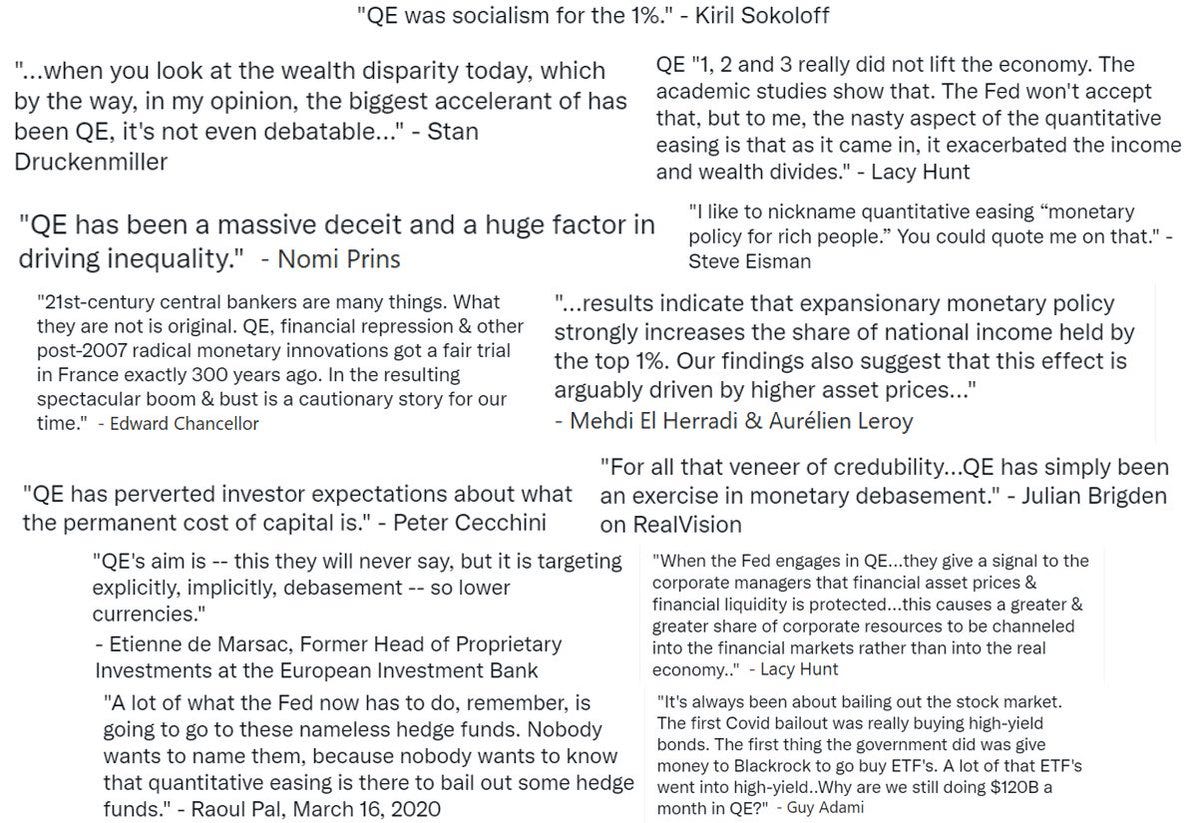

Monetary policy for rich people.

“A clear and explicit return to QE policies” is coming.

Our isolation from the bulk of the country left us with a narrow view of the world. We valued what we could measure, and that meant material wealth. Things that couldn’t be measured—community, dignity, faith, happiness—were largely ignored…

Who had I become? Just another shark in a suit?

- Jerry Maguire

It is difficult to get a man to understand something,

when his salary depends upon his not understanding it!

Upton Sinclair,

I, Candidate for Governor: And How I Got Licked, 1934

There was a good recent podcast with Michael Howell, “the Professor of Global Liquidity,” titled the Recent Rise of Liquidity and the Dollar's Triffin Dilemma

Trevor Hall, the host of Mining Stock Daily, and Howell discussed a variety of subjects, including the recent “de-dollarization” kerfuffle1. Both agreed that reports of the death of the dollar are exaggerated, to borrow from Mark Twain, with the Yuan “decades away” from being any sort of serious threat.

Howell is a perspicuous2 guide to the financial system’s plumbing. There are a number of “financial plumbing experts” making the podcast rounds who describe the same system in various ways, so I’m not singling out Howell here. He clearly knows his field well.

One thing that has aided me immensely in navigating markets over the years is that I don’t come from Wall Street, have no PhD in economics, and have had he ability and desire to approach our financial system without having to first unlearn everything I’ve been taught.

There’s a wonderful quote from the movie Sicario:

“You're asking me how a watch works. For now we'll just keep an eye on the time.”

I just try to keep an eye on the time.

To start off, Howell explains a process of “stealth easing” that he believes has been happening, with the Fed injecting “a half trillion dollars into the financial system since Silicon Valley Bank.” The stock market lately seems to agree with him.

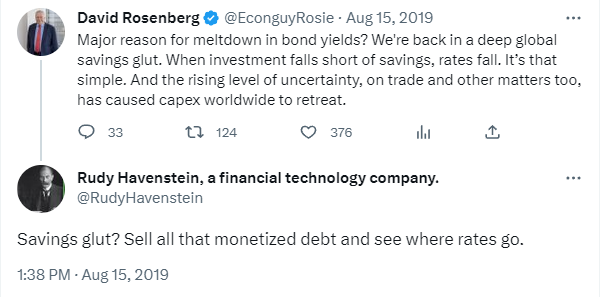

So much for QT, which I have since 2017 rightly mocked as a joke. Howell says that the powers that be will not allow a “banking crisis at any cost,” and sees liquidity significantly increasing over the next six months. He mentions that deficits will (apparently inevitably) grow, and the question is then asked: who is going to buy all these new bonds, investors, or the Federal Reserve?

JULIA LAROCHE: You have to kind of wonder, like, who wants to own government treasuries right now?

JEFFREY GUNDLACH: The Fed. The Fed is the one that wants to own them.

“A clear and explicit return to QE policies” is coming, is the answer.

“You simply have to have central banks buy this debt because no one else is going to buy it.”

“The financial system cannot handle higher interest rates…the only solution is really for the Federal Reserve to start to monetize - in other words, purchase more and more debt. Now if you’re gonna start monetizing, in other words, creating monetary inflation, number one, there is a risk of a return to High Street inflation. It’s not necessarily the case, we’ve seen lots of example in the last 20 or 30 years of increased monetary inflation without causing High Street Inflation. Monetary inflation is much more obvious in the asset markets [e.g. housing - RH], where it comes through directly and it only comes through indirectly on the High Street, because you’ve got other factors, such as falling costs, and we’ve benefited for much of the past two decades from low costs from importing cheap goods from China. Now if you look forward, we may not have that luxury of cheap Chinese goods, but High Street inflation is a greater risk - but above all that, monetary inflation is likely to come back, and, if you’re gonna get monetary inflation, what you absolutely must have in portfolios is monetary inflation hedges. The two most obvious monetary inflation hedges are gold and Bitcoin, but then I’d say more generally if you look at the experience of the past 20, 30, 40, 50 years, residential real estate ain’t bad either.” [Just ask Tom Barrack - RH]

(Perhaps the Americans who’ve had their jobs shipped overseas in recent decades would not consider cheap Chinese goods a “luxury,” but I digress.)

“...if you can depreciate a currency what you’re really lowering is the price of labor."

"Of course, there was always inflation. There's no such thing as no inflation. It's just lower inflation than what they want. We always have inflation, inflation is not transitory, it always goes up. It's just the rate of change that we're debating here."

Peter Boockvar on Realvision

And again, I protest the very common canard that “we did not have inflation” prior to 2021. CNBC hosts used to say that every day. It’s the “big lie” of the 2010’s, the type of cluelessness only someone with an econ PhD or a very close symbiotic attachment to financial markets would have.

We absolutely had inflation, it was just either understated by the goofy CPI (e.g., car prices didn’t go up for 25 years), or was simply, as Harley Bassman points out, not measured.

I’ve also tried to highlight over the years that the very common claim that QE was merely some sort of meaningless “asset swap,” hardly worth mentioning, was, pardon my French, horsesh*t. One of the best at explaining how this worked in the real world was real estate investor Nick Halaris, who I’ve written about several times, including here.

Or just ask some people with actual skin in the game in the markets about QE:

Mr. HENSARLING. Will the Federal Reserve monetize this debt?

Mr. BERNANKE. The Federal Reserve will not monetize the debt.

Citadel Senior Advisor Ben Bernanke, October 1, 2012

A related question I sometimes hear--which bears also on the relationship between monetary and fiscal policy, is this: By buying securities, are you "monetizing the debt"--printing money for the government to use--and will that inevitably lead to higher inflation? No, that's not what is happening, and that will not happen. Monetizing the debt means using money creation as a permanent source of financing for government spending. In contrast, we are acquiring Treasury securities on the open market and only on a temporary basis, with the goal of supporting the economic recovery through lower interest rates. At the appropriate time, the Federal Reserve will gradually sell these securities or let them mature, as needed, to return its balance sheet to a more normal size.

I love Howell’s use of the word I use - monetizing - since many avoid it. I do quibble with Howell’s claim that the Fed will have to “start to monetize.”

Using Bernanke’s definition - Monetizing the debt means using money creation as a permanent source of financing for government spending - The Federal Reserve has been monetizing Federal debt for years.

As far as the Fed returning “its balance sheet to a more normal size,” come on - who are they kidding? I refer again back to Pimco Senior Advisor Ben Bernanke’s testimony of March 25, 2010:

Congressman Ron Paul: As we talk about this, I think most people assume that they're waiting for a signal from you when the balance sheet might shrink. But even in the Depression, when it shrunk 16 percent, it wasn't done purposely; it was the way the system was working back then. Can you give me a rather quick answer on this? Do you have any idea what percentage the base should shrink or might shrink, or is that something that you don't even want to address?

Mr. Bernanke. No. I think we would like to bring the balance sheet back to something consistent with where it was before the crisis, which means enough to accommodate Americans' demand for currency plus a modest amount of reserves in the banking system, and that would suggest something under a trillion dollars I think would be--

Dr. Paul. A trillion dollars?

Mr. Bernanke. Or less, yes.

Dr. Paul. Okay. Of course, that would be very unprecedented. During the crisis that Paul Volcker had to deal with from 1979 to 1982, it was considered a major problem. The inflation got out of hand at 15 percent and he had to come in and do something. And I guess the question is, how much did he have to shrink the balance sheet during those 3 years?

Mr. Bernanke. Well, not very much. He was focused on money growth in particular. So he wasn't clearly in a situation where we are now where there are these large, unused balances. I would point out that he was focused on M1 and M2 growth. M1 and M2 are not doing anything now. They're very flat. It's just the base, as you point out.

Dr. Paul. Excuse me, but the truth is, is during that time, which was considered very tight money, the monetary base was still growing, during those 3 years, the monetary base grew 31 percent. So my suggestion is, it might not be so easy to cutback, because even in the midst of an inflationary crisis like that, because maybe in 6 months or a year from now when you decide to do something, maybe there will be an increase in M1 and M2, and then it will be a different ball game when you're dealing with this.

Well, Brookings’ Distinguished Fellow Ben Bernanke - as of today - is only off about $7.6 trillion from his 2012 prediction of the Fed’s balance sheet size. A rounding error the Nobel Committee must have overlooked.

Howell calls the American banking system “rock solid,” although later says, “the Western financial system is more fragile than the Chinese,” which is more “robust” (shout out to Nassim Taleb.) Schrödinger's financial system.

Howell then talks about a shortage of high quality collateral.

Perhaps there’s merely a shortage of high quality collateral at a price a free-market would set it at?

I mean, the Federal Reserve has about $8.6 trillion of high-quality collateral on their balance sheet right now, right? Why not sell that?

Howell also describes the U.S. banking system as “very tightly regulated,” but I think the history of Federal Reserve bank regulation, both recently and in 2008, is clearly pretty abysmal.

Anyway, here’s the money quote for me from the podcast:

“Forget about the inflation remit, forget about the employment remit, it’s the integrity of the sovereign debt market, the Treasury market, that is absolutely paramount.”

Here we really cut to the chase: Screw the serfs!

A pet peeve forever as I’ve followed financial marketeers is the utter lack of concern - almost contempt - by almost everyone involved about the cost of living for 340+- million Americans.

Yes, Powell and his apparatchiks have over the past year finally started to notice, but these are the very same people who squirted trillions all over the financial system and cried for higher inflation just a couple years back. Many of the “inflation isn’t that bad” crowd - including everyone on the FOMC - own highly-levered assets - lots of them - and they benefit immensely from monetary inflation in a way most Americans do not. I understand that our financial elites - including the Fed - WANT higher inflation, even if they can’t say it out loud (although they sometimes do). My point is that this is terrible for most Americans.

Since rich people are the only ones who have sufficient collateral to borrow massive amounts of cheap money, their first access to the money printer allows them to buy and bid up assets in a virtuous cycle. Borrowing begets bidding which begets price appreciation which begets more collateral for borrowing. [Great article worth reading - rh]

i.e., The Cantillon Effect.

I’ve heard a number of financial pundits - many with nine or ten or more digits in their net worth - saying we need higher inflation for longer, as if that hasn’t been the daily experience of most Americans forever. These people should go to the neighborhood bar to opine, instead of Bloomberg.

Some are now even trying to make inflation a partisan issue - it's not. If anything, inflation - i.e., the cost of living spiking ever higher - is a class issue.

Those with assets, especially leveraged assets - should do quite well. Everyone else will not.

The economic and social costs of inflation have been enormous. Inflation is a tax that erodes the income of our workers, distorts business investment decisions, and redistributes income in favor of the rich, Americans on fixed incomes, such as the elderly, are often pushed into poverty by this cruel tax.

If we have 340 million Americans, and the vast, vast concentration of levered-wealth is held by - let’s say 10 million, no, say 20 million - then the other 320 million are cruelly exposed daily to the relentless pressure of a higher cost of living - inflation, the most regressive tax.

It doesn’t matter to Janet Yellen in the slightest what food costs - to millions of Americans it very much does. And yet I have, for decades - more so lately - heard very well off people and their publicists dismissing the cost of living as some minor annoyance, something way down on the list of priorities. The stock price of Nvidia is far more important. They love their Fed fun coupons!

Inflation is top of mind for most people though, I assure you. The stock market for half of America is as alien as a private jet.

We need to elevate the problem of a rising cost of living to a much higher priority.

There’s a reason for my nom de plume.

"The temptation now is to find another way out: to ditch the 2% inflation targets of recent decades and raise them modestly to, say, 4%. That is likely to be on the menu when the Fed begins its next strategy review in 2024."

A doubling of inflation is considered “modest.”

Finger on the pulse.

I once had a very famous hedge fund manager, who I liked - and who later blocked me - DM me to argue that the U.S. needed years of “6%” inflation (this was when official CPI was around 2%, which - if you’ve seen how oddly the CPI model is calculated - means actual real world inflation was probably already over 6% at the time).

I told him high inflation would be really bad for most people, and he was dumbfounded that I didn’t agree with him. I’ve thought this often when hearing otherwise very smart people opining on Fintwit, Substack, on podcasts etc. - I want to yell at them, and sometimes do - go say that in a supermarket!

Very few people who’ve benefited from the current system criticize it. I do. I personally have benefited, but I know those who have not.

I do not think it is good for the United States to devolve towards a system with South African levels of wealth inequality.

One of the only billionaires (besides Jeremy Grantham or Sam Zell) I’ve ever seen criticize the system is Stan Druckenmiller, in this epic clip from 2021.

“People see the risk in a temporary 20% stock market decline...But chronic serious inflation is way more disastrous. The 7% annual rise in the Consumer Price Index in the 1970s doubled the price level in just 10 years...every dollar of savings lost 50% of its purchasing power."

Steve Bregman, Horizon Kinetics

I don’t think Steve Bregman’s a billionaire, but he gets the scam.

I hear very, very often from people like Howell, people whose business lives are intricately tied to the financial system as it stands - that the number one issue is always “saving the system,” which over recent decades has become synonymous with “saving the stock market.”

I learned today about the acronym POSIWID -- the "proof of a system is what it does." Well, what exactly has our current system done?

Who exactly are we “saving” with all the QE and monetary inflation and monetization?

Here’s a sobering view - from the Federal Reserve - of how things have changed since financial war criminal Alan Greenspan took over the reigns of the American financial system in 1987:

Corporate equities and mutual fund shares by wealth percentile group

What we have witnessed over the past 30 years under Greenspan, Bernanke, Yellen and Powell - and the corrupt, profligate Congress that has cheered them on - has been the absolute triumph of the financial class, and the financial decimation of the middle and lower classes.

Just look at the above numbers.

Today the top 0.1% own twice as many financial assets as what I, for simplicity sake, refer to as the “middle-class” - the entire 50th to 90th percentile!

This is what ZIRP and QE hath wrought, and financial markets of course want MOAR.

It’s incredible. In 1989 that same 50th to 90th percentile owned MORE than the top 0.1%.

The top 0.1% own 21.8% of assets (and growing), while the next 0.9% own 31.5%.

The top 1% now own 53.3% of financial assets. Even the next 9% - the financial upper middle-class - are losing ground.

And the bottom fifty-percent’s ownership has been cut in half - now a mere 0.6% of assets. A rounding error.

Whatever financial system we have adopted post-Greenspan has been grim for 90% of America, but very, very good for people like Larry Fink, Ben Bernanke, Janet Yellen and Jerome Powell.

Howell continues:

What I would argue is that you want to diversify if you believe or you fear that monetary inflation is ahead of us. My view is, there is no alternative. That’s what’s coming. Governments are gonna fund what seem to be huge, whopping and rising deficits. The only [there’s that word again - RH] choice they’ve got is to start printing money, because you know the numbers simply don’t add up otherwise. You can say, ok, they can force everybody to buy bonds, they may well try that, there may be attempts at yield curve control, that’s what’s foreshadowed in the book, but it’s highly likely that they will use monetary means, because they can’t afford to let interest rates go up and the simple reason is that if they let interest rates go up, the whole debt problem just compounds.

Wait - start printing money? Seems like that ship sailed awhile ago.

What hath Greenspan, Bernanke, Yellen and Powell bequeathed to us?

A system that is no longer a “new financing system,” where you borrow to build a plant, and have to measure cost of capital versus the return on investment - an environment where interest rates matter from a business point of view. No, now we’re are in a “debt refinancing system,” where we (well, not me, but somebody) has to rollover $70 trillion (with a “T”) of debt each year. According to Howell, for every $1 of new investment now, there is $7 of refinancing. Heckuva system, guys.

Why do we keep making serial arsonists fire marshals?

If you don’t have liquidity and balance sheet capacity you get debt defaults, you can’t roll debt, you get refinancing crises, and that’s what we’ve seen many many cases of in the last 20 years. These crises are refinancing crises. Central banks I believe are just waking up to this whole issue, and therefore liquidity is a paramount concern.

So doing more of the same will fix what Howell describes?

He ends the podcast saying he’s “looking forward to a bull market in assets.” Yay - for those with assets.

In the end, the solution - as always post 2008 - is MORE QE, MORE ZIRP, MORE Financial Repression - and, not surprisingly, more of America’s wealth being held in fewer and fewer hands.

Considering that half of Americans don’t own any assets, what’s good for Stephen Schwarzman and Barry Sternlicht most assuredly will not be good for them.

“…state bankruptcy is a one-time surgical intervention, while inflation is a permanent poisoning of the very bloodstream of a society.”

fyi I wrote on a variety of topics back in 2022 - they’re all free posts if you’re interested in browsing. This post is free because I rarely see anyone bring up these issues, which are important to me. (Our financial media is abysmal.) Anyway, I just started paid subscriptions a month ago (after 10 years of trying my best on Twitter for free.) If you like what you see, please consider subscribing. I’m not always so serious. Godspeed.

I had so much to say and no one to listen and then it happened, an unexpected thing: I began writing what they call a "mission statement." Not a memo, a "mission statement", a suggestion for the future of our company. A night like this doesn't come around very often. I seized it. What started out as one page slowly became twenty-five. Suddenly, I was my father's son again. I was remembering the simple pleasures of this job: how I ended up here out of law school, the way a stadium sounds when one of my players performs well on the field, the way we are meant to protect them in health and in injury. With so many clients we've forgotten what's important. I wrote and wrote and wrote and I'm not even a writer. I was even remembering the original words of my mentor, the late, great Dicky Fox. Suddenly it was all clear: the answer was fewer clients and less money, giving more attention to them, caring for them, caring for ourselves. I'll be the first to admit it, what I was writing was somewhat "touchy feely". I didn't care, I had lost the ability to bullshit. It was the me I always wanted to be. I put the mission statement into a bag and took it to a Copy Mat in the middle of the night, printed a hundred and ten copies. Even the cover looked like The Catcher in the Rye. I entitled it, "The Things We Think And Do Not Say: The Future of our Business."

a commotion or fuss, especially one caused by conflicting views.

clearly expressed and easily understood; lucid (I had to look it up)

With all the leveraged commercial office space, and with all the “work” at home that has continued, how can the commercial REITs be solvent? In other words, is Blackrock mgmt really as smart as they think they are?

The ShadowStats.com site continues to confirm your hypothesis that inflation, calculated the way it was in 1980 without all the lies about what they are "adjusting" and whether seasonal or hedonic are the bigger lies, is much higher than the gooferment claims.

You are also right that things like Yellen cannot perceive that inflation is torture because they are not able to see other people as humans. We are objects to be abused and manipulated.

Happily there is a charity serving lunch to the poor here in Ashland tomorrow. God provides. Amen.