There is No Average

Your home is shelter.

“How did you go bankrupt?” Bill asked.

“Two ways,” Mike said. “Gradually and then suddenly.”

Ernest Hemingway, “The Sun Also Rises”

Gary Webb

“I had a grand total of one story spiked during my entire reporting career. That's it. One. (And in retrospect it wasn't a very important story either.) Moreover, I had complete freedom to pick my own shots, a freedom my editors wholeheartedly encouraged since it relieved them of the burden of coming up with story ideas. I wrote my stories the way I wanted to write them, without anyone looking over my shoulder or steering me in a certain direction. After the lawyers and editors went over them and satisfied themselves that we had enough facts behind us to stay out of trouble, they printed them, usually on the front page of the Sunday edition, when we had our widest readership.

In seventeen years of doing this, nothing bad had happened to me. I was never fired or threatened with dismissal if I kept looking under rocks. I didn't get any death threats that worried me. I was winning awards, getting raises, lecturing college classes, appearing on TV shows, and judging journalism contests. So how could I possibly agree with people like Noam Chomsky and Ben Bagdikian, who were claiming the system didn't work, that it was steered by powerful special interests and corporations, and existed to protect the power elite? Hell, the system worked just fine, as far as I could tell. It encouraged enterprise. It rewarded muckraking.

And then I wrote some stories that made me realize how sadly misplaced my bliss had been. The reason I'd enjoyed such smooth sailing for so long hadn't been, as I'd assumed, because I was careful and diligent and good at my job. It turned out to have nothing to do with it.

The truth was that, in all those years, I hadn't written anything important enough suppress.”

- Gary Webb, Into The Buzzsaw: Leading Journalists Expose the Myth of a Free Press

Then, in 1996, Webb wrote a series of stories for The Mercury News, entitled Dark Alliance, that began this way:

For the better part of a decade, a Bay Area drug ring sold tons of cocaine to the Crips and Bloods street gangs of Los Angeles and funneled millions in drug profits to a Latin American guerilla army run by the U.S. Central Intelligence Agency, a Mercury News investigation has found.

This drug network opened the first pipeline between Colombia's cocaine cartels and the black neighborhoods of Los Angeles, a city now known as the "crack" capital of the world. The cocaine that flooded in helped spark a crack explosion in urban America-and provided the cash and connections needed for L.A.'s gangs to buy automatic weapons.

It is one of the most bizarre alliances in modem history: the union of a U.S.-backed army attempting to overthrow a revolutionary socialist government and the Uzi-toting "gangstas" of Compton and South Central Los Angeles.

In "Compromised: Clinton, Bush and the CIA," [Terry] Reed writes that he was an intimate of [Barry] Seal's, and says they were both at the center of an extensive, Arkansas-based CIA effort to train pilots for the Nicaraguan contra forces, manufacture and ship thousands of illegal weapons and parts to the contras, and help launder hundreds of millions of dollars in agency funds…

Then-Gov. Bill Clinton even has a cameo role or two, as do many of the people in his circle, including the Rose firm and former associate attorney general Webster Hubbell. In one memorable scene in the book, the future president pops into a meeting in an abandoned Army ammunition bunker to complain to North and future U.S. attorney general William P. Barr that he had taken great risks to accommodate the CIA's covert trade and didn't want it to end.

According to the book, the state collected a 10 percent "commission" on all of the CIA's "black money," some of which allegedly was laundered through close Clinton ally and once prominent bond broker Daniel Lasater.

"Like you, I grew up in this business thinking our job really was to tell the public the truth. Maybe that was the mission at one time. Maybe there was that Awakening in the 1970s with Watergate, the Pentagon Papers, the CIA scandals, etc.

But something very bad happened to the news media in the 1980s. Part of it was the 'public diplomacy' pressures from the outside. But part of it was the smug, snotty, sophomoric crowd that came to dominate the national media from the inside. These characters fell in love with their power to define reality, not their responsibility to uncover the facts. By the 1990s, the media had become the monster.

I wish it weren't so. All I ever wanted to do was report and write interesting stories—while getting paid for it. But that really isn't possible anymore and there's no use crying over it.

Hang in there. You're not alone."

- Bob Parry, AP reporter who first broke the Contra drug story in 1985, in a note to Gary Webb, Dark Alliance: The CIA, the Contras, and the Crack Cocaine Explosion

This woman is Katherine Roberts Maher, the chief executive officer and president of the National Public Radio since March 2024. She’s not fit to tie Gary Webb’s shoes:

"One of the questions I have been asked many times since this story broke is this: Now that the facts are out there, what can we do? My answer, depressing and cynical as it may be, is always the same. Not much." - Gary Webb, Dark Alliance

The Fiscal Impulse on Speed

“…how stimulative these deficits are! Once Trump started talking about his tax proposal, I said to myself, "This is game over. That's it. The economy is going to light up." I mean, we're talking - you know…this was by no stretch a reduction of the fiscal impulse. In fact, it was the fiscal impulse on speed!”

David Cervantes, Pinebrook Capital (on Twitter)

The term ‘Uniparty’ is right, at least on fiscal probity.

Everyone says they pay too much in taxes. I have paid enough taxes that I used to joke that they should name an aircraft carrier after me.

Nobody likes taxes.

But everybody sure loves to spend!

If more government debt is a good thing, why not just spend $100 trillion? I’m sure someday we will.

As Lacy Hunt reminded us last year,

“For every 1% increase in government size, you lose about one-tenth of 1% of your growth in the standard of living.”

Does Fiscal Stimulus Stimulate?

Here is Rob Arnott’s downloadable research paper: Does Fiscal Stimulus Stimulate?

“Excessive public spending’s unintended consequence is slower economic growth.”

The use of words like “stimulus,” “fiscal impulse,” “monetary stimulus,” and “government investment” in relation to government policy implies an incurious acceptance of government spending as a source of economic revival and even long-term growth. But according to our analysis, when government spending exceeds approximately 20% of GDP, it tends to hinder rather than help economic growth.

What’s more, increasing public debt can also stifle growth. Since the GFC in 2008, in particular, public debt accumulation has shifted into ever higher gears. This trend is likely to persist in the years ahead as developed countries spend more to support their aging populations.

This study can help reframe the discussion around government spending and debt. Excessive public spending’s unintended consequence—slower economic growth—must be part of the dialogue. Most of us would love government to do more for us. But if doing more for us means slower economic growth and less prosperity for our children, we might very well change our view. Let’s have that conversation.

An overview of everything that went wrong with economics:

Nice trick how economists like Fischer, Krugman, Bernanke, Yellen & Summers have been able to turn providing intellectual cover for a Cantillon Effect-on-steroids system - that created the greatest wealth divide in U.S. history - into their own generational wealth, provided by the super-rich!

“I have the nausea in my gut just like ‘08.”

I’ve had a nice influx of new paid subscribers lately. Thank you, it’s appreciated. As you can see above, the free people still get a lot of content - whether they want it or not - but all the good stuff is below the fold: more Rob Arnott, Mike Green, CRE with Sean Kelly-Rand, Melody Wright, Harley Bassman, Bens Bernanke and Hunt, and Waldo the Ostrich.

Rob Arnott

“I think stimulus always involves picking winners and losers, and therefore is always likely to be at least moderately misguided.”

“We looked at how does real per-capita GDP growth correlate with spending, and I was utterly unsurprised that the relationship was relentlessly negative. Folks in the economics community will say, of course it's negative - if the economy is shrinking, you have contra-cyclical programs, where spending will rise, and so of course you're going to get a negative result. Well, we didn't focus on single years for that very reason. We focused on rolling five-year results, because if you're boosting spending in a contracyclical way, and it doesn't boost real per-capita GDP growth on a 5-year window, then I think it's fair to say it failed.”

“We also took it back over 60 years in another paper that we're preparing now for an academic journal, and got the same results. Every single 5-year span, the countries that spent more, grew slower…it's an overwhelming relationship. It's contrary to Keynes, which has been accepted as economics dogma for almost 90

years at this point” [This matches what Lacy Hunt and William White have been warning - rh]

“there's bipartisan embrace of overspending”

“If the government wants to create a sudden surge in GDP, all they have to do is borrow like crazy, spend like crazy, and create a growth in government spending, which will create a corresponding growth in GDP. Tat doesn't make people more prosperous.”

“This was a fun paper, because it really does highlight how powerful the relationships are that conform to common sense, and don't conform to current prevailing economics wisdom.” [See William White here]

“Ours certainly is a wealthy economy that can afford a robust safety net, can afford to take care of those who are genuinely needy, but when you cross the line to take care of those who aren't needy by providing benefits to people who just choose to not do much with their lives, that has the dual effect of of rewarding indolence and rewarding lack of initiative and misaligning incentives, and I think most of us would agree that that's not a good thing.”

“If you ask people, do you want government to do more for you? Of course we do! If you ask people do you want government to do more for you if it reduces future growth and means your kids won't be as well off as they would be otherwise be? You're going to get a more nuanced answer.”

“Keynes himself would be appalled at some of the things that are called Keynesian these days.”

Mike Green on Passive Flows

“What we're we're seeing is somewhere in the neighborhood of about seven to eight dollars worth of market cap created for every dollar that flows into the market”

Someday this may work in reverse.

Saks Reveals $100 Million Loss in No-Questions Creditor Call

Saks Global Enterprises told creditors it had an adjusted loss of more than $100 million last fiscal year, one day after it announced a $350 million financial lifeline ahead of a looming coupon payment. The luxury retailer has $275 million in overdue payments to suppliers, management told bondholders in a Friday call…The company took no questions on that call…

The company’s bonds due 2029 rallied Friday, gaining as much as 9 cents on the dollar to 45.5 cents…

I just realized that Saks is no longer a public company, the last trade being on November 4, 2013. I was never a big department store investor. Missed that train.

Melody Wright

“I look at credit quality as someone who started in 2006, when things looked okay, except for the subprime book - and subprime was only about 12% of our book - things looked okay. Loan to value looked okay. For prime we were like, “prime's going to be fine,” and then you saw prime just degrade, degrade, degrade, degrade, at the same time home prices were coming down.”

“the FHA’s ridiculous loss mitigation program out was being used for fraud. People would buy a home, and never pay their home payment. Like never. And they would go back and back and back and you could see that this was being used for fraud.”

“in June we'll see how many people are going to cross that 30-plus day

delinquency, which we call the death cross, because it's that choice that you're going to let go of your credit score at that point.”

“you had the most multifamily [construction] in progress that we've had since the ‘70s, and we don't have the demographics to support it, At the same time, new home builders were building like crazy, building homes for sale, building homes to rent, multifamily builders were going nuts - and most of it was luxury, because they thought everybody was rich1”

“This inventory shortage narrative is just total B.S., and sure, do we not have affordable homes? 100%. Are we sort of low on the upper-middle class home that's the three-bedroom, three-bath kind of thing? Yes, because those are the people that can afford it. So there's a shortage there, but, in general, we per-capita have never had this much housing.”

General thoughts: “If you don't have 20% to put down, do not take out a mortgage. If you don't have a year of reserves, do not take out a mortgage. I don't care that you have two high-paying jobs. I cannot tell you how many people I've talked to in the last 6 months where they suddenly lost their job, so you need a year of reserves. You need a 20% down payment.” [See clip below]

‘We have to get back to a place where the investment is scrubbed out of the system, and we start looking at shelter as shelter again.’

Rosanna: “Do you think this time around it could be a similar magnitude to 2008-2009? How would you compare what you're seeing occurring now to the GFC1?”

Melody: ”I think we never finished that. I think that Wall Street came up and bought the inventory, and then rented it out. But prices - and this is going to sound crazy to people - but prices never really normalized. If you go back in history before Greenspan, you can look at home prices, and median income, you can look at the median home price, median income, and it it all makes sense, and home prices just go like this [slowly rising].Same with autos, because Ford made sure that the people that worked at his plant could afford his car. I recently wrote that essentially an auto worker back then could afford two and a half cars a year, if they had no other expenses. They now can't even afford one, based on their median wage. So you look at a chart where you look at median household median income since way back in the ‘60s, and then your median home price, either for your existing home, or your new homes, and we are so out of balance - we're way more out of balance than the GFC!

We have to get back to a place where the investment is scrubbed out of the system, and we start looking at shelter as shelter again.”

"Before 2010, institutional landlords DIDN'T EXIST in the single-family-rental market; now there are 25 to 30 of them, according to Amherst Capital, a real estate investment firm."

Francesca Mari, The Great Wall Street Housing Grab (March 2020)

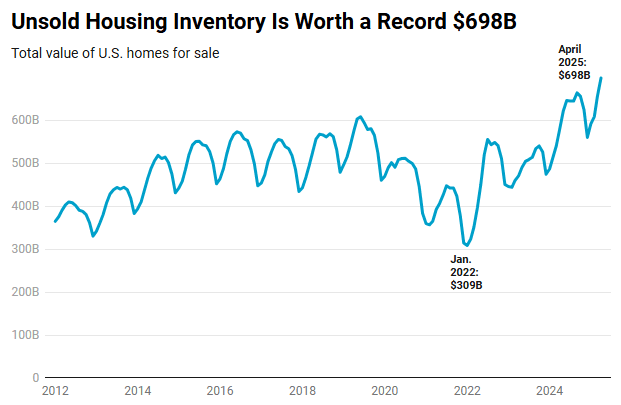

U.S. Home Sellers Are Sitting on Nearly $700 Billion Worth of Listings, an All-Time High

SAT Question: One of these does not belong with the others:

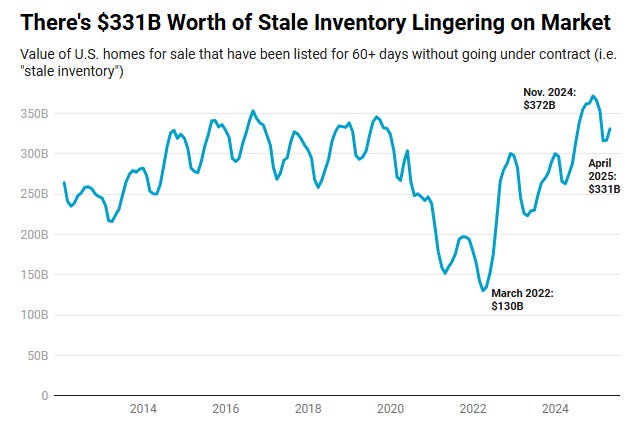

Housing supply is at a 5-year high.

Homes are sitting on the market longer.

Homebuying demand is falling.

Home prices are rising.

Sean-Kelly Rand

Managing Partner, RD Advisors I was not familiar with this guy, but once in a while on the CRE podcasts you get an insightful guest, and I enjoyed this one.

Don't count on the borrower paying you back.

“If it's leveraged returns, it's not alpha. That's just leverage. And that has its benefits on the upside, and has its costs on the downside.”

“Every single day you kind of have to be a little bit paranoid when you're doing underwriting.”

“There is actually some downward pressure on rates, and some upward pressure on LTVs. I don't think it's a great thing, and I think some of the investors that have jumped into the market are in and out players, right? They don't really understand it.”

“it's your marginal buyer that determines the price”

”You have to be fundamentally comfortable with owning the asset if you're going to be a lender”

“Don't count on the borrower paying you back. Make sure you're at a leverage level that if you have to take it over, you're comfortable taking it over.”

“Why don’t the banks take a loss on some of these loans?”

An important clip to watch. If you have savings, stay under the FDIC limit. Janet saved Bill Ackman, but next time they may not save you.

“One of the things I find most interesting is not reading the news, but googling the news on the eve of - go back and read the news in 2008. Go back and look up the housing section of the New York Times or the Wall Street Journal from January 2008, and you'll find some articles. I remember reading an article about a person wanting to buy a home and standing in line to get into an open house for a condo, and the price going above - and you're like this is in 2008! This isn't ‘06, this is ‘08. Open houses were still packed.

In hindsight, everybody goes back and says we all knew the world was collapsing, we all knew back in ' 06 that this was unsustainable - yeah, well, a lot of people were lining up at an open house desperate to buy a house or a condo in New York City on the eve of a global financial crisis. Are we smarter today, or is it just different signals that we're missing?”

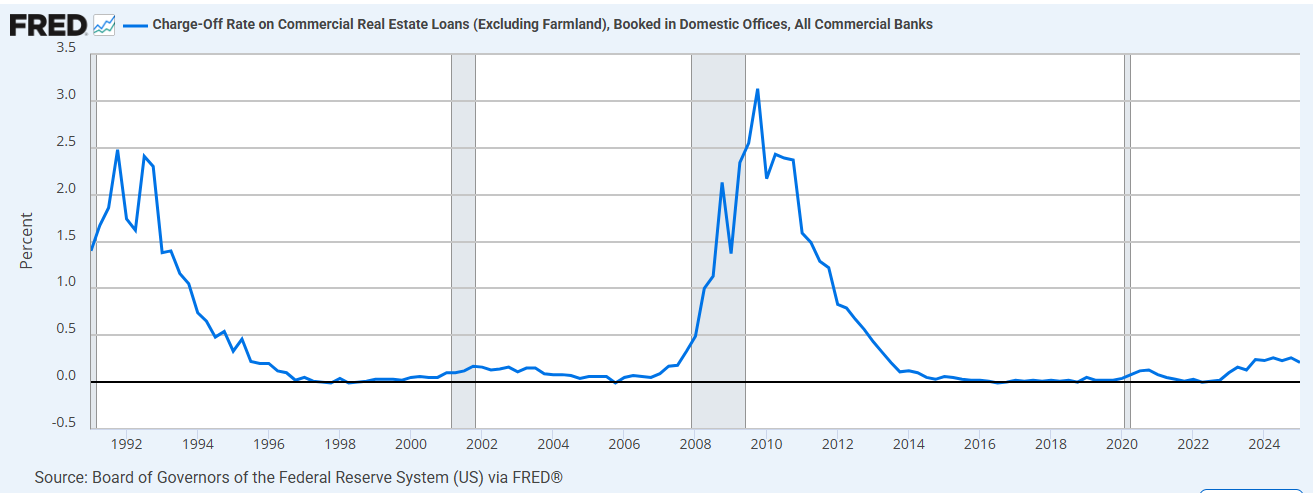

It doesn’t seem like banks are recognizing their CRE losses yet

Harley Bassman

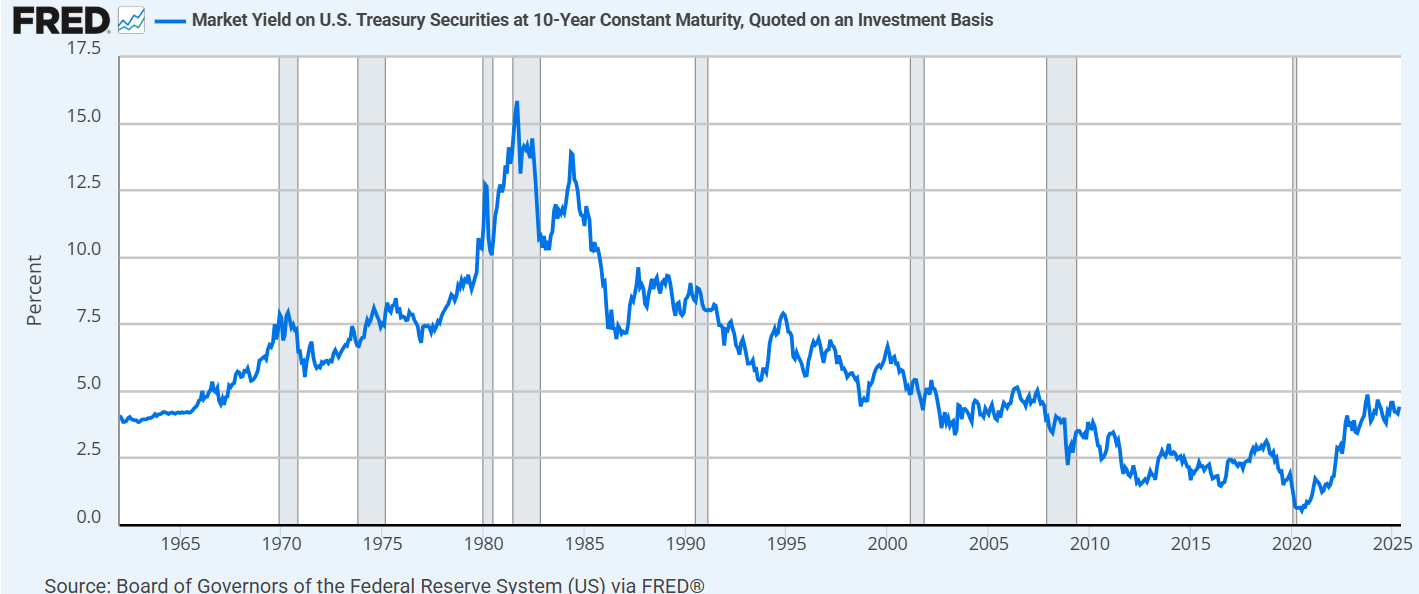

“Is a 4.35% 10-year yield crazy? No, it really isn’t. We’ve gotten back to normal.”

“…this big enchilada. The big one is the US dollar as the world’s reserve currency. If that is damaged, then we’ve got a problem, then we become Argentina or Venezuela or something else…seems to me that many people do not fully appreciate the value of being the world’s reserve currency that everyone has to use, and we can print. And you lose that -then you got a problem”

“I have been in the camp for quite a while of higher for longer. I’m not going to name names here, but you know who they are in Team Transitory. I don’t buy that. I’m U-Chicago. I think you print money, you get inflation, and that’s it. It might take a few years, but that’s how it works man.”

“This notion of Europe not paying their own way. The bigger picture is this, we as the world’s reserve currency, the world’s hegemon, we use our currency. It’s our legal system. We protect the seas. Basically, it’s our game and everyone plays by our rules and that is it, man. It doesn’t get better than that. The world plays by our rules and we decide everything.”

“Most of Japan’s debt is owned by Japan, so it’s not the same thing as us. We borrow and lend USD, so we’re the same as Japan in that way. I think the question you’re asking, which is I’ve always pondered if the BOJ is issuing and the other side buying, why can’t they just take the debt and just collapse it?”

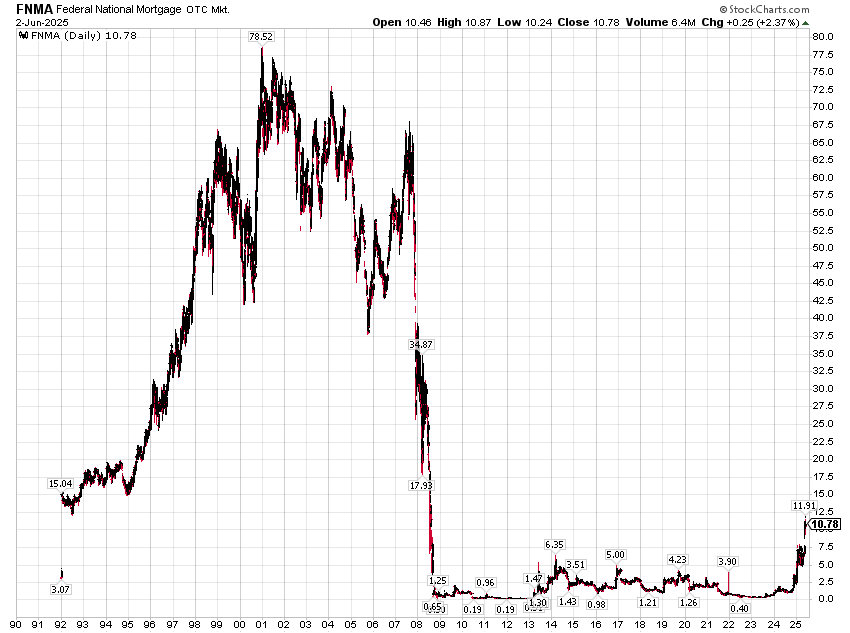

“I’m not going to mention names here, but you can go look up who the largest holders of Fannie Mae stock are. This is pure grift, okay? Pure grift. The idea of taking Fannie and Freddie and making them private again is utterly insane as a public policy concept. What do you got to learn about moral hazard? We’re going to go and make it so private people get the upside and the government gets the downside? We didn’t learn our lesson 15 years ago on this? So we’re going to go and pay off a few hedges to go and raise rates 50 basis points on all people who take out loans. And remember, who are the Fannie Freddie guys? They’re taking loans out $700,000 below. Like real people, not like rich guys like you two [Williams and Fleckenstein]. As a public policy concept, it’s terrible and I cannot believe it’s a serious idea. Spreads will widen - not tomorrow - but I mean over time because they have to. No reasonable person can say that we’re going to go and take away the U.S. government backstop and say things are better. They’re not. Now, will they tighten tomorrow? No, but will they widen? That’s the only direction we can go is wider.”

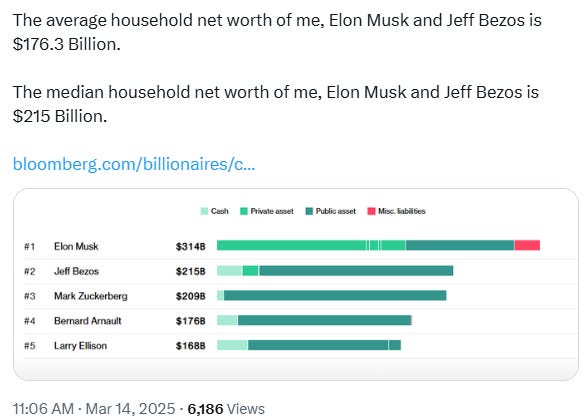

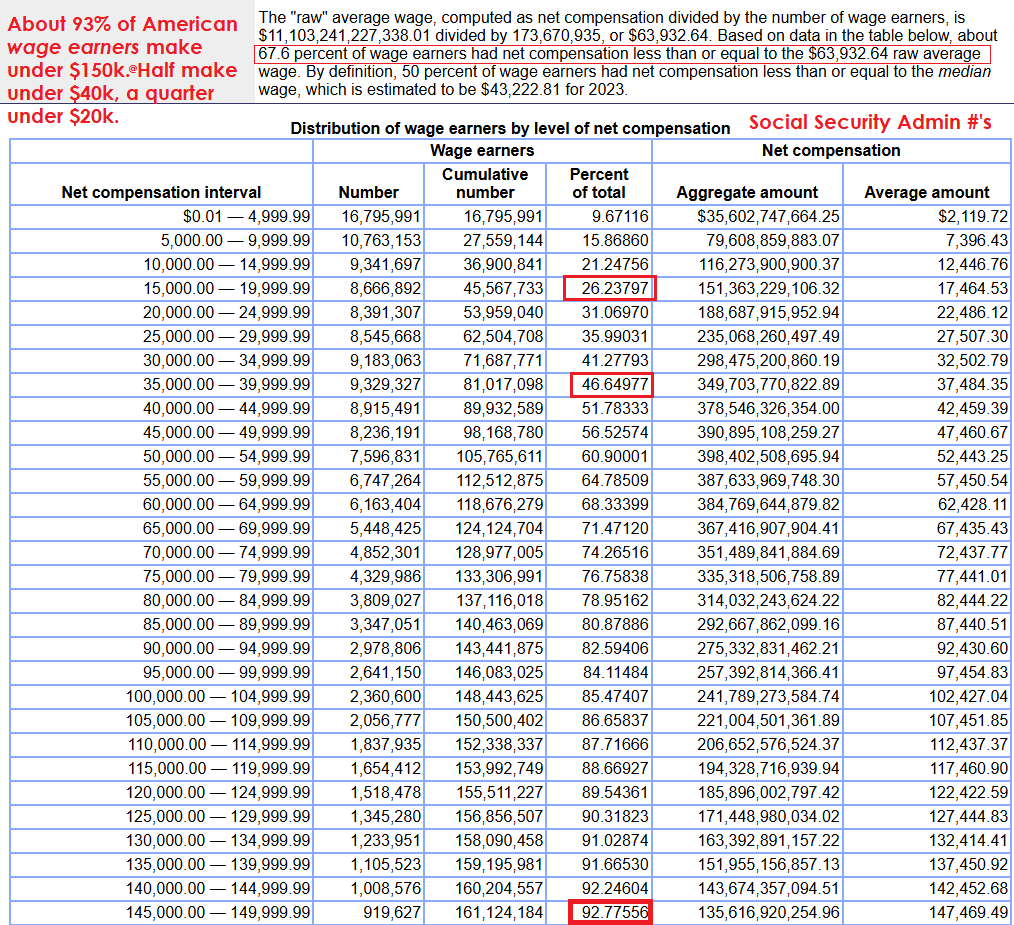

There is no average

“Let’s not get too deep into politics here, but Trump is not the problem. Trump is a symptom2 of something changing, and what’s changed over the last 20, 30 odd years is this income distribution has been...The Gini index has been widening and widening. We’re back to 1929 levels or maybe worse. And this is the core problem that somehow, some way, both parties did not address this in some manner, fashion or form to contain things. And now we’re coming to the point where we have this significant group of people who have financial issues.

It’s a mean median problem. So you have your small village of a hundred people, 99 of them make a thousand a year. One makes 10 million a year, so your average income is a hundred thousand but it really...There is no average. It doesn’t exist. You have a thousand a year and 10 million a year, and that’s where we are right now. As we keep talking about these average numbers and they’re bogus. If you actually look at the media, it’s very bimodal. What’s it now? 50% of all spending comes from the top 10%. And these people are certainly, they don’t care if prices go up by 5 or 10%, although I will say that restaurants actually have me now a little shocked.

Excellent and accurate private-equity rant

I always fount it amusing that Ben Bernanke - widely lauded as some "expert on the 1930's" - never learned a damn thing from the 1920's. This is from the outstanding popular history, “Only Yesterday,” by Frederick Lewis Allen:

Yes, the public bought. By 1925 they were buying anything, anywhere, so long as it was in Florida. One had only to announce a new development, be it honest or fraudulent, be it on the Atlantic Ocean or deep in the wasteland of the interior, to set people scrambling for house lots. "Manhattan Estates" was advertised as being "not more than three-fourths of a mile from the prosperous and fast-growing city of Nettie"; there was no such city as Nettie, the name being that of an abandoned turpentine camp, yet people bought. Investigators of the claims made for "Melbourne Gardens" tried to find the place, found themselves driving along a trail "through prairie muck land, with a few trees and small clumps of palmetto," and were hopelessly mired in the mud three miles short of their destination. But still the public bought, here and elsewhere, blindly, trustingly—natives of Florida, visitors to Florida, and good citizens of Ohio and Massachusetts and Wisconsin who had never been near Florida but made out their checks for lots in what they were told was to be "another Coral Gables" or was "next to the right of way of the new railroad" or was to be a "twenty-million-dollar city."

The stories of prodigious profits made in Florida land were sufficient bait. A lot in the business center of Miami Beach had sold for $800 in the early days of the development and had resold for $150,000 in 1924.3 For a strip of land in Palm Beach a New York lawyer had been offered $240,000 some eight or ten years before the boom; in 1923 he finally accepted $800,000 for it; the next year the strip of land was broken up into building lots and disposed of at an aggregate price of $1,500,000; and in 1925 there were those who claimed that its value had risen to $4,000,000. A poor woman who had bought a piece of land near Miami in 1896 for $25 was able to sell it in 1925 for $150,000. Such tales were legion; every visitor to the Gold Coast could pick them up by the dozen; and many if not most of them were quite true—though the profits were largely on paper. No wonder the rush for Florida land justified the current anecdote of a native saying to a visitor, "Want to buy a lot?" and the visitor at once replying, "Sold."

Yeah, we had Bernanke’s back in the 1920’s too…

The speculative fever had been intensified by the action of the Federal Reserve System in lowering the rediscount rate from 4 per cent to 3½ per cent in August, 1927, and purchasing Government securities in the open market.

This action had been taken from the most laudable motives: several of the European nations were having difficulty in stabilizing their currencies, European exchanges were weak, and it seemed to the Reserve authorities that the easing of American money rates might prevent the further accumulation of gold in the United States and thus aid in the recovery of Europe and benefit foreign trade. Furthermore, American business was beginning to lose headway; the lowering of money rates might stimulate it. But the lowering of money rates also stimulated the stock market. The bull party in Wall Street had been still further encouraged by the remarkable solicitude of President Coolidge and Secretary Mellon, who whenever confidence showed signs of waning came out with opportunely reassuring statements which at once sent prices upward again. In January 1928, the President had actually taken the altogether unprecedented step of publicly stating that he did not consider brokers' loans too high, thus apparently giving White House sponsorship to the very inflation which was worrying the sober minds of the financial community.

Every policy decision made by China and Europe and Japan and the US in the wake of the Great Financial Crisis was made with a singular goal in mind – to prop up and inflate financial asset prices. Originally, it was to keep the status quo financial system from imploding. But soon after…and still now…it was to keep the status quo political system from imploding. What started as an entirely laudable effort to keep capital markets from collapsing became an entirely problematic effort to turn capital markets into political utilities. This has been a Team Elite goal since at least 1997...

So what’s the problem with being richer than you “should” be?

The problem is how those riches are distributed. The problem is that the road to hell is paved with good intentions, sure, but even more so with hubris and post hoc rationalizations.”

The Black Vault filed a FOIA request to get the “photographs and videos of the wreckage of United Flight 93, taken on or around September 11, 2001” released to the public.

That case was filed in December of 2021, and on February 14, 2022, the FBI responded by denying all of the records as being “exempt from disclosure.”

This movie looks terrible.

A MAJOR X bug was put in in early May 2025 which basically trashed many long, multi-year threads, including my infamous “Fugazi” one that dated back to 2016. Tweets are not viewable or shareable (web version at least). Thanks, Elon.

I noticed right away because I have a number of long, connected threads, many of which date back years. I’ve complained, but Twitter is about as awful as it has ever been since I got there in 2013.

I’ve used Twitter - as well as the old emails I used to send to friends - as sort of a database of things of interest to me, easily searchable even a decade later. I used threads as a way to tie connected things together. I can still retrieve old tweets - if I know the day or the keywords - but it’s so tedious - a lot like being permanently suspended but still having my archive.

Anyway, because I can’t trust Elon or Twitter or anything at all really (see: Tony Deden), I may put random articles from my tweets (and sometimes private emails) on Substack for posterity, as long as they’re still relevant, which they usually are.

You guys are used to disconnected eclectic stuff by now anyway.

Larry Summers is “more responsible for the economic mess in this country than any single human being."

Robert Scheer, 2016

Ben Hunt: “Crisis Actors and a Reichstag Fire” (July 2016)

“I understand that I’m tarring central bankers and their fellow travelers with the fascist brush.

Because the road to hell is paved with good intentions as well as bad. Because there IS a moral equivalence between the means used by Göring and Erdogan to accomplish their ends and the means used by central bankers to accomplish theirs.

Do the differing ends and the better intentions matter? Of course they do. And that’s why Ben Bernanke gets $250,000 per speech and Hermann Göring got a cyanide pill in his prison cell.

But the shared means of false Narrative and crisis acting matter, too, because they create a world of profound inauthenticity, where ALL public speech is deemed suspect and self-serving — because it is! — and where ANY public speech, no matter how demagogue-ish or false or borderline insane, is deemed functionally equivalent to any other speech. Because it is.

It’s what I call Gresham’s Law of Narrative: inauthentic speech drives authentic speech out of circulation, just like bad money drives good money out of circulation.

If the function of public speech is to persuade rather than inform — and that’s precisely the function of forward guidance and every other status quo political statement of the past seven years — then it’s just comical for those same status quo institutions to complain now that their political opponents are “lying”. No, they’re just more effective persuaders. They’re just better liars.”

"Obama could sell Trump Steaks to a vegan."

Jeffrey St. Clair, Night of the Hollow Men: Notes From the Democratic Convention (2016)

September 2018: “Ten years after the financial crisis brought the U.S. economy to its knees, about 30 percent of the lawmakers and 40 percent of the senior staff who crafted Congress’ response have gone to work for or on behalf of the financial industry, according to a Washington Post analysis.”

An ostrich named Waldo

“Waldo lived in the exotic animal compound behind the House of Cash offices, and in September ’81, he was the sole survivor of a cold spell that croaked the rest of the ostrich population there, including Waldo’s mate. In his grief and isolation, Waldo went rogue. As [Johnny] Cash walked through the compound, the eight-foot bird materialized and crouched in front of him with wings out, hissing menacingly. Cash froze, and for several moments, they stood there like a couple of gunfighters. Waldo backed off, but a few minutes later, he returned, fully locked and loaded. By then, Cash had wisely armed himself with a six-foot-long stick, and the battle was joined.

Johnny’s home run swing missed because the 250-pound Waldo leaped straight up into the air. He came down with his razor-like claws extended, breaking two of Cash’s ribs and ripping open his stomach. Only the big metal belt buckle he wore prevented Johnny from being disemboweled. Before Cash managed to get a lick in with the stick and drive Waldo off, the ostrich broke three more of his ribs.

(Waldo won the battle but lost the war. According to those in the know, the battling ostrich’s final resting place—semi-final, actually—was Cash’s freezer.)”

“That song was written during the Vietnam War and so it’s very much about the awareness that war is always present; it was very present in life at that point”

- Jagger

Again, the best way to search this - or any Substack you subscribe to - is:

site:rudy.substack.com [search keyword(s) or phrase in quotes]

e.g., in Google:

site:rudy.substack.com epstein “Larry summers”

Ignore Google’s goofy “AI Overview” that pops up first. Not sure what other search engines have the “site” option.

They’re not rich. And yes, to make it clear, these are W-2 employees. Some people work multiple jobs, some are self-employed. I know that.

I’ve been saying this for 10 years

Keep in mind that - even using the goofy BLS CPI calculator - $150k in 1924 is roughly $2.88 Million in April 2025.

Gary Webb's reported suicide must be the only case in history where someone shot himself twice in the head

I listened to Bassman and read Marc Faber's letter. Both assume some notion of "free market captialism". Faber is more "libertarian" leaning than Bassman, from my perspective. But is that really the case?

Read Jonathan Tepper's "Myth of Capitalism", which speaks to the monopolistic, oligopolistic, misopolistic (one price take) type of structure here. He makes a very persuasive case that capitalism is a "Myth" so to speak. So the basis of the arguments appears to me to be unfounded.

Does Harley have any children in the military, such that if Article 5 is activated that child might be reduced to ashes defending, say Latvia? I doubt it. With allies like this and the rest of Europe, I think we can do without.

Would are military spending decrease if Europe actually spent some money on defense?

Well why isn't that question asked and why isn't it (spending here) reduced.

We're broke and cannot afford to defend the transoceanic space for all of our allies. Including counties like Australia and New Zealand.