collins

“You can see that the spending is outpacing the federal tax revenue by about $2 trillion, and every time I click on there it just mind-numbing to me, and so we're running a 7% budget deficit and it's debt monetization. That's what's going on, right?”

“You know I love Steve [Eisman], our former boss, but he's now a long-only guy, and he's like, I don't worry about it [inflation]. Listen - he'll worry about it when it's a problem - but he's in stocks, and stocks are going up right now. I think stocks are inflating against the dollar too. Look at the P/E multiples. For whatever reason, the P/E multiples have exploded over the past 15 years.”

Andy Schechtman

“I look at gold and silver not as an investment. Gold and silver are wealth, not investments. I think it's important to say that at the beginning of this conversation for your people who are listening, because to me it's wealth that has outlived two world wars, German hyperinflation, the Great Depression, every pandemic, and anything that's ever been thrown at it, and so to me, what gold and silver is just pure and simple wealth.”

Mr. UNTERMYER. But the basis of banking is credit, is it not ?

Mr. MORGAN. Not always. That is an evidence of banking, but it is not the money itself . Money is gold, and nothing else.

Mr. UNTERMYER. Do you not know that the basis of banking all over the world is credit rather than gold?

Mr. MORGAN. It is the basis of credit, but it is not the basis of money.

The way I phrase it is: Gold is a handgun you keep in a drawer and hope you never need.

“A couple of things that I would say as you look at gold that really resonate with me - number one, in 2019 the most well funded, well-informed, and sophisticated and powerful bank on the planet, the Bank for International Settlements, which is really viewed as the central banks’ central bank, reclassified gold as the world's only other tier one reserve asset. Now that that's very important to me, because when you realize that really over the last six or seven years we've seen the central banks of the world - who I would say are not only the most well-funded, but more importantly the most well-informed traders on the planet - have not only gone on a repatriation spree, they’re repatriating all of their gold holdings both from the New York Fed and the Bank of England.

They’re also on a purchasing spree to where over the last three years in particular the most well-informed traders on the planet have accumulated more gold than at any time in the last 100 years. I think the most important thing when we talk about gold is that it is important enough to be reclassified the only other tier one reserve asset other than treasuries, and important enough to be accumulated by the central banks at a level we've never seen before.”

“Money is, I repeat, in its literal sense, a confidence trick. The first duty of a central bank is therefore to maintain people's absolute confidence in its integrity. (For me that implies that no bank with a fiduciary mandate should be burdened like the Fed, or in effect the Bank of England, with a political one too such as safeguarding employment or stimulating economic activity.)

Last, wilful inflation of the money supply, call it what you will (QE, deficit financing, liberal credit policy, printing money), is the creeping repudiation of debt. It is dispossession by stealth. Keynes called it an unfair tax. Worse, and most dangerously, it is the betrayal of trust.”

Bill Fleckenstein

“We had a tremendous opportunity after the 2008 banking crisis, brought on by the real estate bubble - I hate when people call it the “great financial crisis”2 or whatever. That's a trite name. That's just crap. You’ve got to call it what it is so you understand what happened. The financial system came about an inch away from being vaporized and people were scared, and in that moment, had we had a real leader, we possibly could have made the tough decisions. I had hoped that would happen. Barack Obama was pathetic when it came to anything finance-related - not not that any of the rest of these guys have been any better - but that was a moment where they could have done some sound things, and put us on a firmer footing, and they didn't, and it's only gotten worse, and now these politicians don't think there's any consequence to any amount of irresponsibility.

I mean you have to ask yourself, how big is the crisis going to have to be to force them to try to deal with this, and I would say it has got to be really big. You can't look at anything about the finances of this country and feel confident at all. There's going to have to be some kind of a train wreck. We will get it - I don't know what it will be - and in that moment, if we have the right leader, perhaps we will settle up. Otherwise it'll be a lot of inflation for a really long time, so I don't know how it's going to play out. We'll have to see how events go, but it's a real problem, and the setup is not constructive at all.”

This incredibly prescient article was written in May 2008 by Pam Martens, one of the people behind the must-read WallStreetOnParade website:

The Wall Street plan for the Obama-bubble presidency is that of the cleanup crew for the housing bubble: sweep all the corruption and losses, would-be indictments, perp walks and prosecutions under the rug and get on with an unprecedented taxpayer bailout of Wall Street. (The corporate law firms have piled on to funding the plan because most were up to their eyeballs in writing prospectuses or providing legal opinions for what has turned out to be bogus AAA securities. Lawsuits naming the Wall Street firms will, no doubt, shortly begin adding the law firms that rendered the legal guidance to issue the securities.) Who better to sell this agenda to the millions of duped mortgage holders and foreclosed homeowners in minority communities across America than our first, beloved, black president of hope and change?

"The terminal value for foreigners' investments in China is zero." - Russell ‘Buzzkill’ Napier

To search these posts, in Google use site:rudy.substack.com [keyword(s)]

I call it “Great Depression II,” because for half of America I think that’s what it’s been.

Just wanted to say I’m a happy paying subscriber. Keep up the great work!

This is one of my favorite weekly reads. You do a great job of grabbing bits and pieces from all over, many from people I already follow, and it helps me work toward getting the bigger picture sorted out--as best I can anyway. I've been "cleaning up" my subscriptions (it's getting out of hand!), but for yours I just switched from monthly to yearly. Keep up the good work!